You check your Shopify payout, compare it to your sales, and the gap feels bigger than it should. You sold the product. You paid for inventory, shipping, and ads. Then the payout lands, and another slice disappeared into payment costs you didn’t really approve in any meaningful way.

A big part of that gap is the interchange fee credit card networks build into every card transaction. Most store owners know they pay “processing fees,” but many don’t realize interchange is usually the biggest piece of that total cost. It also gets more painful when your store starts dealing with chargebacks, because payment risk doesn’t just create one-off losses. It can push your business toward more expensive processing over time.

If you’re trying to understand where your margin keeps going, this is one of the first places to look.

The Biggest Fee Eating Your Shopify Profits

You don’t need a complicated finance background to spot the problem. A customer places an order. Shopify marks it paid. You mentally count the sale as revenue. Then the payout arrives lower than expected, and you start asking the same question most merchants ask: where did the rest go?

A large share of that missing money is interchange. These fees started in the 1960s and became the largest component of merchant fees. By 2008, total US interchange fees reached $48 billion, and merchants passed enough of that cost through pricing that households paid an average of $427 annually, according to a California Assembly report summarizing the history of interchange fees and merchant costs in the US interchange fee report.

For a Shopify merchant, this doesn’t feel like some abstract card-industry issue. It shows up in every order. If you’ve ever tried to sort out platform fees versus payment fees versus network costs, a practical starting point is this breakdown of how much Shopify takes per sale, which helps separate what Shopify charges from what the card ecosystem takes.

Why this fee feels invisible

Interchange rarely appears in a way that feels clear to a merchant. You usually see a bundled processing cost, not a neat line that says, “This part went to the customer’s issuing bank.”

That’s why so many owners underestimate it. They focus on ad spend or shipping, while payment costs impact every sale, often overlooked.

Practical rule: If your store accepts a lot of credit cards, interchange is not a side fee. It’s one of your baseline cost drivers.

Why chargebacks make this worse

The part many merchants miss is that interchange and chargebacks aren’t separate problems. They’re connected. If your store has more disputes, processors and networks may see more risk around your transactions, and that can affect what card acceptance costs you over time.

If you want a clearer picture of how these costs stack together on Shopify specifically, ChargePay’s guide to Shopify payment processing fees is useful because it breaks the fee layers into plain English.

That’s the core issue. You’re not just losing money on the occasional disputed order. You may also be protecting or hurting your future processing economics with every chargeback you win or lose.

What Exactly Is a Credit Card Interchange Fee

A customer places a $100 order on your Shopify store. The payment goes through. Your payout lands lower than $100, even though the order shipped normally and nothing looked unusual at checkout.

A large part of that gap is interchange.

Interchange is the fee paid to the customer’s card-issuing bank every time a card transaction is approved. It sits inside your total processing cost, which is why it often feels hidden. You usually see one blended payment fee, not a clear line showing how much went to the issuing bank.

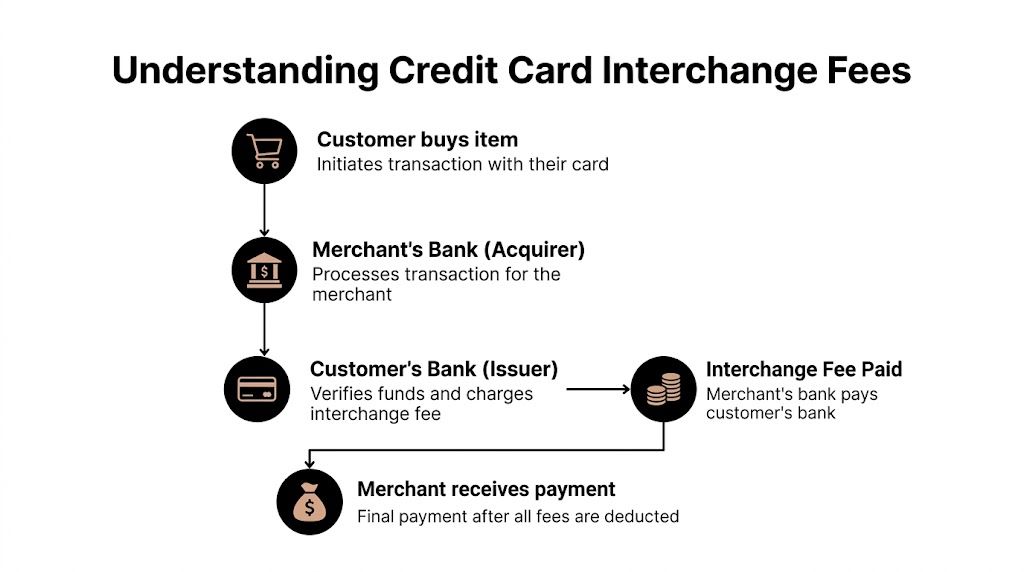

The four parties in every card sale

A card payment looks simple to the shopper. Behind the checkout button, four parties are involved:

