A big order lands in Shopify. The billing name looks normal, the cart value makes your day, and then the little warning lights start flashing in your head.

Shipping and billing don't quite line up. The customer used an email you've never seen before. The order is expensive enough that if it turns into a chargeback, it won't just sting. It'll wipe out margin, inventory, shipping, and a chunk of your time.

That's the moment customer identity verification stops being a compliance term and becomes a profit decision. You're not trying to be paranoid. You're trying to answer a simple question before you ship. Is this a real customer, or are you about to donate product to a fraudster?

That Sinking Feeling When a Huge Order Looks Too Good to Be True

Every Shopify merchant knows this feeling. A high-value order comes through and you want to approve it fast, but the details don't sit right.

A lot of chargebacks start exactly there. Not with an obvious scam, but with an order that sits in the gray area long enough for someone to click fulfill and hope for the best. Hope is expensive.

Why this gets messy fast

Fraud screening inside Shopify can catch some issues, but it won't answer the full identity question on its own. A card can authorize and still belong to someone other than the person placing the order. A customer can look normal on the surface and still be using stolen credentials, a synthetic identity, or a throwaway setup designed to disappear after delivery.

That's why good stores build a second decision layer. Not for every order. For the ones that can hurt.

Practical rule: If canceling a suspicious order would feel painful, fulfilling it without verification is usually riskier.

The point of customer identity verification isn't to make checkout harder. It's to give you enough confidence to do one of two things cleanly: approve the order and ship, or cancel it without second-guessing yourself later.

The real cost isn't just the lost order

When fraud slips through, the chargeback is only part of the damage. You also lose inventory, pay shipping, deal with support tickets, and spend time digging through order notes trying to build a defense after the fact.

Merchants who deal with repeat abuse often end up creating manual workarounds. They blacklist names, block zip codes, and watch the same scam patterns come back with small variations. If that sounds familiar, this guide on how to blacklist, block, and ban scammers on Shopify is worth keeping handy.

What good verification gives you

Done right, verification gives you three things:

- Cleaner approvals: You stop canceling legitimate orders just because they look unusual.

- Cleaner declines: You reject bad orders before they become fulfillment losses.

- Cleaner evidence: If a dispute still happens, you're not scrambling to explain what happened.

That last part matters more than most merchants realize. If you ever have to defend a transaction, the difference between “the card passed” and “we verified the customer behind the order” is huge.

What Customer Identity Verification Actually Is

Think of payment authorization as the bartender checking whether the card works. Think of customer identity verification as the bouncer checking whether the person holding that card is who they claim to be.

Those are not the same job.

A card can be valid, funded, and approved by the issuer. That still doesn't prove the customer is legitimate. Customer identity verification is the process of checking the person, not just the payment method.

What sits inside a verification flow

Modern verification usually combines several checks. Leading overviews describe a layered process that can include document verification, biometric authentication, database checks, knowledge-based authentication, and multi-factor authentication, usually after collecting basics like name, date of birth, address, and a valid ID. Automated systems can compare a selfie to an ID document, cross-check databases, and return an approval, rejection, or manual-review outcome in seconds to a few minutes, depending on risk and human review needs, as described in this customer identity verification overview from 1Kosmos.

That layered setup matters for e-commerce because one signal rarely tells the whole story. An expensive cross-border order from a new customer may need more than AVS and a card authorization. If you want a quick refresher on where address matching fits in, this breakdown of AVS address verification is useful.

Why this became a core business function

This used to feel like something only banks and regulated companies worried about. That's no longer true.

One market forecast valued the identity verification market at $13.75 billion in 2025, rising to $15.84 billion in 2026 and projected to reach $50.58 billion by 2034, with North America accounting for 31.50% of global revenue in 2025, or about $4.33 billion, according to Fortune Business Insights on the identity verification market. Another forecast put the sector at $14.34 billion in 2025 and $29.32 billion by 2030, implying a 15.4% CAGR over that period, while another report estimated $18.8 billion in 2026 and $29.0 billion by 2030.

Those numbers tell you something simple. Verification isn't a niche add-on anymore. It's now part of the operating stack for digital commerce.

