Flex rent, which you likely know as Buy Now, Pay Later (BNPL), lets your customers break down a purchase into smaller, more manageable payments. It’s like a modern layaway, but they get the product right away, and you get the full payment upfront from the BNPL provider.

What Is Flex Rent and Why It Matters for Your Shopify Store

For Shopify store owners like you, offering flex rent can be a great way to increase your conversion rates and average order value. Think about it: when a customer sees they can split a $400 purchase into four simple payments of $100, that "add to cart" click gets a lot easier. The BNPL company, such as Afterpay or Klarna, pays you the full $400 immediately (minus their fee) and handles collecting the payments from the customer.

Sounds like a clear win, right? But here’s the catch, and it’s a big one that many store owners miss. While the provider deals with the customer's payment defaults, you are still on the hook for chargebacks. Since each installment is a separate transaction, you suddenly have multiple new chances for a customer to file a dispute. That payment flexibility you offered to boost sales can quickly turn into a revenue leak. Flex Rent is a major shift in how payments are handled and fits into the evolving payment landscape where convenience and risk go hand-in-hand.

At ChargePay, we see this happen every single day. We've managed over 100,000 disputes and recovered more than $2.8 million for Shopify merchants, and a growing number of those disputes come from these installment plans. The very design of flex rent creates unique chargeback problems, especially with friendly fraud.

A customer might pay the first two installments for a product they love. Then, they dispute the third or fourth payment, claiming it was unauthorized or they weren't happy with it—all while keeping the item they received. These are the kinds of disputes that quietly drain your profits.

Figuring out how to handle this double-edged sword is crucial. You want the extra sales, but not the financial hit from the disputes that follow. In this guide, we’ll walk you through how flex rent really works, where the hidden risks are, and what you can do to protect your revenue. Knowing all the ways customers can pay is key, and you can learn more about other alternative forms of payment and what they mean for your business. Our goal is to give you the confidence to offer flex rent, armed with a solid strategy to fight the chargebacks that will come.