The merchant

That’s your store. You submit the charge for approval.The acquirer

This is the merchant-side bank or processor that helps your store accept card payments.The card network

Visa, Mastercard, and similar networks set rules and route transaction messages between parties.The issuer

This is the customer’s bank, the one that issued the credit or debit card.

A useful way to picture it is a delivery route. Your customer starts the order. The acquirer passes the payment request through the card network. The issuer decides whether to approve it. If the transaction is approved, interchange is the issuer’s portion of the cost for participating in that transaction.

What interchange is, and what it is not

Store owners often lump every card cost into one bucket. That makes it harder to spot what is driving margin loss.

Interchange is only one layer of the total fee stack. It is usually the largest layer, but it is not the whole processing fee. Your full card acceptance cost can also include network assessments and processor markups.

So if a customer pays $100, the money does not move straight from the customer to your bank account. Part of it is carved out along the way, and interchange is the issuer’s share.

Why debit and credit do not cost the same

Debit and credit can look identical at checkout, but they follow different pricing rules.

One reason debit often costs less is regulation. The Federal Reserve explains in its overview of the Debit Card Interchange Fees and Routing rule under Regulation II that certain debit interchange fees for large issuers are capped under the Durbin Amendment. Credit cards do not have that same cap, which is one reason credit transactions often cost merchants more.

That difference matters on Shopify because you are not just paying for “a card payment.” You are paying based on the type of card the customer uses and the risk profile attached to it.

Why this matters more than it seems

Interchange is not just a payment term for accountants. It affects contribution margin on every order.

It also connects to chargebacks more than many merchants realize. The card system prices risk into transactions. If your business starts looking riskier because disputes rise, the pain is not limited to refunded orders, chargeback fees, or lost inventory. Higher perceived risk can put pressure on your processing economics over time, which makes dispute prevention and chargeback wins part of cost control, not just revenue recovery.

If you want a clearer view of who handles each step in the card flow, this guide on what a payment processor does in the transaction chain helps connect the roles without payments jargon.

Once you see interchange as the issuer’s cut of every approved card sale, the fee stops feeling random. It becomes a predictable cost driver you can measure, monitor, and work to contain.

How Your Interchange Fees Are Calculated

Interchange isn’t one flat number applied to every sale. Card networks use a schedule of rates based on risk, card type, and transaction details. That’s why two customers can each place a $100 order on your Shopify store and cost you different amounts to process.

For e-commerce, this matters because online transactions carry more uncertainty than in-person sales. You can’t physically inspect the card. You can’t verify the cardholder face-to-face. That makes card-not-present transactions riskier, and higher risk usually means higher interchange.

The biggest drivers behind your rate

Some factors are outside your control. Others are heavily influenced by how your checkout and operations work.

Card type matters

A standard consumer card may cost less than a premium rewards card. The shopper gets points or perks. You help fund that through higher processing costs.How the transaction happens matters

Online transactions generally cost more than in-store transactions because fraud risk is higher.Your business category matters

Networks sort merchants by category. Some industries are seen as riskier than others, and that can affect the interchange rate profile tied to your transactions.Your store’s dispute history matters

Mastercard’s merchant rate documentation notes that interchange is strongly tied to risk, and merchants with high chargeback rates can be re-categorized into higher-risk categories that trigger automatic rate increases on future transactions. It also shows example ranges where American Express rates can run from 2.3% to 3.5%, compared with Visa at 1.4% to 2.5%, reflecting different pricing and risk models in the market Mastercard merchant interchange rates.

A quick comparison

Below is a simple way to think about how rates can vary on the same order value.

| Card Type / Transaction | Example Interchange Rate | Cost on a $100 Sale |

|---|---|---|

| Visa credit transaction | 1.4% to 2.5% | $1.40 to $2.50 |

| American Express transaction | 2.3% to 3.5% | $2.30 to $3.50 |

Those ranges don’t mean your store will always land at one exact point. They show why your costs move depending on the card a customer uses and how the sale is classified.

Why chargebacks affect more than one order

A lot of merchants think of chargebacks as isolated losses. One customer disputes one order. You lose that order and move on.

