When you're deciding between Klarna and Affirm for your Shopify store, you're not just adding a payment button. You're making a choice that directly impacts your revenue, your customer experience, and, most importantly, your vulnerability to chargebacks.

Here’s the direct comparison: Klarna is built for high-volume, smaller purchases. Think fashion, cosmetics, and everyday items. Its "Pay in 4" model is a huge driver for converting younger shoppers on frequent, lower-cost buys. On the other hand, Affirm is designed for big-ticket items—furniture, electronics, high-end equipment. It provides clear, upfront financing for customers making larger, planned purchases.

Klarna vs. Affirm: Key Factors for Shopify Merchants

Choosing a Buy Now, Pay Later (BNPL) provider isn't a small tweak; it's a critical business decision. Both Klarna and Affirm can boost your sales—we’ve seen stores get a 14% revenue bump in sessions where BNPL is offered—but they also bring unique risks. This choice directly impacts your cash flow, your customer's experience, and your exposure to costly disputes.

We're ChargePay, and we focus on one thing: protecting your revenue from chargebacks. We've been in the trenches with Shopify merchants, handling over 100,000 disputes and recovering more than $2.8 million. With a 92.4% win rate, we know exactly where the risks are. This guide cuts through the marketing fluff to give you the real-world data you need to choose between Klarna and Affirm.

Key Differences at a Glance

The biggest difference is their core payment models and target customers. Klarna's game is flexible, short-term options perfect for high-volume retail. Affirm acts more like a traditional loan provider, offering fixed-term financing for larger, considered purchases.

Understanding this difference is the first step to figuring out which one fits your business and your tolerance for risk.

The reality is, no matter which BNPL you choose, you're opening a new door for disputes. While these services aim to boost sales, our data shows they can also increase instances of friendly fraud.

Both services are powerful tools to increase your ecommerce conversion rate and grow your business. But you have to pair them with a solid chargeback management plan. Let’s dive into the details so you can pick the right partner and protect the new revenue you’re about to generate.

Understanding Their Core Business Models

To really get the Klarna vs. Affirm debate, you have to look at how each company makes its money. Their business models are fundamentally different, and that difference affects everything—the fees you pay, the options your customers see, and the types of risk your store will face.

Klarna operates on a volume game. Its primary income comes from merchant fees on every transaction. This means its goal is to get as many people as possible to check out, which is why its "Pay in 4" option is so dominant for smaller, everyday buys.

Affirm, however, acts more like a traditional lender. A significant portion of its revenue comes from the interest it charges shoppers on longer-term payment plans. This model is built for bigger-ticket items where customers need to spread the cost over several months or even years.

The Financials Tell the Story

The numbers show just how far apart these two strategies are. Both are massive players, but their revenue generation is night and day. Over the last four reported quarters, Klarna brought in $2.60 billion in revenue, while Affirm was right behind with $2.53 billion.

But the real story is in the margins. Affirm’s revenue is about 8.7% of its Gross Merchandise Volume (GMV)—the total value of all transactions it finances. Klarna's revenue, in stark contrast, is just 2.4% of its GMV. This tells you what you need to know: Affirm depends heavily on consumer interest, while Klarna’s business is fueled by merchant fees.

To see how these strategies affect your costs, let's break it down.

Klarna vs. Affirm Business Model At A Glance

As you can see, the way each company is structured creates a completely different set of incentives and risks for you as a Shopify merchant.

This is a crucial distinction. Klarna's model encourages high transaction frequency, which is great for sales but can also lead to a higher number of small-value disputes. Affirm's model, focused on bigger loans, carries the risk of a single, high-value chargeback that could wipe out your profit on dozens of sales.

What This Means for Your Bottom Line

So, why should you care about this? Because their business models directly influence the type of customer each platform brings to your store and the risks that come with them.

- Klarna's Focus: Klarna is perfect for catching impulse buyers. For you, the risk is often a wave of "friendly fraud" from many small transactions, which adds up to a big problem fast. We've seen merchants lose thousands this way.

- Affirm's Focus: Affirm appeals to shoppers planning a significant purchase. The danger here is that one large dispute could wipe out the profit from dozens of other sales. A single lost chargeback on a $2,000 item is a painful hit.