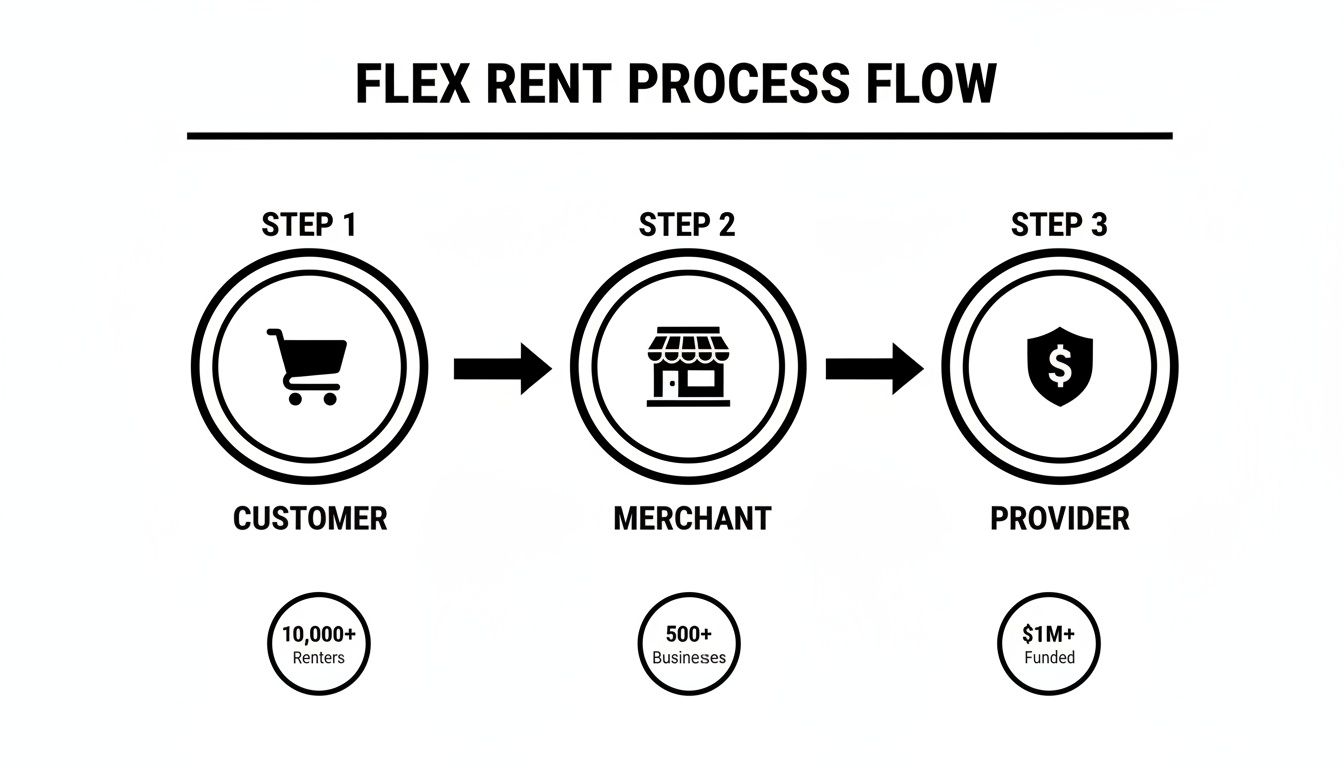

To really understand how flex rent works, let's walk through a typical purchase, looking at it from your customer's side and then from yours. On the surface, it seems simple, but the behind-the-scenes mechanics are where the chargeback risks start to pile up. It’s completely different from a normal credit card sale.

For your customer, the experience is incredibly smooth. They find an item they love, add it to their cart, and head to checkout. There, they see an option like Klarna or Afterpay, select it, and get an approval decision almost instantly. They pay the first slice of the price—say, $25 on a $100 purchase—and their order is confirmed. The rest of the payments are then automatically charged to their card on a set schedule. Easy.

But for you, the Shopify merchant, things are a bit more involved. This is where you need to pay close attention.

Your Side of the Transaction

The flex rent company pays you, the merchant, the full purchase price right away, after taking out their fee. For that same $100 order, you might see $94 land in your account almost immediately. The provider, meanwhile, takes on the responsibility of collecting the remaining $75 from the customer over the next few weeks.

When you look at your Shopify dashboard, you'll see this transaction isn't listed like a typical Visa or Mastercard payment. It will be clearly marked as a payment from the flex rent provider. This small detail is very important because how you handle returns and disputes for these orders is completely different.

This flow chart breaks down how the money and the product move between the three parties involved.

The key takeaway here is simple: while the customer gets to enjoy their product and pay for it over time, you get your money upfront from a third party. This adds a new, and sometimes tricky, layer to the whole payment process.

The Lifecycle and Potential Pitfalls

Once you understand this transaction flow, you can start to see where the chargeback vulnerabilities pop up. The biggest risk isn't that the customer will stop paying—the provider takes on that headache. The real danger for you is when a customer disputes one of the later installments.

Imagine a customer buys a $200 item from your store. They pay their first two installments of $50 each with no problem. But a month later, buyer's remorse kicks in. They decide they don't want it anymore and dispute the third $50 payment with their bank, claiming the charge was unauthorized.

This is a classic case of "friendly fraud," and the flex rent model can unfortunately make it easier for this to happen. Since the provider paid you the full amount weeks ago, that $50 chargeback now comes directly out of your pocket.

Optimizing your store's payment process is key, and you can learn more about that in our guide to the Shopify checkout process. Managing these delayed disputes is where many merchants lose money without even realizing what's causing it. This is exactly the problem ChargePay was built to solve, helping merchants like you fight back with our 92.4% dispute win rate.

Understanding the True Cost of Flex Rent

Offering flexible payment options is a great way to boost sales, but let's be direct—it's not free. There are costs involved, both for your customer and for you, the merchant. For a shopper, a missed payment can quickly lead to late fees, turning what seemed like a good deal into a financial headache. But for your Shopify store, the costs hit your bottom line right away.

Flex rent providers, or BNPL services, almost always charge a higher fee per transaction than your typical credit card processor. While a standard credit card sale might cost you around 2.9% + 30¢, a flex rent provider could take a slice anywhere from 4% to 7% of the total purchase. It’s a trade-off: you get a potential lift in conversions and bigger cart sizes, but you pay a premium for every one of those sales.

The Impact on Your Profit Margins

Let’s run the numbers to see what this actually looks like. On a $200 sale, a regular processor might take about $6.10. But a flex rent provider charging 6%? That’ll cost you $12.00. That's nearly double the fee, eating directly into your profit margin before you even factor in shipping, marketing, or the cost of the product itself.

This is where most merchants stop their math. They weigh the higher fee against the extra sales and figure it's a worthwhile cost of doing business. But they often overlook a critical second cost—one that can wipe out those hard-won profits in an instant.

The higher your initial transaction fees, the more damaging a chargeback becomes. When you lose a dispute on a flex rent order, you don't just lose the product and the revenue—you also lose the non-refundable, higher processing fee you paid to make the sale in the first place.

This makes protecting every single dollar more important than ever. When your margins are already squeezed by higher fees, you simply can't afford to let friendly fraud and other disputes slide. Every chargeback isn't just lost revenue; it's also a sunk cost from the fee you paid upfront. As you can imagine, those extra percentages add up fast, and knowing how to calculate the total cost of a chargeback fee is vital to understanding your true profitability. That's exactly why having an automated defense like ChargePay, which has successfully handled over 100,000 disputes, becomes an essential part of your financial strategy when you offer flex rent.