That’s not how payment risk works in practice.

If your store starts showing a pattern of disputes, processors and networks may treat your business as riskier overall. When that happens, you’re not just dealing with a single painful event. You may be dealing with higher acceptance costs on future transactions too.

A chargeback can be a one-time loss. A worse risk classification can become an ongoing tax on every future sale.

Why your statement may still look confusing

Some merchants are on flat-rate pricing. Others are on interchange-plus pricing. Shopify merchants often see a bundled fee structure that doesn’t cleanly separate the network-driven parts from the processor markup.

That’s why fee analysis can feel frustrating. You’re trying to diagnose a cost problem using reports that weren’t built to teach you payments economics.

If you compare channels, tools like this PayPal transaction fee calculator can help you understand how different payment methods affect margin, even though the underlying fee structures aren’t identical.

The takeaway is simple. Interchange is calculated based on risk and transaction context, not just sale amount. If your store looks riskier, your payment costs can rise with it.

The Real-World Impact on Your Store's Margins

A customer places a $100 order on your Shopify store. You see the sale come through and start doing the mental math on profit. Then the payout lands lower than expected.

That gap is where interchange becomes real.

A $100 order does not mean $100 in your payout

On a typical credit card order, part of the transaction is carved out before the money reaches you. Interchange is one of the largest pieces of that deduction. It sits underneath the sale like a built-in toll.

So your $100 order has to cover more than the product itself. It also has to absorb:

- Your cost of goods

- Shipping and fulfillment

- Platform and acquiring fees

- Return and refund risk

- Dispute costs if the order turns into a chargeback

That matters because margin is not revenue. Margin is the thin layer left after every other hand has taken a piece.

For stores with healthy markups, interchange may feel manageable. For stores selling lower-margin products, paid-traffic products, or high-return items, it can erase more profit than the sale summary suggests.

Why online stores feel this pressure faster

Shopify merchants usually deal with card-not-present transactions. That brings extra friction compared with an in-store payment. You are paying for payment acceptance in an environment with more fraud screening, more fulfillment cost, and more chances for the order to unravel after checkout.

A simple way to look at it is this. Interchange reduces your cushion.

If your store also faces rising ad costs, frequent returns, or expensive shipping, that cushion gets very thin. A fee that looks small on one order can become a serious drag across hundreds or thousands of orders each month.

Some merchants respond by reviewing checkout and pricing. Others also examine whether certain alternative payment methods for ecommerce stores can reduce pressure on margins in the right situations.

Bottom line: interchange cuts into the amount of profit available to absorb normal ecommerce problems.

A quick visual explanation helps if you want to see how these fees stack up in an online sale:

When the order turns into a chargeback

The cost becomes more painful.

A disputed order can leave you without the revenue, without the product, and still stuck with the operational cost of processing and fulfilling the transaction. In many cases, the original payment costs do not unwind cleanly enough to make you whole.

Interchange works like an extra loss layer. You paid to accept the order, and then you paid again through the fallout of the dispute.

That is why a chargeback is not just a one-order problem on your P&L. It is a margin event.

Why this changes how you should think about disputes

Many Shopify store owners treat chargebacks as a fraud issue or a customer service issue. They are both. They are also a card-cost issue.

Repeated disputes can do more than drain revenue from individual orders. They can contribute to a risk profile that makes your payment environment more expensive over time. In other words, poor dispute control can turn a temporary loss into a longer-term drag on your baseline processing costs.

For Shopify merchants, this means chargeback management is also fee management. Winning more disputes and preventing weak ones from happening in the first place helps protect today’s revenue and helps prevent tomorrow’s card acceptance costs from getting harder to control.

Practical Strategies to Reduce Your Interchange Costs

You usually can’t negotiate interchange directly with Visa or Mastercard. For most Shopify merchants, that part is fixed by the network rules and by how the transaction qualifies. What you can do is improve how your transactions are processed and reduce the risk signals attached to your store.

That matters because interchange typically makes up 70% to 90% of total credit card processing costs, and in some cases, submitting enhanced transaction data known as Level 2 and Level 3 data can qualify certain transactions for up to 1% lower interchange rates, according to the overview of interchange fee structure and data qualification.

Start with transaction quality

Not every tactic fits every Shopify store, but these basics usually help:

Use AVS and CVV checks

These tools don’t eliminate fraud, but they help verify the billing address and card details before approval.Settle transactions promptly

Delays can hurt how some transactions qualify and can add avoidable mess to reconciliation.Keep order data clean

Clear product descriptions, accurate tax handling, shipping confirmation, and customer communication all help create a better transaction record.Use enhanced data where available

This is more common in B2B or certain specialized payment setups, but it matters enough to be worth asking your processor about.