Understanding these alternative forms of payment is the first step toward building a checkout that works for you, not against you. Each model introduces different friction points that can turn into chargebacks. At ChargePay, we see merchants using both Klarna and Affirm successfully, but the ones who protect their revenue have a solid plan to manage the disputes that follow.

Comparing Merchant Fees and Payout Schedules

When you're deciding between Klarna and Affirm, the conversation always lands on two things: how much it costs you and when you get your money. This is where BNPL directly impacts your profit margins and cash flow. Both services take a cut, but their fee structures are designed for different kinds of businesses.

Both Klarna and Affirm charge a merchant fee that's part percentage, part fixed cost. A typical rate you might see is 5.99% + $0.30 per transaction. But don't take that as a fixed number. Your actual rates will depend on your sales volume, your industry, and the specific payment plans your customers use.

Since Klarna’s business model is built around merchant fees, their rates can sometimes be higher, especially for their popular "Pay in 4" plans. Affirm makes a good chunk of its revenue from consumer interest, which can allow them to offer more competitive merchant rates, particularly for long-term financing on big-ticket items.

Analyzing the Real Cost to Merchants

Let's run the numbers to see how these fees play out on your profit and loss statement. These examples show how small differences add up.

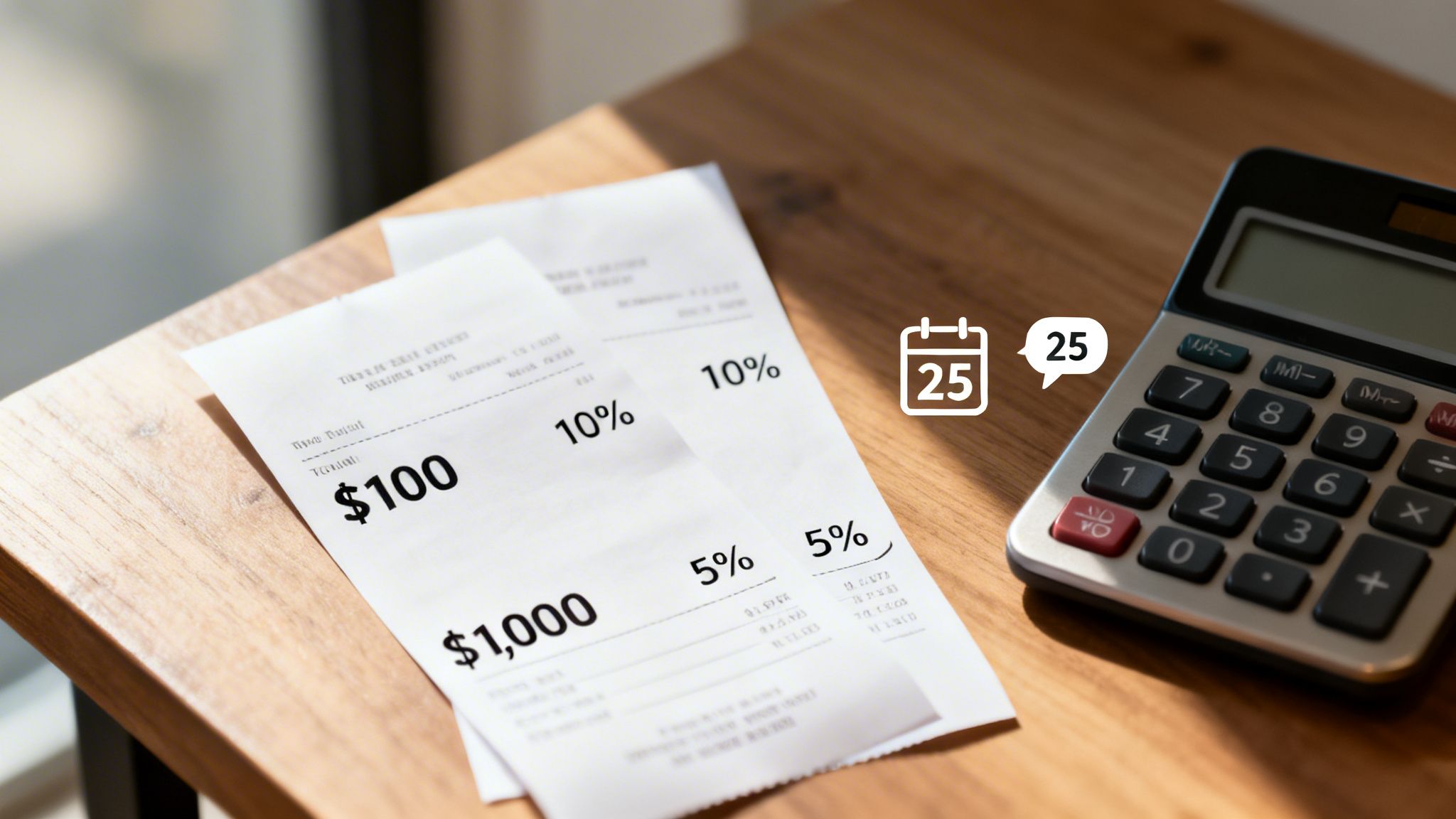

Example 1: A $100 Sale

- Klarna/Affirm (at 5.99% + $0.30): You'd pay $6.29 in fees, leaving you with $93.71. On smaller orders, the fees often look very similar.

Example 2: A $1,000 Sale

- Klarna/Affirm (at 5.99% + $0.30): You pay $60.20 in fees and keep $939.80.

While these examples use the same rate, this is where you have to get a custom quote. A high-volume furniture store might secure a better rate from Affirm for its long-term plans. A fast-fashion brand, however, might find Klarna’s overall package more valuable despite a similar fee. Getting a handle on your total Shopify payment processing fees is a critical part of this decision.

Getting Paid: Payout Schedules

Just as important as what you pay is when you get paid. The good news is that both Klarna and Affirm pay you the full purchase amount upfront (minus their fee). They take on the job of collecting the installments from the customer.

