If you run subscriptions on Shopify, recurring charges aren't just a billing setting. They're a chargeback trigger.

Consumers underestimate subscription spend badly. One survey says the average American spends $219 per month on subscriptions but thinks it's only $86, which creates a $133 monthly gap and leaves a lot of room for “I don't recognize this” disputes, especially when the charge hits weeks later on a bank statement. That same research says 89% of consumers underestimate their subscription spending (subscription spending research).

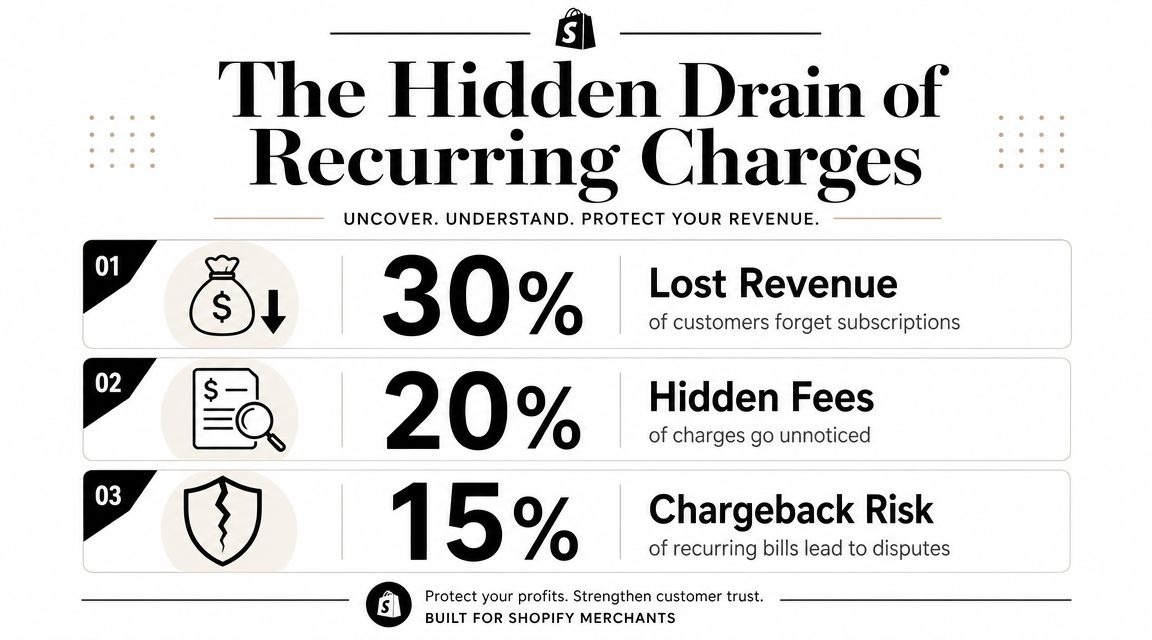

You feel that gap as lost revenue, refund pressure, and chargebacks that eat your time long after the sale looked settled.

The Hidden Drain of Recurring Charges

A recurring charge looks harmless when you set it up. Automatic rebills. Predictable revenue. Less checkout friction.

Then the cardholder forgets. The statement arrives. Your descriptor looks vague. Support doesn't answer fast enough. The customer files a dispute instead of asking for help.

Why this hits Shopify merchants harder

Subscription merchants live on repeat billing, but repeat billing also creates repeat chances for confusion. The same automatic charge that protects retention can also produce an “unrecognized transaction” claim when a customer forgets they signed up, misses a renewal reminder, or doesn't connect your store name to the statement line.

That matters because recurring disputes are expensive even before you lose them. You lose the sale, you risk fees, and you lose staff time chasing evidence. If you need a refresher on that extra cost, review what a chargeback fee actually does to each dispute.

Practical rule: If a customer has to think for more than a second about who charged them, you're already closer to a dispute.

The real problem isn't billing. It's memory plus friction.

