Most chargeback advice is too polite. That is the issue.

If you run a Shopify store, a chargeback response is not paperwork. It is revenue defense. You are not arguing over one order. You are protecting margin, staff time, processor trust, and your ability to keep scaling without getting buried in dispute admin.

I have a simple view on this. If a dispute is invalid and you have the evidence, fight it fast and fight it clean. If your process is messy, manual, and late, you will lose cases you should have won.

The High Cost of Ignoring Chargebacks

In the United States alone, cardholders disputed $65.2 billion worth of charges in 2023, while the total cost to U.S. merchants reached about $243.75 billion. Globally, merchants responded to only 53% of disputes, which means nearly half went unchallenged (ChargebackStop chargeback statistics). That gap is the whole story.

A chargeback does not stop at the order value. You lose the sale, absorb fees, burn support time, and add another mark against your processing profile. That is why merchants who treat chargebacks like random customer service noise get punished twice. First by the reversal, then by the operational drag.

What merchants usually miss

Most store owners think the pain starts when the bank takes the money. It starts earlier.

Your team wastes time hunting order confirmations, checking tracking links, pulling email threads, and trying to decode issuer language that was not written for merchants. If you want a plain-English breakdown of one piece of that cost stack, this guide on what a chargeback fee is is worth reading.

A legal mindset shift is present here. A chargeback works a lot like a forced reversal mechanism. If you have ever looked at a clawback provision, the idea feels familiar. Money that looked settled can be pulled back under defined conditions. The difference is that in e-commerce, the timeline is shorter and the burden lands on you fast.

Why ignoring one dispute creates more trouble

Merchants train their own future losses when they do not respond.

Customers learn when a brand is easy to challenge. Issuers also see patterns. If your records are weak and your responses are inconsistent, you make yourself look disorganized even when the order was legitimate. That turns a frustrating process into a repeatable leak.

My opinion is blunt. A passive chargeback response process is not a strategy. It is surrender with extra admin attached.

Takeaway: You do not beat chargebacks by caring more. You beat them by building a response system that is fast, reason-code-aware, and evidence-first.