Payout speed is a big deal for growing Shopify stores. A delay of just a few days can strain your ability to restock inventory and fund marketing, putting a brake on your growth.

Typically, you can expect funds from both providers to settle within 1 to 3 business days after a transaction. Affirm often sends payouts via ACH transfer, which will land in your bank account according to standard banking timelines. Klarna works on a similar schedule. The exact timing can vary based on your specific agreement and sales volume.

Even with fast payouts, the threat of chargebacks is always there. A customer dispute can claw back that entire sale weeks or even months later. This is exactly why an automated chargeback system isn't just nice to have; it's necessary. At ChargePay, we’ve recovered over $2.8 million for merchants by fighting and winning these disputes on autopilot.

Who Is Responsible for Chargebacks and Fraud

When you add a BNPL button to your checkout, you're stepping into a different world of dispute resolution. This brings up the most critical question for any Shopify merchant weighing Klarna vs. Affirm: When a customer files a dispute, who actually foots the bill?

Both Klarna and Affirm have "seller protection" policies, but let’s be direct: they are not a free pass. Yes, they pay you upfront for the sale. But if a customer disputes the charge and wins, that money is coming right back out of your account.

The biggest headache here is "friendly fraud." This is when a customer gets your product but then disputes the transaction, claiming they never authorized it or the package never arrived. This is where the fine print in your BNPL agreement really matters.

Klarna's Seller Protection Policy

Klarna’s policy is built to shield you from certain types of fraud, mainly unauthorized purchases. If a customer claims they never made the purchase, and you’ve followed all of Klarna’s rules (like shipping to the verified address), Klarna will typically absorb that loss.

However, that protection has firm boundaries.

- You're Covered For: Unauthorized transactions, but only if you've perfectly met all of their shipping and fulfillment requirements.

- You're Liable For: Any disputes related to product quality, "item not as described," or "item not received" (INR) if your proof of delivery isn't rock-solid. For INR claims, you must provide valid tracking information showing the item was successfully delivered to the customer’s address.

If the customer’s complaint is about your product or your fulfillment, the responsibility lands squarely on you. You will be held liable for the full amount of the chargeback.

