You approve the order. Shopify shows the CVV matched result. The package goes out on time.

Then the dispute lands anyway.

For a lot of store owners, that's the moment the card verification code mastercard check stops feeling like a security feature and starts feeling like a false promise. You did ask for the code. The bank did accept it. But the funds still got pulled back, the inventory is gone, and you're left proving a transaction you thought was already verified.

That disconnect matters because many merchants treat CVV or CVC as stronger evidence than it really is. It helps at checkout. It does not carry much weight once a cardholder says the charge was unauthorized. If you're trying to reduce fraud and protect revenue, that distinction is the difference between a useful filter and a weak dispute defense.

The Frustrating Truth About CVV Security Checks

A common Shopify pattern looks like this. A customer enters a Mastercard number, expiration date, and the three-digit code from the back of the card. The transaction clears. Nothing looks obviously wrong, so the order gets fulfilled.

Weeks later, the issuer reverses the payment.

What merchants expect

Most merchants read a CVC or CVV match as confirmation that the buyer was legitimate. That assumption sounds reasonable. If the buyer knew the code, they must have had the card. If they had the card, the purchase should be defensible.

That logic breaks down fast in chargebacks.

A passed card security code check is a checkout signal, not a liability shield.

What actually happens in disputes

In card-not-present commerce, banks and card networks know that stolen card details can include the security code. They also know that some disputes come from the actual cardholder after delivery. So when a merchant submits a response built around "the CVV matched," the issuer usually wants more.

What matters more is evidence tied to customer behavior and order fulfillment, such as:

- Address consistency: Billing and shipping details that align with the order story

- Customer activity: Login history, account age, prior purchases, and communication records

- Fulfillment proof: Carrier scans, delivery confirmation, and any delivery-related notes

- Authentication records: Additional verification steps beyond the code itself

If you're losing chargebacks on orders that passed CVC, the problem usually isn't that your checkout skipped a basic control. It's that your evidence package stops at the wrong layer.

What Is a Mastercard Card Verification Code

A Mastercard card verification code is the three-digit security code on the back of the card. Mastercard refers to it as CVC2, and processors use it during card-not-present transactions to check whether the buyer entered a code associated with the account, as described in this card security code reference.

Where it sits and why it exists

You will usually find CVC2 in the signature panel on the back of the card. It exists for remote payments, where the card is not tapped, inserted, or swiped, and the issuer needs one more check before approving the authorization.

That design matters for merchants. The code helps filter out some low-effort fraud attempts, but it was never built to prove who placed the order or who received the goods.

If you want the naming and format details spelled out, ChargePay has a separate guide on what CVV2 means and how issuers use it.

How the check works in practice

At checkout, your gateway sends the card details and the entered CVC2 for authorization. The issuer returns a response indicating whether the code matched, did not match, or could not be verified. Your fraud settings then decide whether to approve the order, decline it, or send it for review.

For a Shopify store owner, the practical meaning is straightforward:

- CVC2 is a checkout risk signal

- It can stop some bad orders before fulfillment

- It does not carry much weight by itself in a chargeback response

I see merchants rely on this field too heavily. A CVC match can help you decide whether to ship, but it rarely wins the dispute after the cardholder claims fraud.

CVC vs CVV vs CID Understanding the Terminology

A lot of merchants use "CVV" as a catch-all term. That's fine in everyday conversation, but processor logs, dispute notes, and network documentation often use brand-specific names.

Card Security Codes by Network

| Card Network | Acronym | Full Name | Digits | Location |

|---|---|---|---|---|

| Mastercard | CVC2 | Card Verification Code 2 | 3 | Back of card |

| Visa | CVV2 | Card Verification Value 2 | 3 | Back of card |

| American Express | CID | Card Identification Number | 4 | Front of card |

The names differ. The function is broadly similar. Each code is there to support remote transaction verification.

Why this matters in Shopify

Your checkout usually won't force you to care about the naming differences. Shopify Payments and most gateways handle that in the background. The customer sees one security-code field, enters the digits, and the processor routes the request based on the card brand.

Where it does matter is reporting and dispute review. If you're checking gateway responses, risk notes, or bank language, you'll see these acronyms used precisely. That can be confusing if you're trying to compare fraud filters with authentication tools such as Mastercard SecureCode or newer Identity Check flows.

If that distinction has been blurry, this explainer on what SecureCode means helps separate static card codes from issuer authentication.

CVC, CVV, and CID are cousins, not identical labels. If you're reviewing disputes, the wording in the processor report matters.