Look at payment mix, not just payment rate

Sometimes the smartest cost move isn’t squeezing one card rate. It’s reducing how much of your volume flows through the most expensive pathways.

You can do that by reviewing payment options, wallet usage, and customer preferences. If you’re exploring checkout alternatives, this guide to alternative forms of payment is a useful way to think through whether different methods could reduce cost or risk for your store.

Protect your merchant risk profile

This is the strategy many merchants overlook.

Your transaction costs don’t live in a vacuum. If your business starts generating more disputes, processors may view your store differently. Once risk classification gets worse, your payment economics can get worse too.

Here’s what that means in practice:

Chargebacks signal operational risk

Networks and processors don’t see your internal context. They see a dispute count and a pattern.Riskier stores can face tougher treatment

That can show up in reserve requirements, monitoring, account pressure, or more expensive transaction categories.Future sales become less profitable

Even clean future orders can cost more because your store now carries a worse risk reputation.

Merchants often chase lower rates while ignoring the behavior that causes rates to rise in the first place.

Operational habits that help

A few store-level habits can reduce the odds that valid sales turn into unnecessary disputes:

Make descriptor clarity a priority

If a customer doesn’t recognize the charge, friendly fraud becomes more likely.Send fulfillment and delivery updates early

Silence after checkout creates anxiety, and anxious buyers dispute faster.Match ad claims to actual product experience

Misaligned expectations often become “item not as described” disputes.Respond to customer issues before they escalate

A refund may hurt less than a chargeback plus the downstream risk signal.

Think long term, not just per order

Most fee advice focuses on shaving small amounts off individual transactions. That can help. But for many Shopify merchants, the bigger win is avoiding the kind of chargeback pattern that pushes the whole business into a riskier category.

That’s why interchange cost control and dispute management belong in the same conversation. If you keep your dispute rate healthier, you’re not only protecting revenue from current orders. You’re protecting the cost structure attached to future ones.

