Saved cards look harmless. They speed up checkout, support subscriptions, and make repeat purchases easier. But they also sit right in the middle of one of the biggest fraud problems in e-commerce.

Card-not-present transactions accounted for 73% of the $33.83 billion in global card fraud losses in 2023, and every $1 of fraud costs merchants an average of $3.75 once you include fees and chargebacks, according to PayCompass' credit card fraud statistics roundup.

If you run a Shopify store, that matters because almost every card on file payment is also a card-not-present payment. That means the same feature that helps you sell faster can also make it easier for fraudsters, and just as often, for legitimate customers to dispute charges they forgot, didn't recognize, or decided to challenge after the fact.

A lot of merchants think of card on file as a checkout feature. A risk manager sees something different. It changes how charges happen, what proof you can show later, and how likely you are to get dragged into a dispute.

The Double-Edged Sword of Saved Cards

A saved card solves a real business problem. Returning customers don't want to retype payment details. Subscribers don't want to manually renew every month. If you're selling supplements, coffee, skincare, memberships, or refill products, card on file isn't a nice extra. It's part of how you keep revenue predictable.

The problem is that convenience removes friction for everyone. Good customers move faster. Fraudsters move faster too. And so do customers who signed up, forgot, then filed a chargeback when the next billing cycle hit.

Why saved cards create more dispute risk

With card on file, the customer often isn't actively entering their payment details when the charge happens. That gap creates confusion.

Common examples look like this:

- A subscriber forgets a renewal date and disputes the charge as unauthorized.

- A spouse sees your descriptor on a statement and doesn't recognize it.

- A customer updates nothing after a card replacement, then gets billed later through an updater service and thinks the charge shouldn't have gone through.

- A fraudster takes over an account that already has a saved card attached.

Practical rule: The easier it is to bill a saved card, the easier it is for a customer to later say, "I didn't mean for this charge to happen."

That's why card on file needs to be treated as both a growth tool and a chargeback risk. If you only focus on conversion, you'll miss the downstream cost. If you only focus on security, you'll damage retention.

The real merchant dilemma

Most Shopify owners don't have the option to avoid saved cards completely. Customers expect one-click checkout. Subscription apps rely on stored credentials. Rebilling flows depend on it.

So the question isn't whether to use card on file.

It's whether your store has enough control around it to stop preventable disputes, catch fraud early, and keep enough evidence when a chargeback lands.