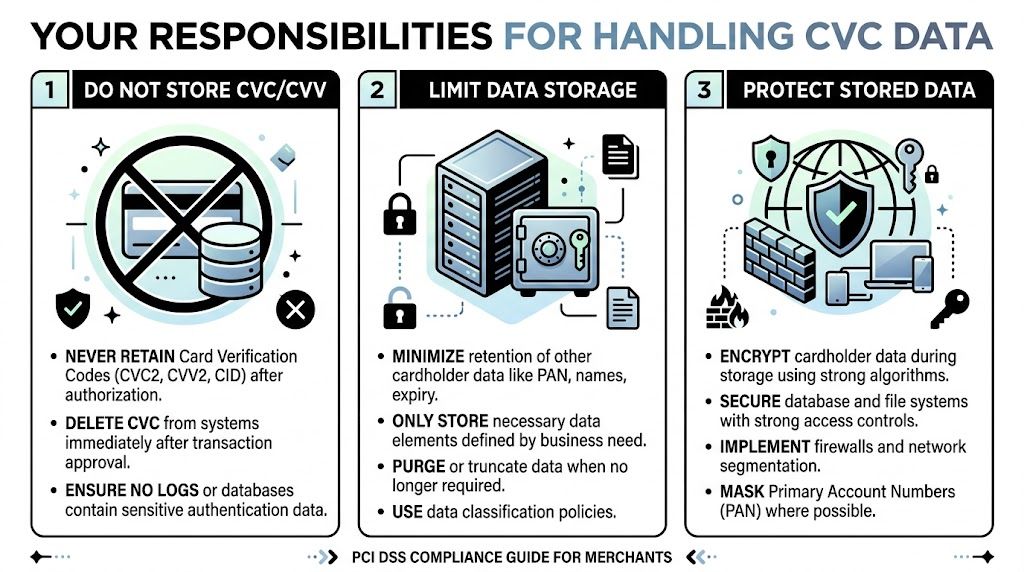

Your Responsibilities for Handling CVC Data

Collecting a CVC is normal. Storing it is where merchants get into trouble.

Mastercard's developer documentation treats CVC as a validation input in account-validation workflows, and that design is for real-time authorization use, not for keeping the code afterward, as shown in Mastercard's account validation documentation.

The rule that matters most

You must not store the CVC after authorization.

That applies to the obvious places and the less obvious ones too. Not in your database. Not in internal notes. Not in exported logs. Not on paper forms. The code is meant to be checked once and discarded.

What this means day to day

For most Shopify merchants, the platform and payment processor handle the transmission piece. Your operational risk usually shows up elsewhere:

- Support workflows: Staff asking customers to send full card details by email or chat

- Custom forms: Apps or scripts that accidentally capture sensitive fields in logs

- Recurring billing assumptions: Expecting to reuse a previously entered code for a later transaction

A better model is tokenized payment handling. Mastercard says tokenization replaces the card number with a randomly generated substitute, and in 2025 Mastercard reported that more than 30% of Mastercard transactions globally are tokenized, with more tokens enabled for digital payments than physical cards in circulation in its one-click checkout update. If you're sorting out how that changes storage risk, this overview of tokenization in payments is worth reading.

The operational takeaway

If your team ever asks, "Can we save the code for returning buyers?" the answer is no.

That's not a workaround issue. It's a boundary. The code exists to support a live authorization check, then disappear.

