You check your Shopify payout, see a sale come through, and the deposit is lower than expected. Nothing looks broken. Nothing looks stolen. But the math still feels off.

That gap is usually a merchant fee. It's the cost of accepting card payments, and it shows up so often that many store owners stop questioning it. That's understandable. You're busy shipping orders, handling support, and trying to keep acquisition costs under control.

Still, this line item deserves attention. These fees look small on a single order, but they add up fast. U.S. merchants paid a record $187.2 billion in swipe fees in 2024, and the average Visa and Mastercard credit card swipe fee rate reached 2.35%, according to Swipesum's merchant fee overview.

If you run a Shopify store, understanding merchant fees helps you predict margins more accurately. It also helps you spot the more painful cost sitting nearby on the same statements and dashboards: chargeback fees. Processing fees are expected. Chargebacks are where many stores start losing money in chunks instead of slices.

That Confusing Line Item on Your Payout Report

A lot of Shopify owners learn about merchant fees backward. Not from a contract. Not from a finance meeting. From a payout that lands short.

You make a sale, celebrate for a second, and then notice the amount that settles is lower than the order total. That difference can feel random when you first see it, especially if your orders come from different channels, use different payment methods, or include a mix of domestic and online transactions.

Merchant fees are a normal part of card acceptance. They're not a bug in your payout report. They're one of the built-in costs of selling online. But “normal” doesn't mean “simple,” and it definitely doesn't mean “harmless.”

Why this matters to a Shopify store owner

If you don't understand what is a merchant fee, it's hard to answer basic business questions:

- What did I really make on this order

- Why do some sales cost more to process than others

- Why does my effective payment cost seem to drift over time

- Where should I focus first, fee reduction or dispute prevention

A good starting point is knowing that the headline processing rate is only part of the story. Your actual payment costs can include fixed transaction charges, provider markups, and dispute-related fees that hit later.

Practical rule: Don't treat payment fees as a single flat tax on revenue. Treat them as a cost stack that changes by order type, channel, and risk.

If you want a broader breakdown of how these deductions show up for Shopify stores, this guide to Shopify payment processing fees is a useful companion.

The big mindset shift is this: standard merchant fees are usually predictable enough to model. The more dangerous losses tend to come from the charges merchants overlook until they pile up, especially dispute and chargeback costs.

The Three Players Taking a Slice of Your Sale

A merchant fee isn't one company charging you one simple price. It's usually a split among multiple parties involved in moving card money from your customer to your store.

Imagine a pizza cut three ways. Each participant takes a slice for a different job.

The issuing bank

This is your customer's bank, the one that issued their card.

It approves or declines the transaction and takes on part of the payment risk. The largest portion of the merchant fee usually goes here in the form of interchange.

The card network

This is the brand layer, such as Visa or Mastercard.

The network routes transaction data between banks and sets rules for how card payments work. It takes a smaller fee for operating that system.

The acquirer or processor

This is the merchant-side payment provider, the company that helps your business accept card payments and receive funds.

On Shopify, this role may be handled through your payment setup and processor relationships in the background. If you want a cleaner view of who does what on each side of a card transaction, this explanation of acquirer vs issuer helps.

Why the fee exists at all

These fees fund the card payment system itself. In the U.S., card transaction volume grew from 37.6 billion transactions in 2009 to 92.1 billion in 2021, as noted in the Federal Reserve figures summarized in this interchange fee overview. More card usage means more merchant-fee exposure for businesses that rely on card payments.

Most confusion starts when merchants assume “my processor charges me a fee.” In practice, several players are getting paid through that one deduction.

That's why a merchant statement can feel harder to read than a Shopify sales report. You're not looking at one cost. You're looking at a bundle.

Anatomy of Your Total Merchant Fee

Once you know who gets paid, the next question is what you're paying for.

For a typical $100 online purchase in the U.S., the merchant might receive about $98, with about $1.75 going to interchange, $0.18 to the card network, and $0.07 to the processor, according to this interchange fee breakdown.

That example helps because it turns an abstract percentage into something tangible. You sold $100. You didn't keep all $100. The missing amount wasn't one mystery fee. It was several smaller charges grouped together.

The biggest piece is usually interchange

Interchange generally goes to the cardholder's bank. It's often the largest component in the total merchant fee.

That's one reason online merchants usually feel these costs more than they expect. Card-not-present transactions carry more fraud risk, and pricing often reflects that. If you sell on more than one platform, it also helps to compare how fee structures behave in different channels. For example, if you also sell socially, this guide can help you protect your TikTok Shop profits.

The smaller pieces still matter

Beyond interchange, your total cost often includes:

- Assessment fees charged by the card network

- Processor markup charged by your payment provider

- Monthly and incidental fees that may not show up in the headline rate

- Chargeback-related fees that appear only when something goes wrong

Stripe's fee explainer makes this point clearly in its discussion of interchange, assessments, processor markup, monthly statement charges, incidental fees, and chargeback fees in its merchant fee guide.