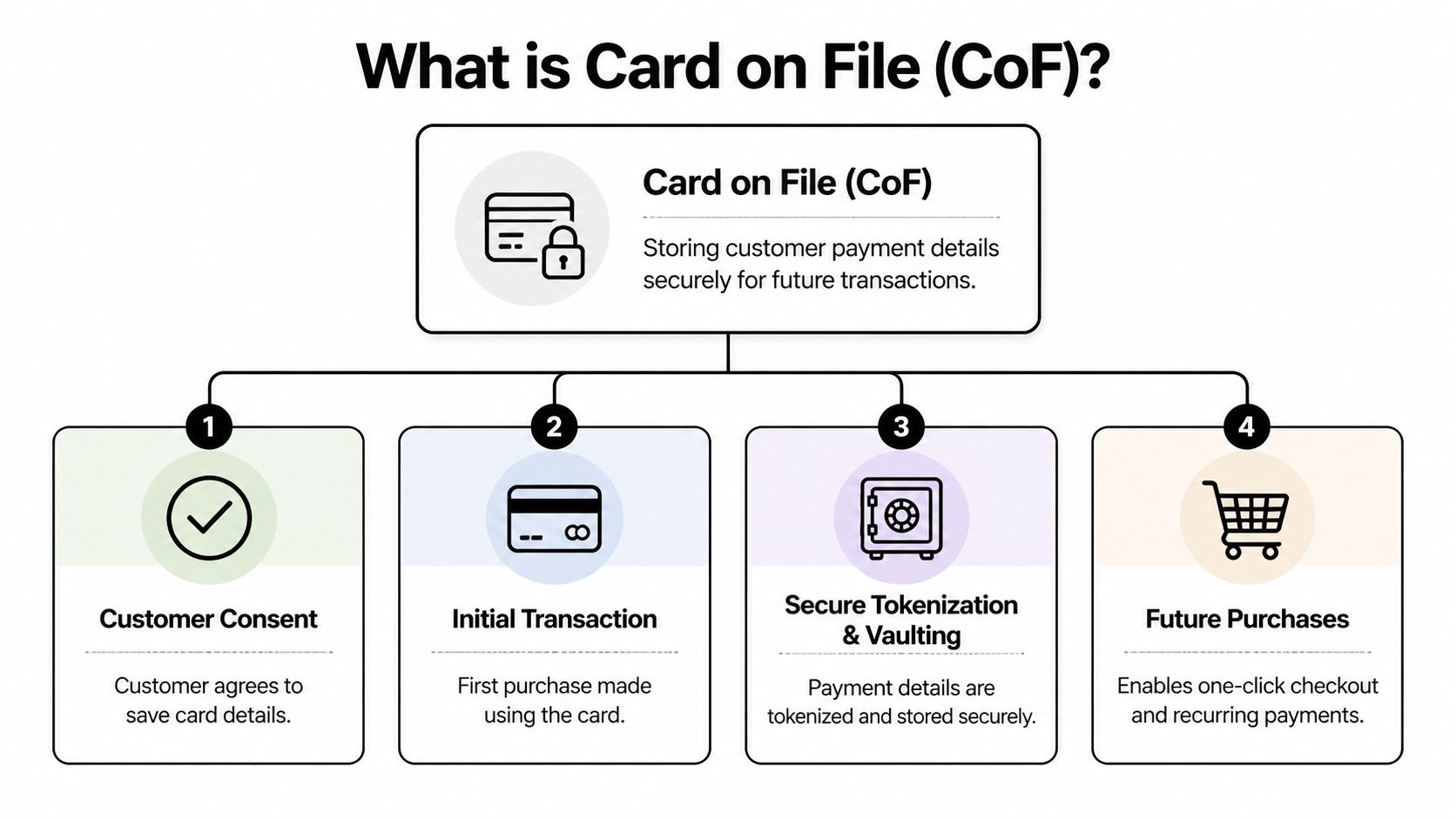

What Exactly is a Card on File Transaction

A card on file transaction happens when a customer gives permission for their card details to be stored for later use. They make the first purchase, the payment system stores the credential securely, and future charges can happen without the customer typing the full card number again.

The easiest way to think about it is a tab at a local shop. You approve the card once, and the business can charge future purchases based on that stored payment method. Online, the process is more controlled and more technical, but the business idea is the same.

Three common card on file situations

Most Shopify stores use card on file in one of these ways.

| Type | What it looks like in a Shopify store | Main dispute risk |

|---|---|---|

| Recurring billing | Monthly subscriptions for coffee, vitamins, skincare, pet food | Customer forgets renewal or says cancellation didn't process |

| Returning customer checkout | A logged-in buyer uses saved payment details for a repeat order | Customer later claims they didn't authorize the order |

| Scheduled or split payments | A merchant charges later based on an agreed payment plan or delayed fulfillment setup | Buyer disputes timing or says terms weren't clear |

Recurring billing

This is the clearest example. A customer buys a monthly product subscription, agrees to future billing, and your system charges the saved card at each renewal.

This works well when communication is clear. It creates trouble when the buyer misses an email, doesn't understand the schedule, or expected the subscription to stop.

For many merchants, these conditions lead to friendly fraud. The cardholder is real. The product may have shipped. But the customer still disputes the charge because they don't remember consenting, don't recognize the transaction, or don't want the product anymore.

One-click checkout for repeat buyers

Saved cards also power fast repeat purchases. A returning customer logs in, clicks through quickly, and finishes checkout without re-entering card details.

That speed helps conversion, but it can also create "I didn't mean to buy that" disputes. If the shopper used the wrong account, a child placed the order, or the household shares devices, the merchant may end up defending a transaction that looked normal at the time.

A card on file payment can be fully authorized at checkout and still become a chargeback later because the customer experience around the charge wasn't clear enough.

Merchant-initiated and customer-initiated charges

Here, many store owners get confused.

Some card on file charges happen because the customer is actively present, such as clicking to buy with a saved card. Others happen because the merchant initiates the charge later, such as a renewal or installment payment.

That distinction matters because customer memory, billing expectations, and evidence quality are different in each case. If your store charges cards after the initial order, your billing terms, reminders, and cancellation flow matter just as much as the original authorization.

How Card on File Works Under the Hood

Most merchants hear terms like tokenization, vaulting, PCI, and encryption and assume they need a payments engineering team to understand saved cards.