Why Flex Rent Leads to More Chargebacks

Here's the catch every Shopify merchant needs to know. Offering flexible payments is a great way to boost sales, but it comes with a hidden risk: a direct increase in your store’s exposure to chargebacks. The very thing that makes "flex rent" so attractive to shoppers—spreading payments over time—also opens up more doors for disputes to walk through.

We aren't talking about traditional credit card fraud from stolen cards. The real threat here is something much trickier, known as friendly fraud. This is when a real customer buys a product, receives it, and then disputes a charge down the road.

Flex rent plans are the perfect breeding ground for this kind of trouble.

The Problem of Delayed Disputes

Think about a normal credit card purchase. It’s a single transaction. The customer either has a problem with it or they don't. But with a flex rent plan split into four installments, you suddenly have four separate chances for a dispute to pop up. A shopper who was thrilled with their purchase on day one might get a case of buyer’s remorse weeks or even months later.

Let’s walk through a real-world scenario.

You sell a high-end bicycle for $1,200. The customer is happy to pay in four monthly installments of $300. The first two payments go through without a problem. But just before that third payment hits, the customer decides they don't want to pay anymore. They call their bank, dispute the $300 charge as "unauthorized" or claim they're "dissatisfied" with the product, and they get to keep the bike.

This is where merchants get completely blindsided. The BNPL provider has already paid you the full amount, so when the customer files that chargeback, the money gets clawed back directly from your account. The customer just scored a 25% discount, and you're left holding the bag.

Confusion Over Recurring Billing

Another common trigger for disputes is simple forgetfulness. A customer might not remember they agreed to an installment plan. When a charge for $300 appears on their statement a month or two after the purchase, they don't recognize it. To them, it looks like a bogus charge, so they immediately dispute it.

This is a classic case of friendly fraud, and it happens far more often than you'd think. If you want to take a deeper dive into this topic, check out our complete guide on how friendly fraud impacts Shopify merchants.

Without a system to fight back, you’re stuck manually digging up evidence to prove the customer agreed to the payment schedule, received the item, and was notified about the upcoming charge. It's a time-consuming battle that most busy store owners simply can't win consistently.

To put it into perspective, take a look at how the risk profile changes with these payment models.

Flex Rent vs Traditional Payments Chargeback Risk Profile

This table breaks down the common triggers for chargebacks and how they compare between a standard one-time payment and a flex rent plan.

As you can see, the installment structure inherently creates more scenarios that can lead to a chargeback, even when there's no malicious intent from the customer.

At ChargePay, we see merchants lose thousands of dollars this way every month. It’s exactly why we’ve successfully recovered over $2.8 million for stores just like yours, hitting a 92.4% win rate by automating the entire complex evidence-gathering process for you.

How to Protect Your Store From Flex Rent Chargebacks

Alright, let's switch from just understanding the problem to actually fixing it. This is where you take back control. While flex rent plans can open up new avenues for chargebacks, you can absolutely take practical steps to shut those doors. The best place to start is with a solid, proactive defense checklist to protect your hard-earned revenue from these frustrating disputes.

The heart of your strategy comes down to one thing: crystal-clear communication. When things are vague, you're practically rolling out the red carpet for friendly fraud. From the very second a customer even thinks about buying, your payment terms need to be so obvious that they’re impossible to misunderstand.

A Practical Checklist for Prevention

Start putting these safeguards in place right away. Think of each one as another layer of protection, another piece of evidence that could be a lifesaver if a dispute ever pops up.

- Be Loud and Clear on Product Pages: Don't bury the installment plan details. Show the payment schedule right next to the price (for example, "4 interest-free payments of $25.00"). This sets the right expectations from the get-go.

- Double-Down at Checkout: Before the customer clicks that final "buy" button, show them the full payment schedule again—all the dates and all the amounts. A simple checkbox like, "I agree to the 4-payment schedule" can be incredibly powerful evidence later on.

- Send Friendly Reminders: Set up automated emails or texts to go out a few days before each installment is due. This simple step helps prevent those "unrecognized transaction" disputes from customers who honestly just forgot.

- Keep Your Paperwork Spotless: You should always have proof of delivery with tracking numbers and all your customer communications saved and easy to find. If a customer disputes a charge, this is your first line of defense.

To really get a grip on these situations, it's a good idea for merchants to have a solid base in understanding service contract disputes, because the same core ideas often pop up in these BNPL agreements.

Now, while these manual steps are a great start, they can become a real headache to manage as your store grows. Just imagine trying to manually track every single installment for hundreds of orders each month. It's just not practical. This is where automation becomes your new best friend.

Your Automated Safety Net

This is the exact problem we built ChargePay to solve. Our AI-powered tool is your automated safety net, designed to handle the entire dispute process without you having to lift a finger. As a 'Built for Shopify' app holding a 4.9-star rating, we're plugged directly into the platform you use to run your business every day.