A merchant fee is easier to manage when you stop asking “what's my rate” and start asking “what line items make up my real cost.”

If you want the middle layer demystified, this explainer on what a payment processor does is worth reading.

A short video can also help if you prefer to see the moving parts laid out visually.

What merchants often miss on statements

The most common mistake is focusing only on the advertised transaction rate.

A cleaner way to read your costs is to separate them into two buckets:

| Cost bucket | What it usually includes |

|---|---|

| Expected processing costs | Interchange, network fees, processor markup |

| Operational and risk costs | Monthly fees, compliance charges, chargeback fees, other incidental fees |

That second bucket is where a lot of revenue leaks happen. It doesn't always show up every day, so it's easier to ignore until margins start feeling tighter than your sales numbers suggest they should.

How Your Merchant Fees Are Calculated

Most Shopify merchants encounter blended pricing. That means the processor charges a percentage of the sale plus a fixed fee per transaction. Industry examples commonly use pricing such as 2.6% + 10¢, as described in Shopify's merchant fee guide.

That fixed fee matters more than many people expect.

Why small orders feel more expensive

On a low-ticket order, the fixed charge takes up a bigger share of the sale. On a larger order, the percentage part does more of the work.

Here's a simple model using the sample rate requested below.

| Metric | Small Order Example | Large Order Example |

|---|---|---|

| Order value | $15.00 | $250.00 |

| Percentage fee at 2.9% | $0.435 | $7.25 |

| Fixed fee | $0.30 | $0.30 |

| Total fee | $0.735 | $7.55 |

| Net before other business costs | $14.265 | $242.45 |

What the table is telling you

The small order pays less in total dollars, but the fixed fee takes a bigger bite relative to the order size.

That's why stores with lots of low-priced items often feel more pressure from processing costs than stores with higher average order values. If your catalog includes low-ticket add-ons, samples, or impulse buys, that fixed component can gradually diminish your margin.

For small baskets, the flat transaction charge is often the part that hurts most.

A better question than what is my rate

Instead of asking only for your listed rate, calculate your effective rate across real orders.

Look at patterns like:

- Small-ticket orders where fixed fees hit harder

- Higher-value orders where the percentage portion dominates

- Online or keyed-in sales that may cost more because of risk

- Refunded or disputed orders where your net economics change again

You don't need complicated finance software to start. Export a period of orders, compare gross sales against net deposits, and group by average order value. That alone usually reveals where merchant fees are most painful.