People don't monitor subscriptions carefully. They autopay them, forget them, and revisit them only when something feels off. That's why recurring billing creates a quiet leak in merchant revenue. The customer doesn't always feel dishonest. They often feel surprised.

Here's the blunt version. If your subscription flow depends on the customer remembering old consent without clear reminders, clear descriptors, and easy cancellation, you're funding future chargebacks.

Decoding Recurring Charges and Billing Descriptors

So, what are recurring charges?

They're pre-authorized payments a merchant runs on a fixed schedule, such as monthly, quarterly, or annually, until the customer cancels. Common examples include streaming plans, memberships, utilities, and phone bills (recurring charge definition from Capital One).

But merchants need to think about them in a more operational way. A recurring charge isn't just a repeated payment. It's a pre-authorized agreement that creates a stateful subscription transaction, meaning your system has to track authorization, billing schedule, cancellation status, and related records across the full customer lifecycle (stateful subscription transaction explanation).

What the customer actually sees

Customers usually don't remember your checkout page. They remember their bank statement.

If the descriptor says something generic, they won't connect it to your store. That's where trouble starts. A descriptor like “SP*YOURSTORE” gives you a fighting chance. A descriptor that looks like a processor label or legal entity nobody recognizes creates confusion fast.

Here's a simple comparison:

| Descriptor type | What the customer thinks |

|---|---|

| Recognizable store name | “Yes, that's the brand I bought from.” |

| Processor name or vague company name | “I don't know what this is.” |

A lot of merchants obsess over checkout conversion and ignore statement clarity. That's backwards. The billing descriptor is one of the cheapest forms of chargeback prevention you'll ever get.

Your descriptor should answer one question fast

Can the customer identify the charge without opening a browser?

If the answer is no, fix it. Also make sure your support email, renewal email, and checkout confirmation all use the same brand name customers will later see on statements. Consistency matters.

If you're dealing with customers who say a valid payment is unauthorized, it helps to understand the difference between true fraud and confusion-driven disputes. This breakdown of what disputed charges mean is worth reading.

A recurring charge becomes dangerous when the customer remembers the product but doesn't recognize the statement.

