You’re probably dealing with this right now. A supplier wants payment today. Payroll is due this week. A customer wants a bank-based option instead of cards. Your finance team says ACH is cheaper. Your bank says wire is faster. None of that answers the fundamental question.

The question is which payment method protects your margin when something goes wrong.

That’s the part most guides skip. They compare speed and fees, then stop. For a Shopify merchant, the difference between ach and wire isn’t just operational. It affects failed payments, fraud exposure, dispute recoverability, and how much time your team burns cleaning up avoidable messes.

If you’re already comparing processors, checkout tools, and bank rails, this e-commerce payment provider comparison is useful context because payment method decisions never live in isolation. They affect your store operations, support load, and dispute volume too.

ACH vs Wire Which is Better for Your Shopify Store

A Shopify merchant I talk to all the time looks like this. They use cards for customer checkout, but behind the scenes they still need to move money constantly. They pay contractors, send vendor deposits, collect some subscription payments by bank account, and occasionally rush a payment to lock inventory before a launch.

Then the confusion starts.

Finance says ACH because it keeps costs down. Ops says wire because they need certainty. Support says neither matters until a customer disputes a debit they authorized. That’s where the clean spreadsheet answer falls apart.

Here’s the straight answer. ACH is usually the better default for routine domestic business payments. Wire is better for large, urgent, or international transactions where delay creates bigger problems than fees. But if you stop there, you miss the revenue risk.

Quick comparison

| Factor | ACH | Wire |

|---|---|---|

| Best use | Routine domestic payments | Urgent or high-value transfers |

| Processing style | Batch-based | Individual transfer |

| Merchant mindset | Cheap and scalable | Fast and final |

| Dispute risk | Higher if the payment can be challenged | Lower after settlement |

| Typical store use | Payroll, recurring vendor payments, subscriptions | Supplier deposits, international settlements, time-sensitive transfers |

My recommendation

If you run a Shopify store, don’t ask “Which one is better?” Ask two sharper questions:

- Is this payment routine or urgent: Routine usually points to ACH. Urgent usually points to wire.

- What happens if the payer disputes it: If reversibility would hurt you, that risk belongs in the decision.

Practical rule: Cheap payments aren’t cheap when you spend the next month fighting reversals.

Most merchants don’t lose money because they picked the “wrong” rail once. They lose money because they use ACH broadly without a process for disputes, evidence, and fraud controls. That’s why this choice matters more than it seems.

Understanding the Mechanics of ACH and Wire Payments

A customer pays from a bank account, the order ships, and then the payment comes back short or gets challenged. That is where merchants get hurt. ACH and wire both move money bank-to-bank, but the path each payment takes changes how much reversal risk lands on your Shopify store.

ACH runs on a clearing network built for volume. Banks collect payment instructions, submit them in batches, and settle them on a schedule instead of handling each transfer one at a time.

That setup makes ACH a practical choice for repeat business activity. It fits subscriptions, account-based billing, vendor payments, and other predictable flows. It also creates delay between authorization, settlement, and return activity. For a merchant, that gap matters because trouble often shows up after you treated the payment like good money.

If ACH is part of your checkout or invoicing flow, learn the failure points before you scale it. ACH return charges and what merchants should watch lays out the fees, return reasons, and operational problems that eat margin.

Wire transfers work differently. The sending bank pushes a specific payment directly through a wire network to the receiving bank. There is no batch queue in the middle. That is why wires are used for supplier deposits, inventory purchases, and other payments where timing and settlement certainty matter more than low fees.

The difference is operational, but it turns into a revenue issue fast.

With ACH, merchants can collect funds in ways that are convenient for recurring billing and account-to-account payments. That convenience comes with more exposure to returns, authorization disputes, and account problems. With wires, the payment is far more final once settled, so the sender usually has less room to unwind the transfer after the fact. If you sell high-risk products, custom goods, or large-ticket inventory, that distinction matters more than the fee line on your bank dashboard.

One more point gets missed in basic ACH vs. wire explainers. ACH is often built around reusable payment relationships. Wire is usually a deliberate, one-off instruction. Reusable payment setups make operations easier, but they also create more opportunities for billing complaints, mandate disputes, and fraud tied to stored bank details.

For a broader banking-side explanation, these Resolut insights on electronic payment processing are a useful companion read.