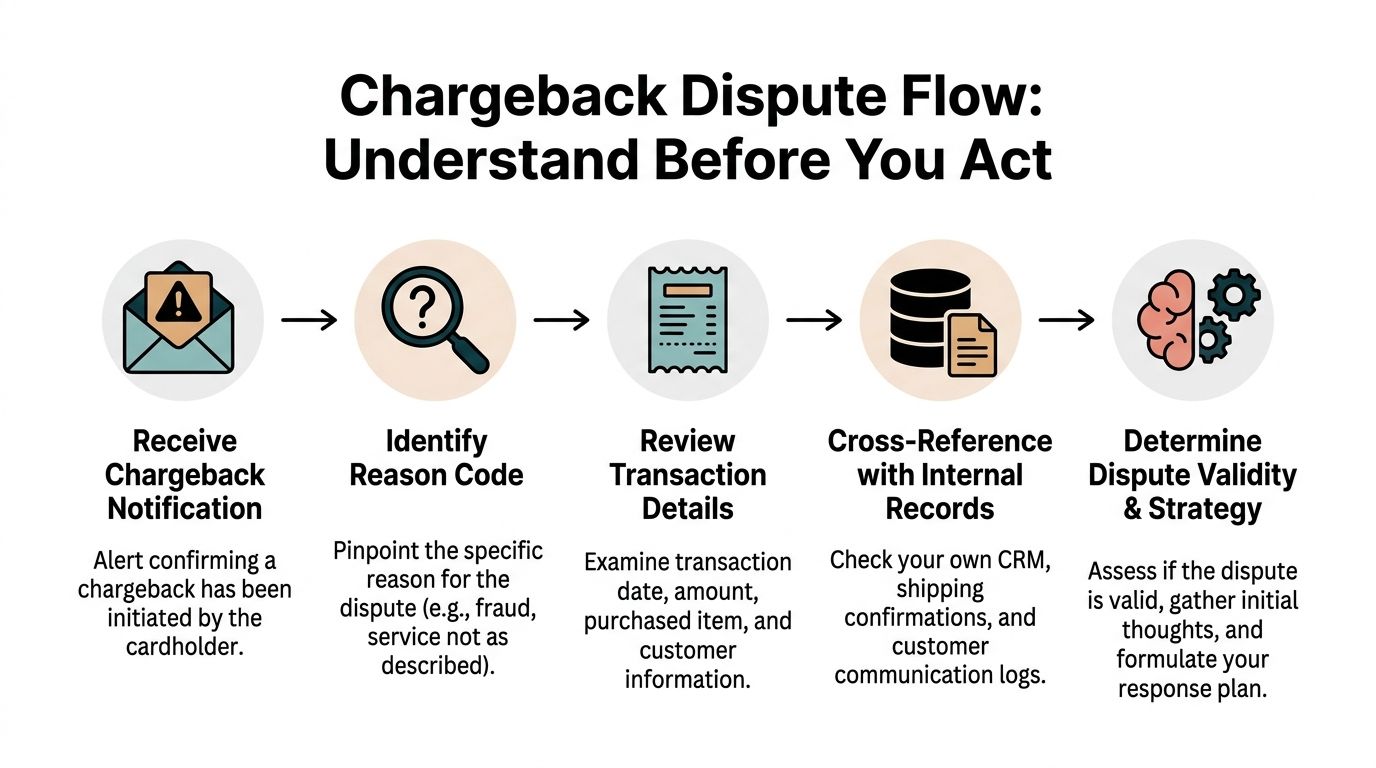

Decoding the Dispute Before You Respond

The worst move is firing off a generic rebuttal the same day the notice lands.

A good chargeback response starts with diagnosis. You need to know what the bank is accusing you of, what network rules apply, and whether the evidence in your system answers that claim.

Start with the reason code

The reason code tells you the bank’s stated basis for the dispute. That is your first clue, not your final truth.

If the code says fraud, do not submit shipping proof alone and hope for mercy. If the code says item not received, AVS and CVV by themselves will not carry the case. Match your response to the claim, not to your own frustration.

For a more detailed map of how the case moves through banks and processors, this overview of the card dispute process is useful.

Deadlines are not flexible

You must submit your chargeback response within strict network windows. For instance, card networks typically allow a few weeks for responses, with specific durations varying by network (e.g., some allow around 20 days, others up to 45 days). Prompt replies to initial retrieval requests can prevent up to 60% of them from escalating into formal chargebacks (Alexander Jarvis on chargeback win rate and response timing).

That means the first day matters. A lot.

If a retrieval request comes in, treat it like a live fire drill. Get the order data, invoice, delivery status, and customer contact history together immediately. Waiting because the dispute “isn’t official yet” is how small issues become expensive ones.

A practical triage workflow

I like a simple triage sequence:

- Confirm the deadline: Check the network, the date received, and the exact submission cutoff.

- Read the stated claim carefully: Fraud, not received, not as described, duplicate processing, canceled recurring billing, and similar claims each need different proof.

- Pull the order record: Order timestamp, items, billing and shipping details, payment checks, tracking, customer messages, and any refund history.

- Check for merchant error: If your team shipped late, refunded partially without clarity, or sent the wrong item, be honest about that before you waste time on a weak representment.

- Choose the path: Accept valid disputes. Fight invalid ones. Do not blur the two.

What reason-code reading looks like

Here is how I think about common buckets:

- Fraud claims: Look for authorization signals, device consistency, IP clues, order history, account age, and post-purchase behavior.

- Item not received: Focus on carrier scans, delivery confirmation, signature proof if available, and customer communication about delivery.

- Not as described: Use product page copy, variant details, photos, return policy language, and any service or support thread showing what was delivered.

- Canceled transaction or subscription issue: Pull cancellation logs, renewal notices, billing terms, and messages showing the customer’s awareness.

Do not overcomplicate this. The question is simple. What exact evidence would make a reviewer say, “Yes, this order was legitimate,” or “Yes, this merchant fulfilled what was promised”?

Tip: If your internal notes are messy, fix that before the next dispute arrives. A clean timeline wins more cases than a passionate argument.