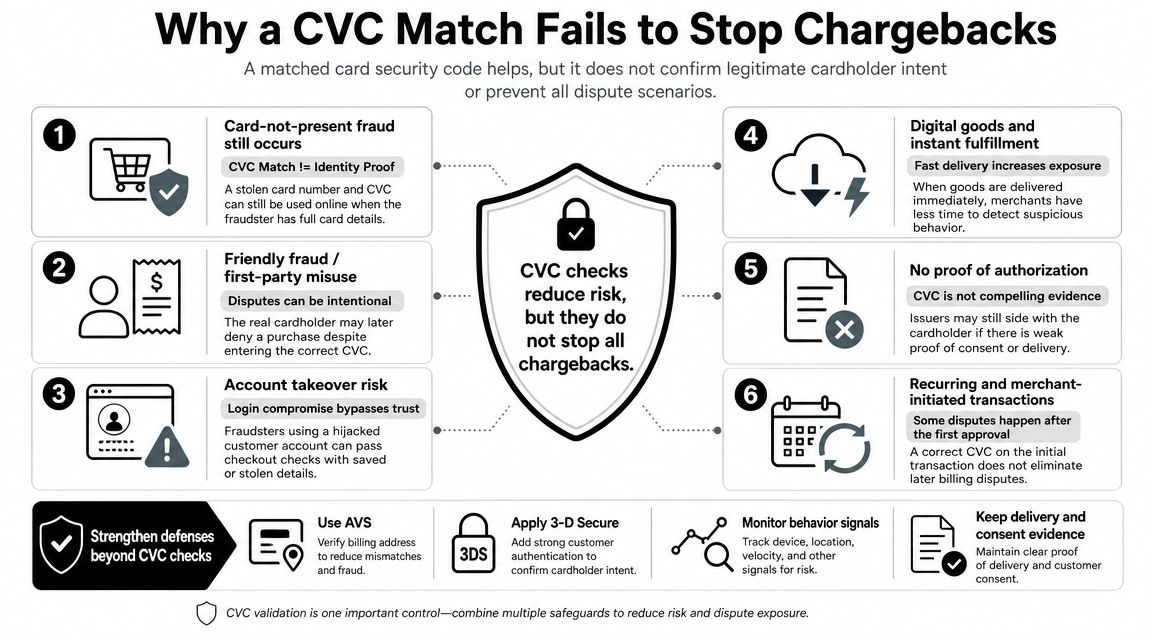

Why a CVC Match Fails to Stop Chargebacks

The biggest misconception around card verification code mastercard checks is that a successful match should protect the merchant later. It doesn't.

Chargeback evidence works on a different question. The issuer isn't asking whether someone entered the right three digits. The issuer is asking whether the legitimate cardholder authorized the transaction.

What a CVC match really proves

In a representment, a CVC match only proves possession of card data at checkout, not the identity of the user. That means it carries very little evidentiary weight against an unauthorized-use claim, especially in friendly fraud cases, according to Chargeback Gurus' explanation of card security code evidence.

That's the practical limitation most public explainers skip.

Two ways merchants still lose

True fraud

If a fraudster has the card number, expiration date, and code, the transaction can pass the CVC check. The bank may authorize it because the submitted data is correct. Later, once the actual cardholder notices the purchase, the dispute arrives.

Friendly fraud

This is often worse because the order may look completely normal. The customer places the order, receives it, then disputes it anyway. In that scenario, your "CVC matched" note doesn't answer the bank's core question about authorization and participation.

What carries more weight

When merchants ask me what tends to matter more, the answer is consistency across multiple records. A stronger response usually pulls together signals such as:

- AVS results: Billing details that align with issuer records. If you need a refresher, here's a practical guide to AVS address verification.

- Order timeline: Checkout time, account creation, order edits, and fulfillment events

- Customer communications: Order confirmation engagement, support messages, or delivery follow-up

- Delivery evidence: Tracking milestones, signed drop-off where applicable, and proof the order reached the destination

- Device and session data: Information that links the order to a coherent buyer session

If your dispute response starts and ends with "the code matched," you're usually defending the wrong point.

How to Actually Protect Your Store and Win Disputes

An order clears checkout, the CVC matches, the package gets delivered, and two weeks later the customer files a chargeback. That is the part many Shopify merchants learn too late. A CVC check helps filter bad transactions at the front end, but it rarely decides the dispute on the back end.

Mastercard and issuers are pushing merchants toward stronger authentication methods such as 3-D Secure and tokenization, as noted in this Mastercard secure authentication overview. For store owners, the practical takeaway is simple. Keep CVC enabled, but do not build your fraud strategy around it.

What a stronger setup looks like

The stores that lose less revenue usually do two things well. They screen risk before approval, and they keep the right records after the sale.

A practical setup includes:

- Front-end risk checks: AVS, device signals, velocity rules, and manual review for orders that do not fit your normal pattern

- Step-up authentication for higher-risk orders: 3DS or issuer challenge flows when the order value, product type, or behavior justifies the extra friction

- Clean post-purchase evidence: delivery scans, customer messages, accepted policies, account logins, and fulfillment timestamps that are easy to retrieve fast

If you want a broader operational checklist, Lighthouse Consultants has a useful guide on fraud prevention and risk management for businesses.

What wins when a dispute still happens

A CVC match is one data point. Issuers usually want a fuller story that shows the cardholder participated in the transaction or benefited from it.

That means tying together checkout data, account history, delivery records, customer communication, and any authentication results into one clear response. This guide to chargeback representment for merchants explains how that process works in practice.

For merchants who do not want to assemble that manually, ChargePay is one option. ChargePay says it has handled 200K+ cases, recovered $10.8M+, and holds a 4.9-star rating with a Built for Shopify badge, based on the publisher information provided for this article. The product focuses on collecting the evidence banks review and submitting disputes on time, which matters far more than citing a matched CVC and hoping that alone carries the case.

A short overview is below.

If chargebacks are eating into your Shopify revenue, ChargePay is built to automate the dispute workflow. It pulls together the evidence banks review, submits responses before deadlines, and uses a pay-per-win model. Install it from the Shopify App Store if you want a simpler way to fight friendly fraud and recover lost revenue.

.svg)

.svg)

.svg)

.svg)