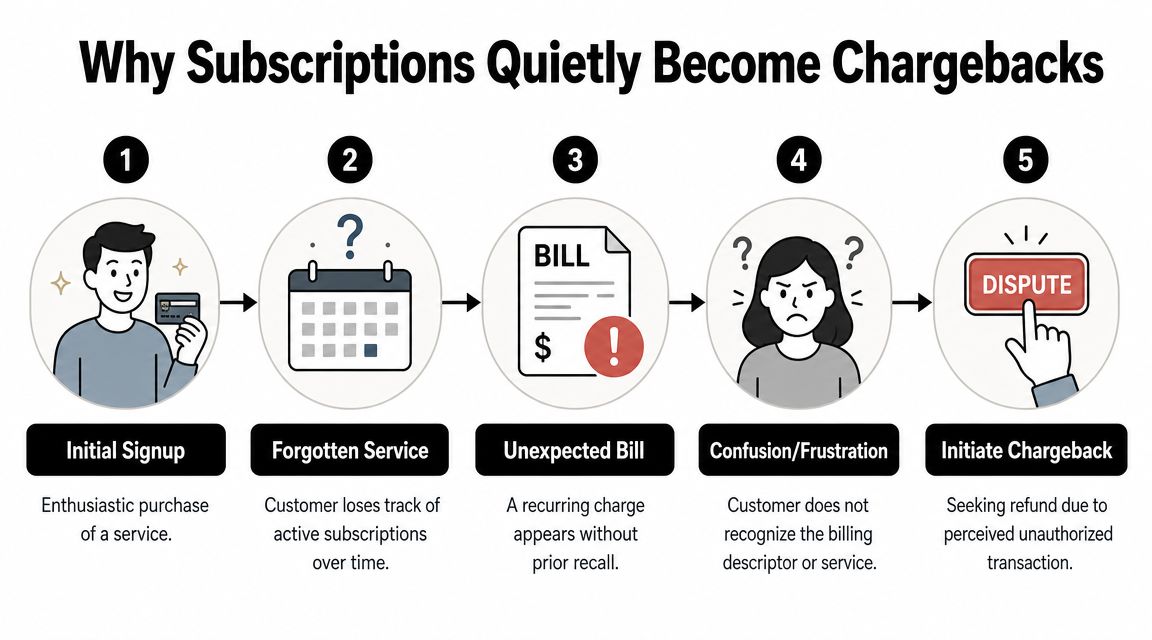

Why Subscriptions Quietly Become Chargebacks

Most recurring chargebacks don't begin with theft. They begin with fog.

A customer signs up for a free trial, a bundle, or a monthly product plan. They mean to evaluate it later. Then work gets busy, their card is on autopay, and the first rebill hits without any mental context. Research says 74% of consumers find it easy to forget recurring monthly subscription charges, and 72% have subscriptions set to auto-pay (recurring charge behavior data).

The path from signup to dispute

The customer journey usually looks like this:

- Signup felt easy: They clicked through an offer, a trial, or a subscribe-and-save option.

- Memory faded: They stopped using the product, or forgot the renewal date.

- The statement looked unfamiliar: The descriptor didn't match the brand they remembered.

- Support felt slower than the bank: Filing a dispute looked easier than waiting for an answer.

- The bank became customer service: Now you're defending a chargeback instead of solving a ticket.

That's why cancellation friction is so dangerous. When customers can't quickly confirm whether a subscription is active, paused, or canceled, they assume the worst. If you want to see how subscription cancellation expectations are framed in another subscription context, this example of canceling your app store research account is useful because it spells out what happens after cancellation in plain language.

Surprise charges are the spark

The most dispute-prone moments aren't the original signups. They're the moments when billing changes shape. A free trial turns into a paid plan. A price increases. A plan changes. A renewal happens sooner than the customer expected.

Stripe's explanation of recurring billing mechanics points to the underlying issue: many complaints come from surprise charges after a free trial, price increase, or plan change, and the core problem is opacity, not the existence of recurring billing itself (unexpected recurring charge analysis).

Customers don't dispute what they clearly understand. They dispute what feels like a surprise.

If your subscription terms are buried, your reminders are weak, or your cancellation path is annoying, you're creating the exact conditions that card networks and regulators care about. That's also why merchants should pay attention to the FTC negative option rule, especially if trials and auto-renewals are part of the offer.