Good verification does two jobs at once. It blocks bad actors and gives legitimate buyers a safer path to complete the order.

If your store also relies on external systems to route products, pricing, or order actions, it helps to understand how identity checks fit into broader commerce automation. Zinc's explanation of an Ecommerce API is a good example of how more stores are connecting decision systems behind the scenes.

The 5 Main Types of Customer Verification

Shopify merchants don't need every verification tool. They need the right mix for the kinds of orders they get.

The easiest mistake is treating every method like a silver bullet. None of them are. Modern systems work best when they combine signals. That's also why automated verification has moved so far beyond manual review. Systems can now compare a selfie to an ID, cross-check databases, and use OCR and facial recognition to reach a decision quickly, as covered earlier from 1Kosmos.

The quick comparison

| Customer Verification Methods Compared | Customer Friction | Best For | Effectiveness |

|---|---|---|---|

| Email or SMS OTP | Low to medium | Basic step-up checks on unusual orders | Useful for lightweight confirmation, weaker against determined fraud |

| Device fingerprinting | Low | Repeat customer behavior, hidden risk screening | Helpful as a passive signal, not enough on its own |

| Two-factor authentication | Medium | Account logins, account changes, high-risk customer actions | Stronger than passwords alone, limited if account is already compromised |

| Document verification | High | High-value orders, resale risk, first-time risky buyers | Strong when you need proof of identity |

| Biometric checks | High | Very high-risk orders, dispute-ready evidence | Strong when paired with ID checks and liveness controls |

Email and SMS one-time passcodes

This is the lightest version of step-up verification. The customer gets a code and enters it to prove they control the email address or phone number attached to the order.

For Shopify stores, this works best when something is slightly off but not alarming. Maybe it's a first-time buyer with a higher-than-average cart, or a customer rushing an order to a forwarding address. An OTP won't prove legal identity, but it can help weed out sloppy fraud attempts.

What it doesn't do well is stop a fraudster who already controls the contact method they entered.

Device fingerprinting

This is mostly passive. The customer often doesn't notice it at all.

The system looks at device and browser characteristics, then uses that context as a risk signal. For merchants, this is valuable because it adds information without adding checkout friction. If the same device has a messy pattern across multiple orders or doesn't fit the claimed customer profile, that's worth a second look.

Two-factor authentication

Two-factor authentication is usually better known for login protection, but it also matters for account actions tied to orders. If a customer logs in, changes their address, and places an expensive order right after, 2FA can help confirm the account owner is really the one making that move.

If you're sorting out where authentication fits relative to card protections, this guide on 3-D Secure authentication helps clarify the difference.

A valid login is not the same as a trustworthy order. Fraudsters love accounts that already look familiar.

Document verification

At this stage, you ask the customer to upload a government ID or similar document. The system checks the document, reads it with OCR, and looks for signs of tampering.

For a Shopify merchant, this is usually reserved for orders where the loss would hurt enough to justify the friction. Luxury items, electronics, limited drops, and bulk purchases all fit.

It's more intrusive than an OTP, but it gives you far better evidence when the order later gets challenged.

Biometric checks

This usually means a selfie check matched against the submitted ID, often with liveness detection added. That extra liveness layer matters because a plain face match is easier to spoof.

For merchants, biometric checks make sense when you need stronger assurance before releasing expensive or fast-reselling goods. They're not something you throw at every customer. They're a tool for the orders that deserve closer inspection.

Matching Verification Strength to Order Risk

A one-size-fits-all verification policy is how stores lose on both sides. You either annoy good customers with unnecessary hoops, or you keep things so loose that fraud walks straight through.

The better approach is simple. Match verification strength to order risk.

What low-risk looks like

A returning customer buys a low-priced item. Billing and shipping line up. The device looks normal. Nothing in the order history suggests abuse.

That order probably doesn't need anything beyond your normal checkout controls. If you force that shopper through ID checks, you're creating friction where none was needed.

What high-risk looks like

Now compare that to a first-time buyer placing a costly order, sending it to a different address, paying with urgency, and using contact details that don't connect cleanly.

That's the order where merchants get into trouble by treating “approved payment” as “safe to ship.” It isn't.