Do not let the bank define the full story

Reason codes are necessary, but they are not always precise. A customer might choose a fraud path because it is easier than admitting buyer’s remorse or a missed support email.

That is why your early review should include context. Did the customer ask for a refund first. Did they log into the account after delivery. Did they place repeat orders. Did they confirm receipt and then reverse course. Those facts often matter more than the short label attached to the case.

A strong chargeback response starts before the rebuttal letter. It starts when you stop reacting and start diagnosing.

Building Your Unbeatable Evidence Package

Most merchants lose winnable disputes because they submit proof that is technically true but strategically useless.

Banks do not reward effort. They reward relevance. Your evidence package needs to answer the specific claim and close obvious gaps before the reviewer asks questions.

Friendly fraud and customer misunderstandings now drive over 70% of disputes. These erroneous chargebacks surged by 25% in 2025 and cost e-commerce businesses $25 billion globally. Initial issuer decisions favor the cardholder in up to 80% of cases, which is why contextual evidence matters so much (OlaPay on handling chargeback disputes effectively).

The rule I use for evidence

Do not send everything. Send the right things in the right order.

A reviewer should be able to see the case in one pass:

- the order was placed intentionally

- the payment checks passed

- the customer received what they bought, or had access to it

- your store communicated clearly

- the dispute claim conflicts with the transaction record

Essential Evidence Checklist for Chargeback Responses

| Evidence Type | Why It Matters | Best For (Reason Codes) |

|---|---|---|

| Order confirmation | Shows the customer completed a purchase and received the order summary | Fraud, canceled transaction, misunderstanding |

| AVS and CVV results | Supports that billing details matched and the card check passed | Fraud-related disputes |

| Device, IP, and session data | Adds context that the order came from a consistent user environment | Fraud, friendly fraud |

| Shipping confirmation and tracking | Proves fulfillment happened and shows carrier movement | Item not received |

| Signed proof of delivery | Stronger delivery evidence when available | Item not received |

| Customer service emails or chat logs | Shows the customer knew about the order, asked questions, or acknowledged receipt | Friendly fraud, not as described, misunderstanding |

| Product page copy or variant details | Proves what was advertised and what the buyer selected | Not as described |

| Refund and return policy records | Shows the terms available at purchase and any attempt to resolve directly | Canceled transaction, return-related claims |

| Prior order history | Helps show repeated legitimate purchasing behavior | Friendly fraud, fraud claims |

| Usage or access logs for digital goods | Shows the buyer accessed the product or service after purchase | Digital goods, subscription disputes |

Evidence by dispute type

Fraud claims

Merchants often under-submit here. They attach the receipt and hope that proves authorization. It does not.

You want signals that tie the cardholder to the transaction. Start with AVS and CVV results. If you need a refresher on how one part of that works, read this guide to AVS address verification. Then layer in IP location consistency, device fingerprint clues, customer account history, and post-purchase actions.

Helpful context can include:

- Repeat buying behavior: Same customer, same account pattern, earlier successful orders.

- Post-purchase engagement: Opened order emails, logged in, contacted support about sizing or shipment, downloaded digital content.

- Shipping alignment: Shipping address fits the broader customer profile rather than looking random or mismatched.

If the cardholder says “I never made this purchase,” your package should show why that claim does not fit reality.

Item not received claims

Carrier proof matters more than emotion here.

Use tracking status, delivery scans, delivery date, and signature proof if you have it. If the customer emailed support after delivery asking about usage, returns, or exchanges, include that too. It places them in possession of the order.

What not to do: submit only a label creation screenshot. That proves you intended to ship, not that the customer received anything.

Not as described claims

This category is about expectation matching.

Show the product page, selected variant, photos, sizing or spec details, and support messages. If the customer never contacted you before filing the chargeback, that can help establish that they skipped normal resolution channels.

This is one place where a simple timeline works well:

- Order placed with chosen variant

- Confirmation sent

- Item shipped and delivered

- Customer contacted support, or did not

- Dispute filed despite the documented order details

Subscription and recurring billing disputes

These cases usually turn on disclosure and customer awareness.