Merchants who understand the mechanics make better risk decisions. They do not just ask which rail is faster or cheaper. They ask which rail leaves the fewest ways for revenue to disappear after the sale.

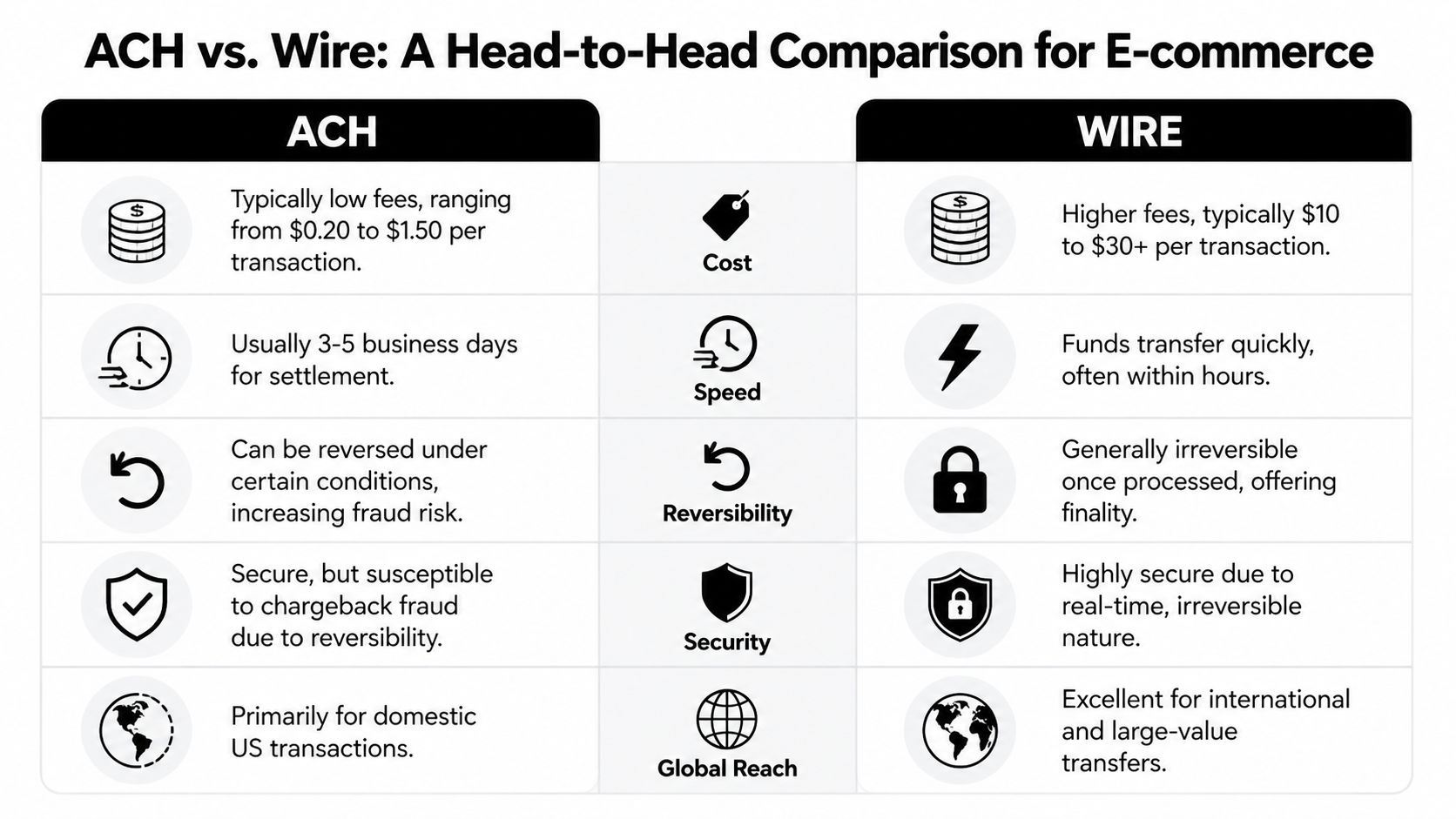

A Head-to-Head Comparison for E-commerce

A Shopify merchant gets two very different problems from ACH and wire. One can look cheap and create dispute exposure later. The other costs more upfront and gives you far less room for reversal drama. If you only compare fees and speed, you miss the part that hits revenue.