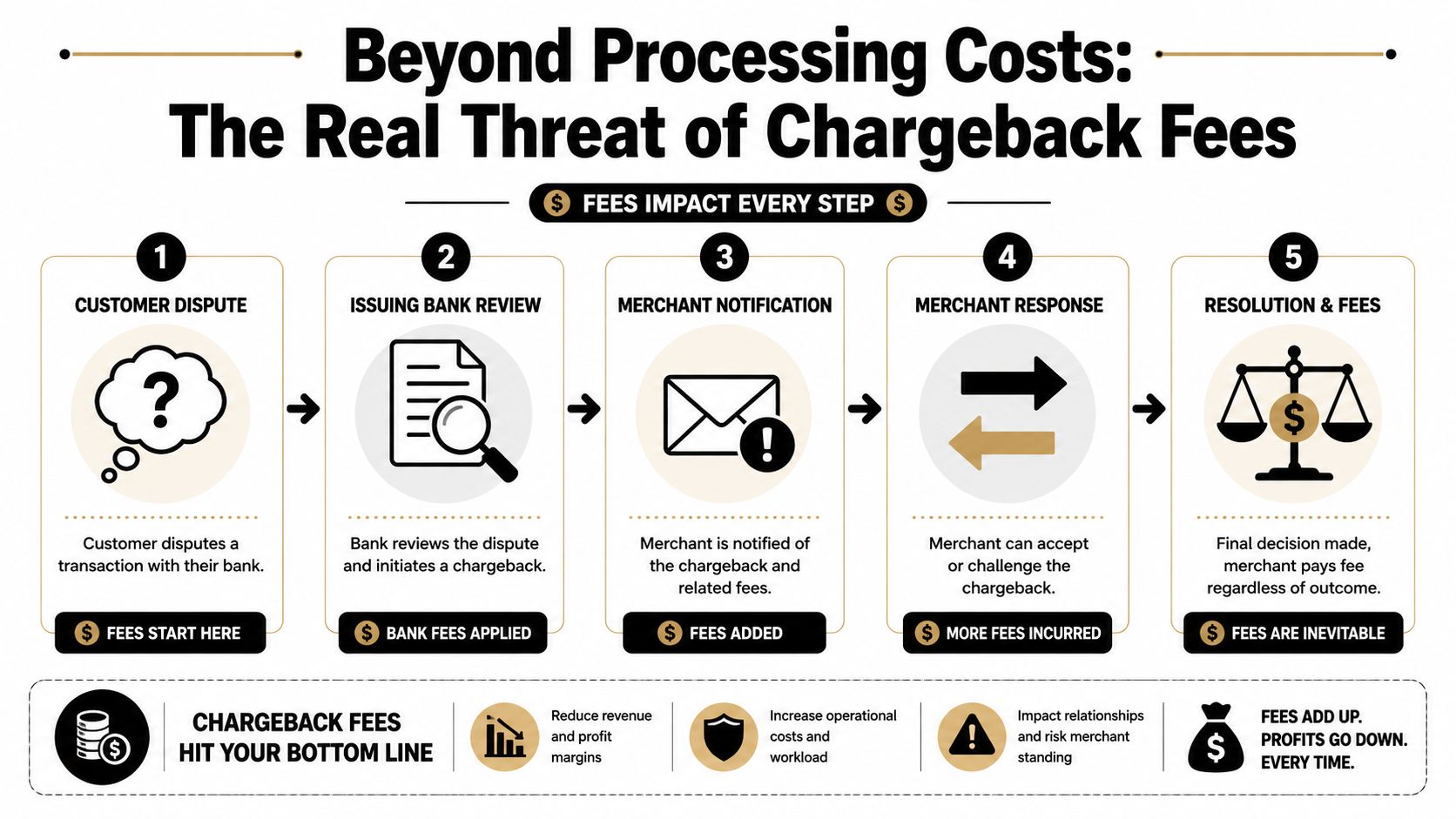

Beyond Processing Costs The Real Threat of Chargeback Fees

Standard processing fees are frustrating, but they're at least predictable. You can model them into your margin. You can price around them. You can review them each month.

Chargebacks are different.

A chargeback can remove the sale, create extra admin work, and trigger a separate fee on top of the revenue loss. Stripe also notes that merchant fees can include incidental charges such as chargeback fees, which is why the true cost is spread across more line items than many merchants expect in its merchant fee resource.

Why chargebacks hit harder than merchant fees

A normal merchant fee takes a slice of a sale.

A chargeback can threaten the whole sale.

That's the difference. If you spend all your time trying to shave a little off processing costs while disputes keep draining full order value, you're solving the smaller problem first.

Here's the practical contrast:

- Merchant fees are expected and usually apply to every successful card payment

- Chargeback fees arrive after a dispute and create extra loss around an order that already looked complete

- Friendly fraud makes this worse because the order may have been fulfilled correctly, yet you still have to defend it

If you need a clearer definition of the dispute-side penalty itself, this guide on what a chargeback fee is breaks it down in plain language.

The hidden operational cost

Even when a chargeback starts small, it creates work across your team.

Someone has to pull order records. Someone has to find tracking. Someone has to check customer communication. Someone has to submit evidence before the deadline. For busy Shopify brands, that process usually lands on an ops manager, founder, or support lead who already has too much on their plate.

The real cost of a chargeback isn't just the fee. It's the lost sale, the time spent responding, and the margin pressure that follows.

That's why merchant fees and chargeback fees should be viewed together. One is the routine cost of accepting payments. The other is the penalty layer that appears when a transaction breaks down or gets challenged after the fact.

Your Action Plan to Protect Your Profits

Start with the part you can control every week.

Review your statements and payout reports. Separate routine processing costs from dispute-related costs. If your margins feel tighter than they should, don't just ask whether your rate is too high. Ask which order types, channels, or dispute patterns are creating the drain.

What to do first

A practical plan usually looks like this:

- Audit your real payment cost by comparing gross sales, net payouts, and any recurring account or dispute charges

- Watch order mix because low-ticket orders and online transactions can change your effective fee picture

- Tighten fraud and post-purchase communication so fewer legitimate orders turn into disputes

- Create a dispute workflow before chargebacks start piling up

If you need broader technical or operational support for Shopify businesses, it helps to work with partners who understand checkout, fulfillment, and store systems together rather than in isolation.

Where automation fits

For dispute management, manual work breaks down fast. Evidence gathering is repetitive, deadlines are rigid, and merchants often respond too late or with incomplete documentation.

One option is ChargePay, an AI-powered chargeback management app for Shopify merchants. According to ChargePay, it has a 92.4% win rate, has handled 200K+ cases, and has recovered $10.8M+ for merchants on a pay-per-win model. It also carries a 4.9-star rating on the Shopify App Store and a Built for Shopify badge. If prevention is your priority before disputes happen, this guide to chargeback prevention is the right next read.

The key takeaway is simple. Merchant fees are part of doing business online. Chargebacks are the part that can distort your margins fast if you leave them unmanaged.

If chargebacks are eating into your Shopify revenue, ChargePay gives you a way to automate the dispute process instead of handling it order by order. It fights chargebacks, submits evidence, and helps recover lost revenue without adding manual work to your team. Install ChargePay from the Shopify App Store if you want a clearer way to protect profit after the sale.

.svg)

.svg)

.svg)

.svg)