Affirm's Dispute Process

Affirm works in a similar way. They take on liability for fraud-related chargebacks, but any disputes about the merchandise itself fall to you. They will manage the dispute process, but your full cooperation is mandatory. You’ll need to supply compelling evidence, like proof of delivery or your email conversations with the customer.

If a customer initiates a dispute, Affirm acts as a mediator. They collect evidence from both you and the customer to make a decision. If you can’t provide strong evidence, you will lose the dispute and the revenue.

Let's walk through a common scenario.

Scenario: An 'Item Not Received' Dispute for a $500 Product

- With Klarna: The customer files a dispute. Klarna immediately asks you for proof of shipment and delivery. If your tracking number shows it was delivered to the right address, you'll likely win. If that tracking is missing, unclear, or shows it went to the wrong place, you lose the $500.

- With Affirm: The process is nearly identical. Affirm will request your documentation. Any failure to provide clear proof of delivery means you'll lose the dispute and the $500.

In both cases, the burden of proof is on you. Their seller protection is not a safety net for fulfillment mistakes or customer service issues. This is why having a dedicated system for managing these disputes is so important. You can find out more by exploring comprehensive guides on chargeback protection for merchants.

No matter which BNPL provider you choose, their policies have gaps that expose your revenue to risk. That’s where ChargePay comes in. We’ve handled over 100,000 disputes and know exactly what evidence is needed to win. Our AI automates the entire evidence-gathering and submission process, using data from winning cases to build the strongest possible response. This is how we’ve recovered over $2.8 million and maintain a 92.4% win rate. Install ChargePay from the Shopify App Store—it’s the essential protection for merchants navigating the world of BNPL.

How Each Integrates with Your Shopify Checkout

Your checkout is where you make money—or lose it. A clunky, confusing experience is one of the fastest ways to lose a sale. So, when you’re weighing Klarna against Affirm, you need to know how smoothly they’ll fit into your Shopify store and what your customers will see.

Both Klarna and Affirm plug directly into Shopify Payments, which makes activation in your admin panel simple. The real test, though, is how they perform from the customer’s point of view.

The Customer Checkout Flow

The goal is to get your customer from cart to confirmation with as little friction as possible. Both services display their payment options on your product and checkout pages, but the approval process is where they diverge.

Klarna's On-Site Approach: Klarna works to keep the customer on your site. For its "Pay in 4" plan, approval is often handled through a simple pop-up. The customer enters a few details, gets a quick decision, and never leaves your branded checkout.

Affirm's Redirect Model: Affirm sometimes sends the customer to its own site to finish the application. This is more common for longer-term financing plans that require a more detailed loan application. While thorough, that redirect takes the shopper away from your store, which can increase cart abandonment.

Thinking about how Klarna and Affirm slot into your store is just as important as any other critical Shopify integration.

A Look at App Store Ratings

Marketing materials tell one story, but merchant feedback tells another. Both Klarna and Affirm have official apps on the Shopify App Store, and the ratings are a goldmine of information on setup, reliability, and support.

This screenshot shows both have a massive footprint. The sheer volume of reviews proves they are major players in the Shopify ecosystem.

But digging into those reviews is where you find the truth. You’ll see common complaints about integration hiccups, customer service headaches, and settlement delays. If you want to learn more about how different payment options can impact your store, check out our guide on Shopify payment processors.

A smooth checkout flow directly leads to higher conversion rates. A difference of just one or two clicks, or being redirected off-site, can be the deciding factor for a customer.

Ultimately, a confusing checkout doesn't just lose you a sale—it creates a bad customer experience that can turn into a dispute down the road. A customer might get confused by the billing or just decide to commit friendly fraud out of frustration.

This is exactly why ChargePay is a critical tool for your store. We've handled over 100,000 disputes and recovered $2.8 million for Shopify merchants just like you. Our AI-powered system works in the background, automatically fighting and winning disputes with a 92.4% success rate, no matter if the order came through Klarna, Affirm, or another payment method. Install ChargePay from the Shopify App Store and stop losing money to checkout-related chargebacks.

Which BNPL Provider Is Right for Your Store

Alright, you have the breakdown of fees, dispute rules, and checkout flows. Now for the big question in the Klarna vs. Affirm matchup: which one makes sense for your store? The right answer comes down to what you sell, who you sell to, and what kind of risk you're comfortable with.