You don't.

The simplest mental model is a coat check. You hand over something valuable. In return, you get a claim ticket. The ticket points to the item, but it isn't the item itself.

Tokenization in plain English

When a customer enters card details, a secure payment system can replace the actual card number with a token. That token stands in for the card during later actions.

According to Bluefin's explanation of card-not-present fraud prevention, the core of secure card on file is tokenization, which replaces sensitive card numbers with non-sensitive tokens. Bluefin also notes that this ties to PCI DSS Requirement #4 for protecting cardholder data in transit.

If someone steals the token from your system, they don't automatically get a usable card number. That's the whole point. The token has no direct value outside the payment environment that issued it.

If you want a deeper breakdown, this guide on tokenization in payments is worth reading.

What vaulting means

The actual card data needs to live somewhere secure. That's where a vault comes in. The vault is controlled by the payment provider or another approved service that stores card credentials safely.

For a Shopify merchant, that means you usually aren't storing raw card numbers yourself. Your payment provider does the heavy lifting, and your store works with references, permissions, and tokens.

That setup reduces your exposure, but it doesn't remove your responsibility.

What your payment processor handles and what you still own

A useful way to split this up is simple:

- The payment provider handles secure storage, encryption, token generation, and much of the PCI burden around raw card data.

- You handle customer consent, billing clarity, app choices, account security, staff access, and how saved-payment flows appear inside your store.

Here’s where merchants get tripped up. They assume "the processor stores the card, so security is solved." It isn't.

You can still create dispute problems if your subscription terms are muddy, your cancellation path is hard to find, or your support team can't prove what the customer agreed to.

Secure storage protects the card number. It doesn't protect you from a customer saying they never expected the charge.

The Hidden Costs and Risks of Storing Cards

Saved cards create revenue. They also create liability.

Once you store a card for future billing, you're operating in a part of payments where proof is harder, customer confusion is more common, and fraud pressure is higher. Many merchants find that out only after a wave of disputes hits.

Why card on file sits in the riskier category

A card on file charge is usually a card-not-present transaction. The card isn't physically tapped, dipped, or swiped in front of you. That changes how issuers and networks view the risk.

The shift became more obvious after EMV chip adoption in the U.S. Around that period, fraud moved online. The Kansas City Fed's payments research briefing notes that CNP fraud rates on some networks increased by over 10 basis points by 2023, and that liability rules in CNP disputes often favor issuers.

For merchants, that means this: when a saved-card transaction is challenged, you're often the one who has to prove the charge was valid.

Friendly fraud is where convenience turns expensive

Not every card on file dispute starts with stolen credentials. A lot of them start with ordinary customer behavior.

A buyer signs up during a promotion. Weeks later, the rebill arrives. The packaging looks unfamiliar. The bank statement descriptor isn't obvious. The buyer contacts the bank instead of your support team.

That's friendly fraud. The cardholder may have made the original purchase. They may have received the product. They may still dispute the later charge anyway.

Typical triggers include:

- Subscription amnesia where the customer forgot the recurring plan

- Poor billing descriptors that don't match the brand name customers remember

- Messy cancellation flows that push customers toward their bank

- Account sharing where one household member places an order and another disputes it

- Impulse repeat orders made too quickly with a saved card

The biggest risk with card on file isn't only outside fraud. It's the mismatch between what your system allowed and what the customer remembers later.

Security mistakes still matter

Even with tokenization, your surrounding systems matter. Admin access, app permissions, customer account security, and how data moves between tools can all affect risk.

Merchants that need a practical framework for internal controls can review F1Group's expert data security advice for data governance habits that support safer operations around customer information.

A weak process doesn't need to expose raw card numbers to create damage. It only needs to create enough confusion, poor records, or account abuse to produce avoidable chargebacks.

The cost isn't just the lost sale

When a chargeback lands, you don't just lose product revenue. You can lose shipping costs, fulfillment effort, ad spend, dispute fees, staff time, and your chance to resell that inventory.

If you need a simple breakdown of one part of that cost stack, this guide on what a chargeback fee is helps clarify what merchants often overlook.

Here's the part many founders underestimate. Card on file disputes don't arrive one by one in a nice clean pattern. They cluster around renewals, billing changes, failed cancellation experiences, and fraud attacks. When they pile up, support gets swamped and the finance team starts chasing losses after the money is already gone.