Your package should show the billing terms presented at purchase, renewal reminders if sent, cancellation path, account access history, and any customer messages about the subscription. If the customer used the service after renewal, that context matters.

Build the story, not just the file stack

Evidence wins when it tells a clean story.

A weak package is a pile of screenshots. A strong package arranges those screenshots so the reviewer understands the transaction without doing detective work. Put the most persuasive documents first. Label them clearly. Keep dates consistent. Remove duplicate files and irrelevant noise.

Tip: Every document in your package should answer one question. If it does not help prove authorization, fulfillment, disclosure, or customer awareness, cut it.

What merchants forget in friendly fraud cases

Friendly fraud is slippery because the order often looks normal. The card was real. The address was real. The delivery happened. The buyer changed the story after the fact.

That is why contextual evidence matters so much. The strongest packages often include small details that look ordinary on their own but become convincing together:

- The customer used the same email across prior orders

- They replied to a shipping update

- They asked a post-delivery product question

- They tried a refund route before escalating

- Their account activity continued after the alleged problem

None of that is dramatic. It is hard to argue with when presented clearly.

Your job in a chargeback response is not to sound offended. It is to make the invalid claim look logically unsustainable.

Writing a Clear and Persuasive Representment Letter

A strong evidence package can still fail if your letter is rambling, angry, or vague.

The representment letter is not the place to vent about banks, fraud, or how unfair this all feels. It is a cover note that helps a busy reviewer understand what happened and why your evidence disproves the claim.

Keep it short and factual

I prefer a letter that can be scanned quickly. State the transaction details, identify the disputed claim, summarize the counter-evidence, and point the reviewer to the attached documents.

Do not over-explain. Do not accuse the customer of lying unless the evidence is overwhelming and your phrasing stays professional. Your goal is credibility.

Bad version versus good version

Bad example

“We strongly disagree with this ridiculous chargeback. This customer is obviously trying to scam us after we already fulfilled the order perfectly. We have tons of proof attached and we expect this to be reversed immediately.”

This fails for three reasons. It is emotional. It is nonspecific. It makes the reviewer do all the work.

Good example

“Order #4821 was placed on the customer’s account using matching billing verification results and was shipped to the address provided at checkout. The package shows confirmed delivery, and the customer later contacted support from the same email used on the order. Attached records show authorization, fulfillment, and post-purchase account activity that contradict the dispute claim.”

That works because it is calm and structured. It points to the facts without drama.

A template you can use

If you want a starting point, this rebuttal letter template is a practical reference.

Here is the structure I recommend:

Subject line

Chargeback response for order [order number]

Opening

State that you are disputing the chargeback and identify the transaction.

Transaction summary

Include purchase date, amount, customer identifier, item or service purchased, and delivery or access status.

Reason claim summary

Briefly restate the issuer’s claim in neutral language.

Your rebuttal

Use a few sentences to explain why the claim is incorrect. Reference the strongest pieces of evidence only.

Evidence list

Name the attachments in a logical order.

Closing

Request reversal based on the attached records.

What to avoid in the letter

- Long backstory: The reviewer does not need your whole support history if two screenshots answer the issue.

- Angry language: It weakens your position.

- Unlabeled attachments: If the evidence file names are a mess, your case feels messy too.

- Claims without support: If you say the customer received the item, attach the delivery proof right behind that statement.

A short educational walkthrough can help if you want to see how merchants think through the writing side of disputes:

The letter should guide the evidence

Think of the representment letter like the index card on top of a case file.

It should tell the reviewer what happened, where to look, and why the conclusion should go your way. That is it. If your evidence package is the engine, the letter is the steering wheel.

Key takeaway: Good chargeback responses do not sound brilliant. They sound organized.

When to Stop Fighting Manually and Automate with AI

There is a point where manual chargeback work stops being disciplined and starts being expensive self-sabotage.

Manual chargeback handling costs an estimated $100 to $300 per dispute in staff time and tools. Manual win rates hover at 20% to 40%, and high chargeback ratios can trigger processing fee hikes of up to 5% (Merchant Advisory Group on getting chargebacks reversed).

The math changes fast

If your team spends hours on each case, low-value disputes become a trap. You can be “fighting back” and still losing money.