This is also where fraud has evolved. Synthetic identity fraud is a fast-growing threat in the U.S. The Federal Reserve has reported it as one of the fastest-growing financial crimes, and guidance highlighted by ComplyCube stresses that businesses should combine document checks, biometrics, device intelligence, and risk scoring because no single signal is enough against AI-assisted fraud, as explained in this analysis of customer identity verification challenges.

A short explainer can help if you want a visual walkthrough of how risk-based review works in practice.

A practical risk ladder

Use your verification tools like levels, not like an on-off switch.

- Low-risk orders: Let them pass with standard checkout controls.

- Medium-risk orders: Add a light step-up, such as OTP or a manual review before fulfillment.

- High-risk orders: Ask for stronger proof, such as document verification or a selfie-plus-ID flow.

- Very high-risk orders: Don't be afraid to cancel if the customer resists reasonable verification or the signals keep stacking up.

Signals worth paying attention to

Not every odd detail matters. Patterns do.

- Address mismatch: Billing and shipping don't align, especially on expensive items.

- New-customer pressure: First order, high value, rush shipping.

- Behavior that doesn't fit: Multiple attempts, repeated declines, or rapid changes in cart behavior.

- Weak contact identity: Throwaway-looking email, inconsistent phone details, or odd account history.

- Reseller-friendly products: Items that are easy to flip often deserve tighter review.

If an order would trigger a refund policy exception, insurance concern, or inventory panic after a chargeback, it probably deserves stronger verification before shipment.

How to Implement Verification on Your Shopify Store

Most merchants overcomplicate this part. You don't need to turn your whole checkout into a bank onboarding flow.

You need a workflow that isolates risky orders, applies extra checks only when needed, and leaves normal customers alone.

Start with order tagging

Shopify Flow is the easiest place to begin. Build automations that tag orders for review when they hit your store's risk conditions.

Examples:

- High-value tag: Flag orders above the threshold that would materially hurt if lost.

- Mismatch tag: Mark orders where shipping and billing details diverge in ways you care about.

- New-customer tag: Flag first-time buyers ordering high-risk products.

- Velocity tag: Surface clusters of purchase attempts or repeated retries.

Once an order is tagged, you can route it into a manual review queue or trigger a verification request through the app you use for fraud checks. That keeps your standard checkout clean.

Keep friction surgical

Many stores go wrong by applying the same policy to everyone because it feels simpler.

It isn't simpler once conversions drop or support starts fielding angry emails from legitimate customers. A better setup asks only the next reasonable question. If a light check clears the order, stop there. If the order still looks off, escalate.

One small but useful upstream step is verifying contact quality before fraud even becomes a dispute problem. If your team is comparing tools for that, this guide on choosing an email validation API gives a practical way to think about bad email data.

Build a review playbook your team can follow

Write down what happens when an order gets flagged. Don't leave it to guesswork.

A simple playbook might look like this:

- Check Shopify signals first: Review the order timeline, customer history, and basic mismatch indicators.

- Request step-up verification: Ask for the least intrusive check that fits the risk.

- Escalate only when needed: Move to ID or biometric proof for high-exposure orders.

- Document the outcome: Save approvals, communications, and verification results in one place.

If you're adding controls around risky segments, this overview of a fraud filter app for Shopify can help you think through where automated rules should sit versus where humans should review.

Don't forget the customer experience side

Legitimate buyers will usually cooperate if the request makes sense. The key is how you frame it.

Tell them the order triggered an extra security review to protect both sides. Keep the request short. Give clear instructions. And move quickly. Merchants create a lot of their own friction by asking for verification, then taking too long to respond once the customer completes it.