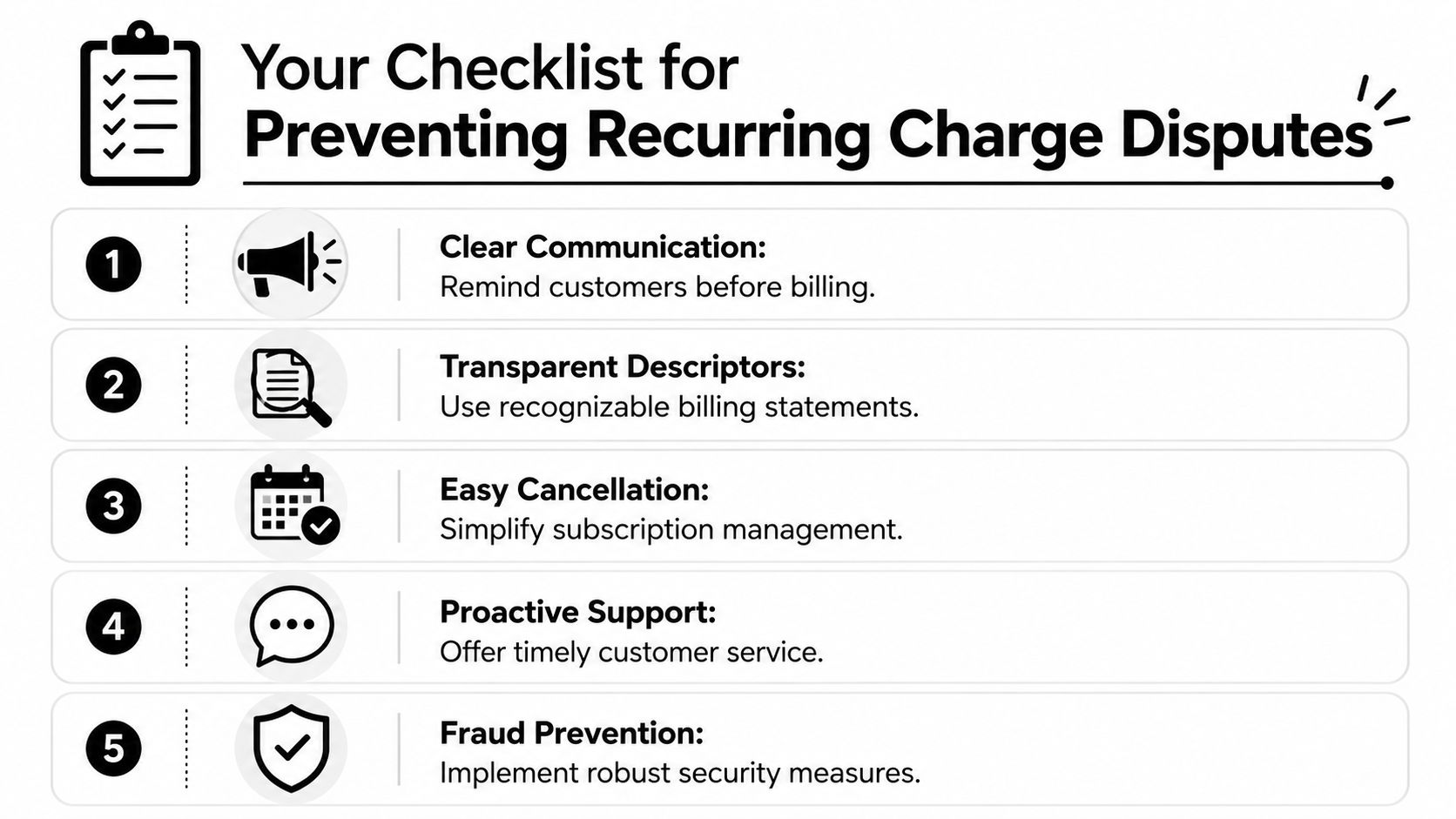

Your Checklist for Preventing Recurring Charge Disputes

Prevention beats representment. Every time.

If you wait until a customer files a chargeback, you're already on defense. A recurring billing system needs to do more than charge cards on schedule. It needs to remove ambiguity before the customer reaches for their bank app.

Fix the customer-facing weak points

Start with the places where confusion usually begins:

- Use a readable descriptor: Your statement name should match the brand the customer remembers, not your processor, warehouse entity, or parent company.

- Send renewal reminders: Especially before a trial converts, before an annual plan renews, or before a price change takes effect.

- State the terms in plain English: Billing interval, renewal timing, cancellation method, and what happens after cancellation should be obvious at checkout.

- Make cancellation easy: If support has to explain how to leave, you're inviting a dispute.

- Store proof of consent: Keep checkout records, timestamps, acceptance of terms, and confirmation emails.

Many recurring disputes aren't about the charge itself. They're about customers seeing a surprise charge after a free trial, price increase, or plan change and deciding it wasn't properly communicated (Stripe recurring billing guidance).

Build a paper trail before you need one

Merchants lose recurring disputes because they can prove a payment happened, but not that the ongoing billing relationship was clear.

Use this as your operating standard:

- Capture consent at signup. Make the recurring nature of the purchase visible before payment is submitted.