Think of it as a balancing act. Choosing a BNPL provider isn't just about adding a payment button; it's about how that choice fits into your overall business strategy.

When to Choose Klarna

Klarna is your go-to if your store has a lower average order value (AOV) and you're targeting a younger, mobile-first crowd. It shines in fast-moving verticals like fashion, cosmetics, and accessories.

Klarna’s "Pay in 4" model is perfect for encouraging impulse buys and getting customers over the finish line.

- Your AOV is under $250: Klarna's sweet spot is making smaller purchases feel more manageable with interest-free installments.

- You sell high-volume, low-margin goods: The platform is built for frequency. If your goal is to lift overall sales volume, Klarna is a powerful engine.

- Your target demographic is Gen Z or Millennial: Klarna's branding and app experience are designed specifically for how these generations shop.

Just be ready for a potential increase in smaller disputes. With high transaction volumes, you will see more cases of friendly fraud. Those small losses add up fast if you're not managing them.

When to Choose Affirm

Affirm is the stronger choice if you're selling higher-ticket items where customers need predictable, longer-term financing to click "buy." Think furniture, home fitness gear, or high-end electronics. Spreading a large purchase over several months is a huge conversion driver in these categories.

- Your AOV is over $500: Affirm's transparent loan terms make big-ticket items less intimidating. Shoppers know the exact monthly payment upfront.

- You want to offer crystal-clear financing: Affirm operates more like a traditional lender, giving customers total clarity on interest and the final cost.

- Your customers are planning major purchases: This audience isn't looking for a quick split-pay option. They value the predictability of a fixed monthly payment plan.

The risk with Affirm is different, but just as real. You might see fewer disputes, but losing a single chargeback on a $2,000 sofa is a much bigger hit than losing a few on $50 t-shirts. Affirm's financial health is also a factor. In its latest quarter, Affirm posted a 34% revenue increase and a 28% adjusted operating margin, which stands in contrast to Klarna's negative operating margin. This stability suggests Affirm is a solid platform for the long haul.

Ultimately, your choice isn’t just about boosting sales. It’s about protecting the new revenue you generate. Both Klarna and Affirm create new pathways for chargebacks.