The moment a flex rent dispute comes in, ChargePay’s AI gets to work, automatically pulling together all the evidence you need. This isn't just one or two things; it's the transaction data, the original payment agreement, shipping confirmations, proof of delivery, and any important customer chats. It builds a complete, bank-ready evidence package for you in real-time.

Instead of you spending hours digging through old emails and order logs, our system does it in a flash. We’ve successfully fought over 100,000 disputes, recovering more than $2.8 million for merchants just like you. This kind of automation means you can offer flex rent with confidence, knowing you have a powerful system ready to step in, fight for you, and win your money back.

For a deeper dive into what this level of protection can do for your store, check out our complete guide on chargeback protection for Shopify stores.

Turning Flex Rent Chargebacks Into Recovered Revenue

It’s easy to talk about the risks of flex rent in theory. But let’s look at how a real store can flip those risks into recovered cash.

Imagine you run a Shopify store selling high-end designer handbags. You decide to offer a flex rent option, and it works—sales climb higher than ever.

But soon, a new problem emerges. You start getting hit with a string of friendly fraud chargebacks. A customer pays three of the four installments, receives the handbag, and then disputes the final payment. Suddenly, you're out thousands of dollars each month, losing both revenue and your valuable product.

Overwhelmed by fighting every single case by hand, the store owner decided to install ChargePay. The difference was felt almost instantly.

From Revenue Drain to Automated Recovery

Our AI didn't just start fighting disputes—it started learning from them. It immediately got to work analyzing the store’s unique chargeback patterns, figuring out exactly why these flex rent disputes were happening. For every new case that came in, the system automatically put together the perfect evidence package.

This included critical pieces of proof like:

- The customer's original agreement to the installment plan at checkout.

- Proof of delivery, complete with tracking information confirming the handbag arrived safely.

- The full payment history showing the first few successful installments.

Within just a few weeks, ChargePay was consistently winning back those disputes. What was once a major revenue leak became a reliable stream of recovered profit. To date, we've successfully handled over 100,000 disputes for our merchants, recovering more than $2.8 million in total.

This isn’t just a success story—it's a clear path from losing money to getting it back on autopilot. The handbag store could finally offer flex rent with confidence, knowing a safety net was in place to protect their bottom line.

This also shows how our simple, no-risk model works. With ChargePay, you only pay us when we win. If we don't recover your money, you don't owe us a dime. It’s that straightforward.

This is how you solve the problem. Instead of viewing flex rent as a chargeback magnet, you can see it for what it is: a powerful tool to grow your sales. If that sounds like the peace of mind you've been looking for, Install ChargePay from the Shopify App Store and start protecting your revenue today.

Frequently Asked Questions About Flex Rent

If you're a Shopify store owner, you've probably heard the buzz around flex rent and have some questions. What does it actually mean for your business, your sales, and your bottom line? Let's clear up some of the common questions we hear from the thousands of merchants using ChargePay.

Is Flex Rent the Same as Buy Now Pay Later?

Yes, they're two names for the exact same thing. "Flex rent" is just another way of saying "Buy Now, Pay Later" (BNPL). It all comes down to letting your customers get their products right away and pay for them in smaller, manageable installments over time. You've definitely seen the big names out there, like Afterpay, Klarna, and Affirm.

Who Is Responsible if a Customer Defaults?

This is a big one. If a customer just stops making their payments, the BNPL provider (like Afterpay) eats that loss. They take on the credit risk, so you, the merchant, get to keep the full payment you received upfront.

But here's the catch: you are still responsible for handling any chargebacks a customer might file. If they dispute one of their installment payments with their bank, that dispute comes back to you.

Can I Fight Chargebacks From Flex Rent?

Absolutely, and you should fight every single one. These disputes can be a little tricky because they often require specific evidence showing the customer knew and agreed to the installment plan. This is exactly why having an automated system on your side makes a huge difference in winning them back.

Does Offering Flex Rent Increase My Fraud Risk?

It can, but not in the way you might think. The biggest risk isn't from stolen credit cards, but from friendly fraud. Because the payment structure is more complex than a simple one-time purchase, it opens the door for customers to get confused or have buyer's remorse and file a dispute. This makes having a solid dispute management process absolutely essential to protect your revenue.

Don't let the fear of a few complex disputes scare you away from boosting your sales with flex rent options. ChargePay has recovered over $2.8 million for merchants just like you, holding a 92.4% win rate across more than 100,000 disputes.

As a 'Built for Shopify' app with a 4.9-star rating, our AI handles the entire headache for you. Install ChargePay from the Shopify App Store and start turning those frustrating chargebacks into recovered revenue.

.svg)

.svg)

.svg)

.svg)