- Confirm the agreement immediately. Email the customer the plan details, amount, cadence, and cancellation steps.

- Remind before sensitive billing events. Trial ending. Plan change. Price update. Annual renewal.

- Log every account action. Login activity, plan changes, skipped shipments, cancellations, and support replies all matter later.

A quick explainer can help your team tighten the flow:

Use tools that reduce human delay

Manual processes break under subscription volume. If your team is piecing together screenshots from Shopify, your email platform, and your help desk every time a dispute arrives, the system is already failing.

Tools should help you centralize evidence, monitor disputes, and respond before deadlines. One example is ChargePay, which is built for Shopify and focuses on automating dispute evidence and submission for merchants dealing with recurring billing and friendly fraud. Use whatever stack fits your workflow, but stop relying on scattered records and memory.

How to Win When a Recurring Chargeback Happens

When a recurring dispute lands, don't argue the customer's motives first. Prove the relationship.

That's the core mistake merchants make. They submit a receipt and think that's enough. It isn't. Recurring billing is a major driver of card-not-present disputes, and many of these cases are consent disputes, not true stolen-card fraud. You need to prove the customer authorized an ongoing relationship, not just one transaction (recurring dispute and consent guidance).

The evidence package that actually matters

For a recurring chargeback, gather records that show continuity:

- Original order confirmation: The first purchase receipt with product or plan details.

- Subscription terms accepted at checkout: A screenshot or system record showing the customer agreed to recurring billing.

- Renewal or billing notices: Emails sent before rebills, price changes, or trial conversion.

- Cancellation policy visibility: Proof that cancellation terms were disclosed where the customer purchased.

- Usage evidence: Login history, shipment records, downloads, account access, or service activity.

- Cancellation timeline: Whether the customer canceled, when they canceled, and what happened after.

Match the evidence to the claim

Not every reason code needs the same response.

| Dispute theme | What to emphasize |

|---|---|

| Unrecognized transaction | Descriptor clarity, order confirmation, customer identity match |

| Canceled recurring transaction | Cancellation policy, cancellation date, billing timing |

| Fraud claim on valid subscription | Initial authorization, ongoing usage, renewal notices |

Response standard: Show who agreed, what they agreed to, when they were billed, and what happened after.

That same logic shows up in other high-friction e-commerce disputes too. If you sell across channels, this discussion of Amazon seller suspension challenges is a good reminder that online sellers often lose when documentation is fragmented.

Speed matters almost as much as evidence

A strong case submitted late still loses.

You need a repeatable workflow for intake, evidence collection, writing, submission, and deadline tracking. If your current process depends on one ops manager digging through tools while juggling support tickets, fix that now. A practical starting point is understanding how chargeback representment works and what your issuer or processor expects in a defensible response.

Automate Your Defense and Recover Lost Revenue

Recurring charges create a weird mix of convenience and risk. Customers like autopay until they forget a subscription, miss a plan change, or decide your support queue is slower than their banking app. Then your team gets buried in disputes that require records from checkout, email, subscription billing, and support.

That workload is exactly why merchants move to automation. You need a system that can pull evidence fast, spot consent disputes, and submit a coherent response before deadlines close. If you're comparing options, even broader directories like this Dispute AI assistant overview show how much the category is shifting toward automated dispute handling instead of manual firefighting.

For Shopify merchants, ChargePay fits that job directly. It handles the dispute lifecycle, builds evidence packages, and submits responses using store data instead of forcing your team to assemble every case by hand. It also carries a Built for Shopify badge, a 4.9-star Shopify App Store rating, and uses pay-per-win pricing, which is a sensible model when you're trying to recover revenue instead of adding another fixed software bill. If you want the broader playbook behind that approach, read this guide to automated chargeback and dispute management using AI.

If recurring chargebacks are draining your Shopify revenue, install ChargePay. It automates evidence collection, fights disputes for you, and only charges when money is recovered.

.svg)

.svg)

.svg)

.svg)