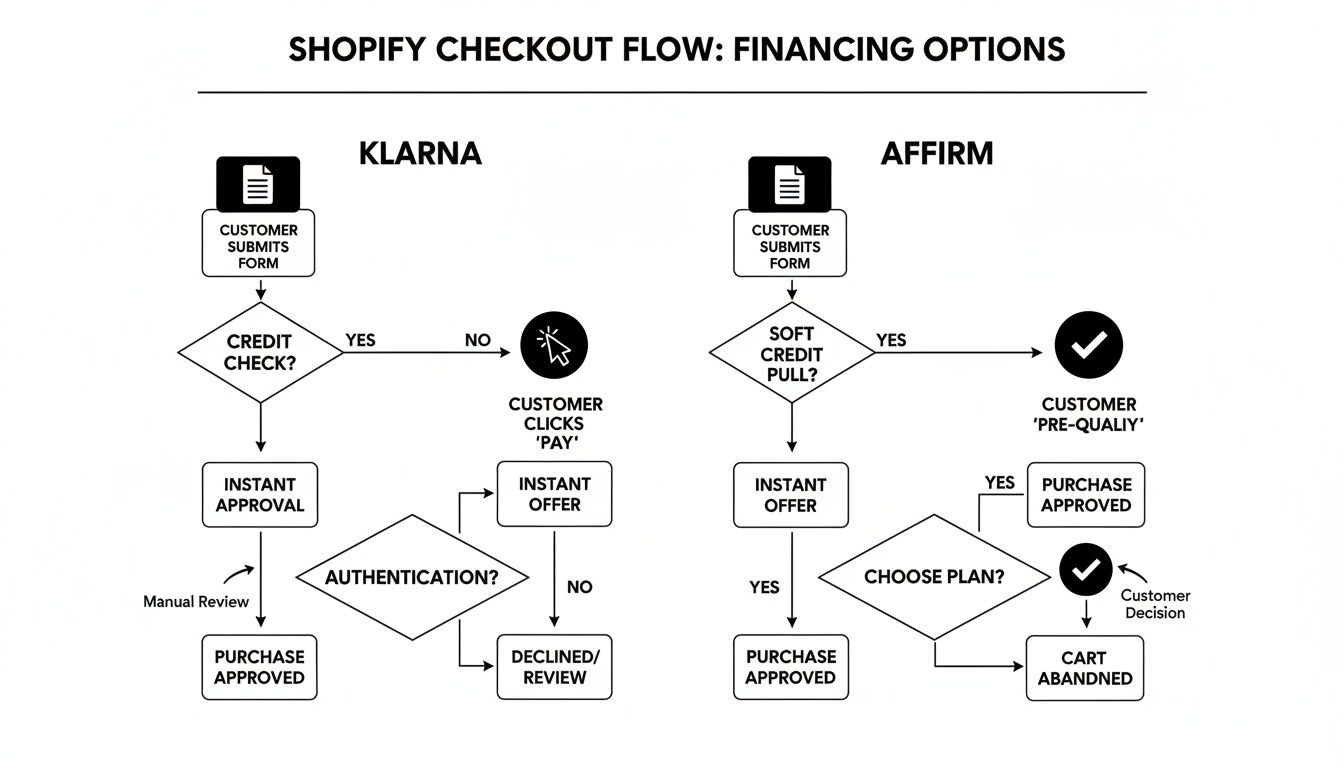

This decision tree gives you a visual of how each provider slots into the Shopify checkout experience.

As you can see, both start with a simple customer form. But Klarna pushes for quick, on-site approvals for its short-term plans, while Affirm’s process for larger loans can be more involved.

No matter which path you take, don't leave that new revenue exposed. With over 100,000 disputes handled and more than $2.8M recovered for merchants, ChargePay is the safety net every Shopify store needs. Our 92.4% win rate isn't just a number; it's proof our AI-powered system delivers. Install ChargePay from the Shopify App Store—it has a 4.9-star rating and a "Built for Shopify" badge for a reason.

Frequently Asked Questions

When you're weighing Klarna against Affirm, a few key questions always come up. Here are direct answers to what we hear most from Shopify merchants.

Is Klarna or Affirm Better for Small Purchases?

Nine times out of ten, Klarna is your go-to for smaller, everyday buys. Its "Pay in 4" option was built for those sub-$250 transactions. This setup is perfect for encouraging impulse buys and boosting conversions on lower-priced goods like fashion accessories or cosmetics.

While Affirm has a Pay in 4 feature, its real strength is financing bigger-ticket items with longer payment terms.

Which Has Higher Merchant Fees: Klarna or Affirm?

On the surface, merchant fees for both Klarna and Affirm look similar, often around 5.99% + $0.30 per transaction. But the rate you actually pay can change based on your sales volume, industry, and the contract you negotiate.

Because Klarna’s business model is almost entirely funded by merchant fees, they can be less flexible on rates. Affirm, on the other hand, also makes money from consumer interest on longer-term loans. This can give them more room to offer sharper rates, particularly for merchants selling high-ticket items.

The most important thing to remember is that both BNPL options introduce new chargeback risks. A single lost dispute can wipe out the profit from dozens of sales, making the fee a secondary concern.

Can a Customer Do a Chargeback on Klarna or Affirm?

Yes, absolutely. A customer can dispute a purchase made through Klarna or Affirm, and the process is very similar to a standard credit card chargeback. When this happens, both providers will ask you to submit compelling evidence, like proof of delivery, to defend the sale.

If you can’t provide enough evidence, you'll be on the hook for the full amount. This is a critical risk that every merchant using BNPL needs a plan to manage.

No matter which provider you choose, friendly fraud and customer disputes are an inevitable part of offering BNPL. Don't let that revenue slip away. ChargePay uses AI trained on over 100,000 disputes to automatically fight and win chargebacks for you, recovering your money with a 92.4% success rate. Install ChargePay from the Shopify App Store and protect your profits.

.svg)

.svg)

.svg)

.svg)