Best Practices to Secure Payments and Reduce Disputes

Most card on file problems don't come from one dramatic failure. They come from small gaps. A vague billing page. A missing reminder. A checkout that saves payment details without enough context. A fraud filter that doesn't notice card testing until banks start sending disputes.

The good news is that these issues are manageable if you treat prevention as part of store operations, not just payment setup.

Fix customer confusion before it becomes a chargeback

A lot of friendly fraud starts with bad communication, not criminal intent.

Use a simple standard for every saved-card program:

- Say exactly what will happen. Show billing frequency, renewal timing, cancellation rules, and next-charge timing before the customer completes the first purchase.

- Send reminders before rebills. Especially for subscriptions and higher-ticket recurring orders.

- Make cancellation obvious. If customers can't stop billing quickly, many will go to their bank instead.

- Match your descriptor to your brand. If the statement name looks unfamiliar, disputes rise.

- Confirm key account changes. If shipping address, login credentials, or subscription frequency changes, notify the customer right away.

A useful operational habit is to centralize billing event records. Teams that care about reconciliation and customer history often benefit from clearer internal visibility, and this guide on optimizing payment tracking for SA businesses has practical ideas you can adapt for tracking payment activity and follow-up workflows.

Add extra proof where it counts

Not every card on file action needs maximum friction. But some moments do need stronger verification.

Use stronger controls for:

- The first time a card is saved

- Large order values

- Changes to subscription terms

- Suspicious account behavior

- Orders shipping to new or mismatched details

Tools like AVS, CVV checks, and step-up authentication can help you establish better evidence at the point where the payment method is attached or reused.

If you're evaluating authentication options, this overview of 3-D Secure authentication is a useful starting point.

Watch for card-testing behavior

Card-on-file systems are attractive to fraudsters because once they validate a card, they can move quickly.

According to Specprotected's breakdown of card testing prevention, advanced fraud-scoring engines and velocity controls can detect card-testing attacks in real time by analyzing IP addresses, transaction timing, and device fingerprints.

That matters for two reasons. First, you can stop bad transactions earlier. Second, the logs from those attacks can become strong representment evidence if disputes follow.

Look for patterns like:

- Many low-value attempts in a short period

- Repeated failures from one IP or device fingerprint

- Rapid testing across multiple cards

- Account logins and purchases that don't fit normal buyer behavior

When you can show a coordinated fraud pattern instead of a single isolated order, your dispute response gets much stronger.

Build for fewer disputes, not just better responses

A good card on file setup makes the right customer actions easy and the risky actions harder.

Use this quick comparison:

| Weak setup | Strong setup |

|---|---|

| Subscription terms buried in fine print | Billing terms shown clearly before checkout |

| No pre-renewal notice | Reminder sent before recurring charge |

| Hard-to-find cancellation path | Self-serve cancellation and account management |

| No fraud monitoring for saved cards | Velocity rules and behavior checks |

| Thin order records | Stored consent, order timeline, and customer communication history |

Prevention doesn't remove every chargeback. But it gives you cleaner transactions, better records, and fewer avoidable losses.

Your Shopify Card on File Implementation Checklist

Shopify gives you a strong payments foundation, but the defaults alone won't solve card on file risk. You need a store-level checklist that covers settings, apps, customer messaging, and failure handling.

Start with your payment and fraud settings

Before you touch subscriptions or one-click experiences, review the basics inside your Shopify setup.

- Turn on address and card verification checks. If your payment configuration supports AVS and CVV checks, use them.

- Review your fraud analysis signals. Look for mismatched locations, unusual order behavior, and repeat attempts.

- Limit admin access. Only the people who need payment-related permissions should have them.

- Audit installed apps. Remove payment-adjacent apps you don't trust or no longer use.

For a deeper operational playbook, this guide to Shopify fraud prevention is a useful companion.

Choose apps that reduce billing confusion

If you run subscriptions, your app choice matters as much as your payment setup.

A strong subscription app should make it easy for customers to:

- see their next billing date

- update payment details

- pause or cancel without contacting support

- review prior charges

- confirm what plan they're on

If customers need to email support just to stop a subscription, you are increasing dispute risk.

Prepare for expired and replaced cards

One of the most overlooked card on file issues isn't fraud. It's operational friction.