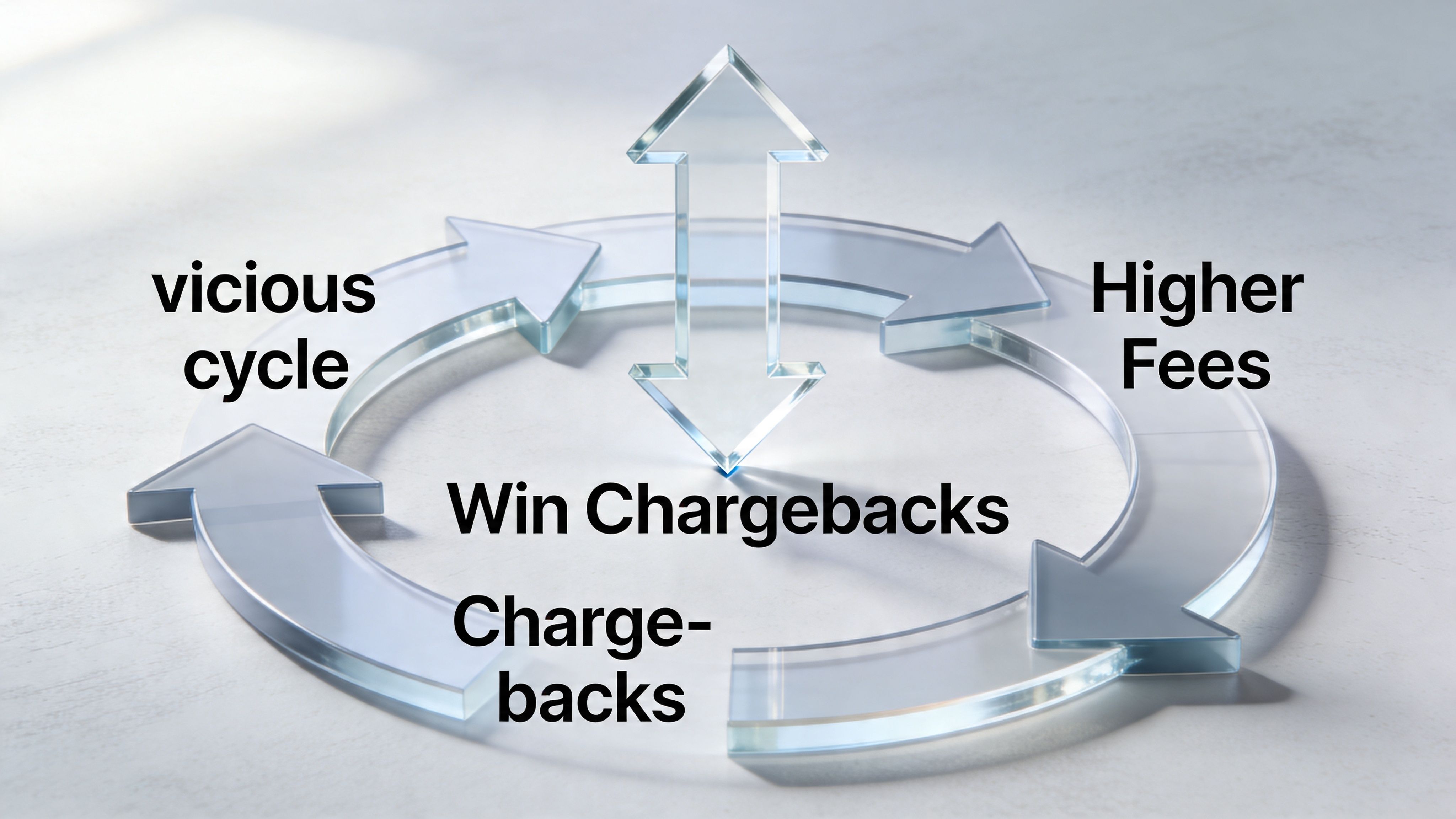

Why Winning Chargebacks Is Your Best Defense Against High Fees

A few chargebacks can start a nasty loop.

You lose revenue on disputed orders. Your processor sees more risk. Your store may face stricter scrutiny. Future transactions can become more expensive or more fragile. Then your thinner margins leave you with less room to absorb fraud, refunds, and customer support pressure.

The cycle most merchants notice too late

It usually looks like this:

- Disputes increase

- Payment risk perception gets worse

- Margins tighten

- The business has less room to absorb future losses

- More disputes hurt even more

This is why winning legitimate chargeback fights matters. You’re not just trying to recover one order. You’re defending the reputation of your merchant account.

Why the environment may get harder

There’s another reason this matters. The analysis of the 2024 Visa-Mastercard settlement notes that while average interchange should decline slightly, reduced issuer budgets for fraud handling could create pressure on how disputes are managed. In card-not-present commerce, that can mean issuers may approve more chargebacks by default, which increases the need for strong merchant-side defense, as discussed in this review of falling interchange fees and fraud-management pressure.

That matters a lot for Shopify brands, because online stores already live in a riskier environment than in-person retail.

If issuer-side fraud review gets weaker, merchants need stronger evidence and faster responses on their side.

Where automated representment fits

Manual dispute fighting is slow, inconsistent, and easy to miss when your team is busy running the store. That’s why many merchants use specialized tools to manage representment, evidence gathering, and submission deadlines.

If you want to understand the process itself before choosing a tool, this guide to chargeback representment gives a solid overview of how merchants challenge disputes and what evidence tends to matter.

The key point is simple. Winning chargebacks protects more than the disputed amount. It helps protect the payment profile that influences what your future sales cost to process.

Take Control of Your Card Processing Costs Today

Interchange is one of those costs that feels fixed until you understand what drives it. You may not control the card networks, but you do control a lot of the signals attached to your business. Better transaction quality, cleaner customer communication, and tighter dispute handling all help you protect margin.

For Shopify merchants, a key lesson is this: chargeback management is also fee management. If too many disputes pile up, the damage doesn’t stop with those orders. It can spill into how your store is viewed by payment partners and what future card sales cost you.

That’s why payment setup choices matter too. If you’re reviewing checkout infrastructure or planning a store upgrade, a practical resource on how to integrate a payment gateway can help you think through the bigger payments picture beyond just the default setup.

You don’t need to memorize every network rule. You do need to stop treating hidden card fees and chargebacks as separate issues. They hit the same margin, and they often feed each other.

The stores that stay healthier usually do one thing well. They catch payment risk early and respond before it becomes a baseline cost problem.

ChargePay helps Shopify merchants do exactly that. It automatically fights disputes, with a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered for merchants. It has a 4.9-star rating on the Shopify App Store, carries the Built for Shopify badge, and uses a pay-per-win model, so you only pay when money is recovered. If chargebacks are eating your margins and pushing up payment risk, install ChargePay from the Shopify App Store and turn dispute management into a solved problem.

.svg)

.svg)

.svg)

.svg)