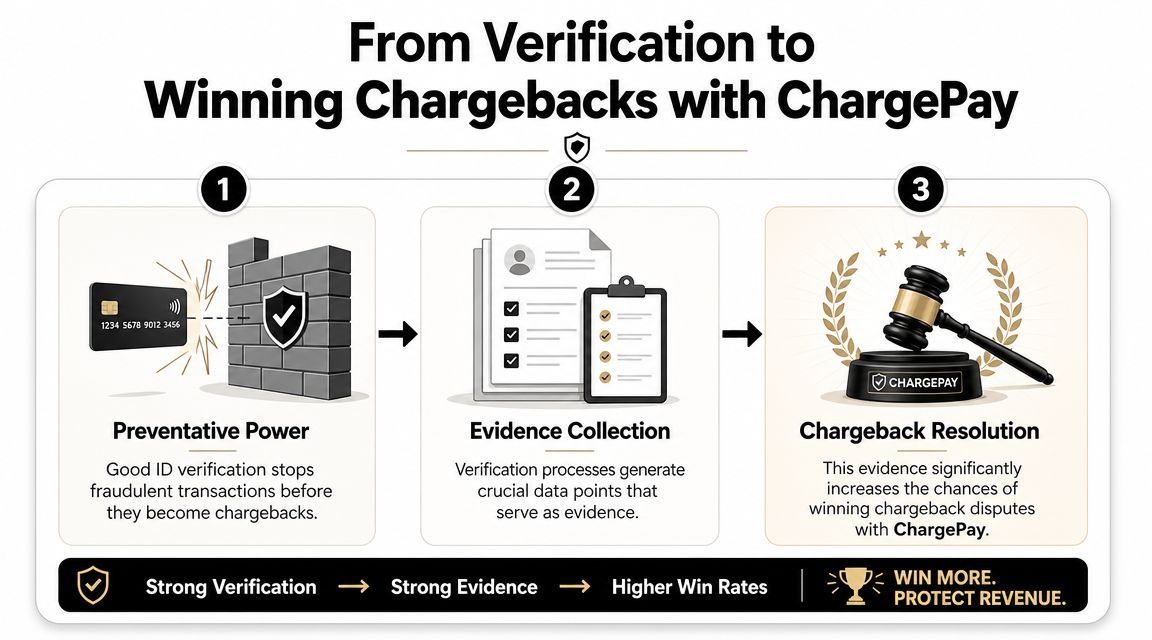

From Verification to Winning Chargebacks with ChargePay

Good verification prevents some chargebacks before they happen. It also does something just as important. It creates evidence while the order is still fresh.

That matters because disputes are often won or lost on what you can prove, not what you believe happened.

Why verification records matter in a dispute

If a customer later claims they didn't authorize the purchase, your defense gets stronger when you can show more than a payment approval. Verification logs, successful step-up checks, identity documents, and customer communications all help establish that the order came from a real person who completed deliberate actions.

Leading providers often separate passive and active checks. Active flows can include a biometric selfie check that compares the face to a government ID and applies liveness detection to spot replay attacks or deepfakes. As Telesign explains in its guide to customer identity verification, that level of evidence can be powerful in a chargeback dispute.

Prevention helps, but it won't stop friendly fraud

This is the part merchants learn the hard way. You can verify an order properly and still get hit with a dispute later.

Some customers forget the purchase. Some don't recognize the descriptor. Some know exactly what they're doing and file anyway. That's why verification should feed directly into your dispute process. If the evidence sits in five different tools and nobody pulls it together before the deadline, you still lose.

Your representment process needs to be fast, organized, and built around the strongest proof available. If you want a better sense of what that package should contain, this guide to chargeback representment is a solid starting point.

The best time to collect dispute evidence is before the package ships, not after the chargeback arrives.

The practical takeaway

Customer identity verification is worth doing for two reasons. First, it helps you stop bad orders before they become losses. Second, it gives you cleaner records for the disputes you can't prevent.

Merchants who treat verification as part of chargeback defense usually make better fulfillment decisions. They ship fewer bad orders, they cancel with more confidence, and they're in a much stronger position when a bank asks what proof they have.

If chargebacks are eating margin, ChargePay is the cleanest next step. It's built for Shopify merchants, has a 4.9-star rating and a Built for Shopify badge, and it automates the ugly part of the process by building and submitting dispute responses for you. ChargePay reports a 92.4% win rate, has handled 100K+ disputes, and recovered $2.8M+ for merchants. Install it from the Shopify App Store and turn your dispute process into something that gets your money back.

.svg)

.svg)

.svg)

.svg)