The Basis Theory article on card-on-file transactions notes that when a saved card fails because it expired or was replaced, failed recurring charges often lead directly to customer service chaos and disputes. It also points to real-time account updater tools as a critical step because they can automatically refresh card details when they change.

That matters in practice because failed payments create messy customer journeys. A rebill may happen later than expected. A customer may think they canceled when the card merely failed. Support may manually retry without enough explanation. Each of those paths can end in a chargeback.

A saved card that quietly updates is often less risky than a failed card that triggers confusing retries and support back-and-forth.

Tighten communication around every rebill

Use short, direct customer messages for saved-card billing:

- Initial confirmation that states the card was saved and why

- Renewal notice that states the date and amount of the next charge

- Payment update prompt when a card needs attention

- Cancellation confirmation so the customer has clear proof that billing stopped

This isn't glamorous work. It prevents a lot of avoidable disputes.

Set rules for when to slow an order down

Not every returning customer order should glide through untouched.

Create manual review triggers for things like:

| Trigger | Why it matters |

|---|---|

| New shipping address on a saved card | Could indicate account takeover or resale fraud |

| Unusual order size | Doesn't match prior customer behavior |

| Multiple retries in a short span | Can signal testing or automated abuse |

| High-risk digital goods order | Harder to recover once delivered |

A clean Shopify card on file setup isn't just about storing credentials. It's about making sure each later charge still makes sense.

Automate Your Defense Against COF Chargebacks with ChargePay

Manual chargeback handling breaks down fast when card on file disputes start stacking up. By the time your team pulls order logs, email records, renewal terms, tracking data, and account history together, the deadline is already close.

That's where automation matters.

ChargePay is built for Shopify merchants dealing with exactly this problem. It uses AI to fight chargebacks across the full dispute lifecycle, including the messy cases tied to saved cards, recurring billing, and friendly fraud.

ChargePay has a 92.4% win rate, has handled 200K+ disputes, and has recovered $10.8M+ for merchants. It detects friendly fraud patterns, builds representment evidence in real time, and submits responses before deadlines without forcing your team into manual dispute work.

That matters for card on file transactions because these cases often depend on scattered evidence. The strongest response usually isn't one document. It's the full timeline. Original order details, stored-card consent, billing history, customer communication, delivery proof, and signs that the charge came from a legitimate account relationship.

Instead of having your support team piece that together one case at a time, ChargePay automates it.

A few details make it especially relevant for Shopify stores:

- Built for Shopify badge

- 4.9-star rating on the Shopify App Store

- Pay-per-win pricing, so you only pay when money is recovered

If your store uses subscriptions, repeat billing, or one-click checkout, card on file disputes aren't an edge case. They're part of the business. Automation is often the only practical way to defend that revenue consistently.

Frequently Asked Questions About Card on File

Am I still responsible for PCI compliance if I use Shopify and payment apps

Usually, your payment provider handles the raw card storage side, especially when tokenization and hosted payment fields are used. But you still need to manage your own environment responsibly. That includes staff access, app permissions, customer account security, and clear consent records.

Can I require customers to save a card on file

You can offer it, but forcing it is usually a bad idea unless the business model requires recurring billing or scheduled payments. Customers should understand why the card is being stored and what future charges may happen. Clear opt-in language reduces later disputes.

What's the difference between customer-initiated and merchant-initiated card on file payments

A customer-initiated payment happens when the buyer is actively checking out with a saved card. A merchant-initiated payment happens later, such as a subscription renewal or installment charge. Merchant-initiated payments usually create more confusion if reminders, terms, and cancellation options aren't clear.

Does tokenization eliminate chargeback risk

No. Tokenization protects card data. It doesn't stop friendly fraud, subscription confusion, account takeover, or poor billing communication. It solves one security problem, not the full dispute problem.

Should I keep cards on file for every repeat customer

Not automatically. Saved cards help conversion, but they also create extra exposure. Use them where they match the customer experience you want to offer, and support them with good communication, authentication, and monitoring.

If card on file is helping your Shopify store grow but chargebacks are eating into that revenue, ChargePay can do the heavy lifting. It automatically fights disputes, detects friendly fraud, and recovers lost revenue with a 92.4% win rate across 200K+ cases and $10.8M+ recovered. It has a Built for Shopify badge, a 4.9-star rating, and a pay-per-win model. Install it from the Shopify App Store and let the system recover your money instead of your team chasing chargebacks manually.

.svg)

.svg)

.svg)

.svg)