This is common in subscription brands, digital products, and any business with recurring support load. You see the same pattern in other payment-heavy industries too. Operators evaluating tools like gym payment software often run into the same problem. Payment admin expands until it starts eating margin and staff attention.

Signs manual handling is no longer working

You do not need a formal audit to know the process is broken. Look for these signals:

- Deadlines feel stressful every time: That means evidence is scattered.

- Only one person knows how to respond: That is a key-person risk, not a system.

- Your team skips small disputes: Reasonable on the surface, but it can hide process weakness.

- Win quality varies by staff member: Good outcomes should not depend on who happened to open the email that day.

What automation should do

An effective automation layer should not just send reminders. It should help with the work that burns time and introduces errors:

- pull order data from Shopify

- organize evidence by dispute type

- draft the representment response in the right format

- submit before the deadline

- maintain a clean record of outcomes and reusable proof patterns

One factual example in this category is ChargePay, which handles automated chargeback responses for Shopify merchants. It is described as achieving a high win rate across many cases, recovering substantial amounts, and holds a strong rating with a 'Built for Shopify' badge. It is positioned with pay-per-win pricing. Those details matter because merchants do not need another dashboard. They need fewer lost disputes and less admin.

My opinion is simple. Once chargebacks start pulling founders or ops managers away from growth work, manual handling is the expensive option, even if the software line item looks cheaper on paper.

When I would still handle some cases manually

There are a few exceptions:

- a very low volume store with rare disputes

- a one-off edge case where the internal context is unusual

- a team already running a disciplined process with centralized evidence and fast submission

But once volume rises, manual work breaks down in predictable ways. Files go missing. Letters get rushed. Deadlines slip. The same avoidable errors show up again.

Automation is not about convenience. It is about building a chargeback response process that does not collapse when the queue gets busy.

Answering Your Top Chargeback Response Questions

A few chargeback questions come up over and over. Here are the answers merchants usually need once they start taking dispute management seriously.

What happens if I lose the initial chargeback response

You have to decide whether to accept the loss or continue if the case escalates.

That next stage can involve pre-arbitration, where the issuer pushes the dispute back with additional information or a revised argument. At that point, do not resend the same package. Review the updated claim and ask whether you have new evidence or stronger context that directly answers it.

If you do not, accept the situation and move on. Throwing more time at a weak second-round case is a bad operating decision.

Tip: Save your strongest energy for disputes where the facts are solid, the value is meaningful, and the documentation is complete.

Should I fight every low-value dispute

Not manually. That is how teams create busywork and call it discipline.

A low-value chargeback can still matter if it affects your overall dispute profile, but the labor cost changes the equation. If your process requires humans to gather files, write the letter, and chase deadlines one by one, some cases will not justify the effort.

Automation changes that decision because the marginal effort drops. If the system can assemble the evidence and respond quickly, more cases become worth contesting. If the system cannot do that, be selective and honest about why.

Can a customer file another chargeback after I win

Disputes can come back in escalated forms depending on what the issuer or cardholder does next.

The important point is operational, not theoretical. Keep the full file even after you win. Preserve the order timeline, communication records, delivery proof, and your submitted rebuttal package. If the case reappears, you will need that history fast.

If your records live across inboxes, chat apps, help desk threads, and exported screenshots, you are making repeat disputes harder than they need to be. Centralize everything. If you want broader help on recurring questions around workflows, deadlines, and dispute handling edge cases, the ChargePay FAQs are a useful reference point.

What is the biggest mistake merchants make in a chargeback response

They argue the truth instead of proving the claim wrong.

Those are not the same thing. You may know the customer is abusing the system. The bank does not care about your certainty. It cares about documentation that fits the reason code and shows a clear, supported timeline.

That is why strong chargeback responses feel boring. They are specific, organized, and easy to review. Boring wins.

If chargebacks are eating revenue, time, and attention in your Shopify store, take a look at ChargePay. It automates the chargeback response workflow, submits evidence before deadlines, and only charges on wins. You can install it from the Shopify App Store.

.svg)

.svg)

.svg)

.svg)