Use this comparison with a risk mindset, not a banking glossary.

| Criteria | ACH | Wire |

|---|---|---|

| Cost profile | Lower cost for routine transactions | Higher bank fees |

| Speed | Slower settlement, often over business days | Faster movement, often same day domestically if sent before cutoff |

| Finality | Can be reversed in some situations | Generally final after settlement |

| International fit | Limited for global use | Better for cross-border transfers |

| Operational fit | Strong for recurring payments and scheduled pulls | Better for one-off urgent transfers |

Cost matters after you price in dispute risk

ACH usually wins on raw transaction cost. That makes it the practical choice for recurring vendor payments, subscription billing, and scheduled domestic transfers.

But low cost does not automatically mean low expense. If ACH creates more returns, account disputes, or internal cleanup for your team, the savings disappear fast. Wire fees are expensive by comparison, but they can be the cheaper option on a high-value transaction where payment finality protects your margin.

That is also why smart operators look past the bank fee and review the full payment stack. This guide to Shopify payment processing fees and hidden margin impact gives the wider cost picture.

Speed matters less than certainty

For e-commerce, the question is not “Which one moves faster?” It is “Which one lets me move inventory, release goods, or pay a supplier without reopening the transaction later?”

Use a wire when timing and confirmation affect fulfillment. Supplier deposits, urgent inventory purchases, and other large one-off payments belong here. Use ACH for repeatable payments your team can schedule and monitor without urgency.

Reversibility decides a lot of the risk

This is the part many payment guides soften. They should not.

ACH gives customers and banks more ways to challenge or return a payment. That can help with legitimate errors. It also creates more ways for a merchant to lose already-booked revenue, especially on recurring billing, high-ticket orders, and any setup where bank details stay on file.

Wire is stronger on finality once settled. That does not make it the default choice for every payment. It makes it the safer rail when the amount is large, the product is custom, or a dispute would hurt more than the fee.

The cheaper payment rail often becomes the more expensive one after a return, a fraud claim, or hours of manual recovery work.

Operational fit decides whether finance stays clean

ACH fits systems. Wire fits exceptions.

If your store runs repeat transactions, ACH is easier to reconcile in batches and easier to build into normal workflows. If a payment needs extra approval, specific documentation, or tight control before money moves, wire is usually cleaner because each transfer is intentional and easier to review on its own.

That difference matters for fraud control too. High-volume convenience creates more chances for billing complaints and unauthorized payment issues. Deliberate, one-off transfers reduce that exposure, even if they are less convenient.

Taking Your Shopify Store Global ACH vs Wire

Your Shopify store lands an international order. The sale looks great until the payment method creates a margin problem, a reconciliation mess, or a dispute you now have to fight across borders.

That is where the difference between ACH and wire starts affecting revenue, not just operations.

ACH is still mainly a U.S. bank-payment rail. If your store collects domestic bank debits, that works. If you need to pay overseas suppliers, handle international partners, or accept large cross-border bank payments, ACH runs out of room fast.

Wire is usually the practical option for international movement of funds because it can move across banking systems. The tradeoff is simple. Wires cost more, so they make less sense for low-ticket consumer orders where fees chew up margin.

What changes when you go international

Cross-border payments raise the stakes on disputes.

According to Wise’s ACH versus wire comparison, global payments were projected to hit $2.1T in 2025, with 40% tied to Shopify volume. Wise also noted that in 2024, chargeback win rates could drop to 45% for disputes crossing jurisdictions, compared with 75% for domestic issues. That gap matters more than the transfer fee. A cheaper payment method stops looking cheap when your odds of keeping the revenue fall.

International selling also creates more points of failure. Shipping timelines are longer. Customer expectations are harder to manage. Documentation standards get stricter the second a bank, processor, or card network sees a cross-border complaint. If you are expanding overseas, review this guide to cross-border e-commerce risk and operations before your dispute rate forces the lesson.

The practical global playbook

For Shopify merchants, the smart setup is straightforward:

- Use ACH for U.S. domestic bank payments. It fits recurring billing and routine stateside cash movement.

- Use wire for international supplier payouts and large cross-border transfers. The higher fee often buys you better control and stronger payment finality.

- Set stricter documentation rules for international orders. Save authorization records, delivery proof, customer communication, and any country-specific terms from day one.

- Do not use one rail for every cross-border scenario. The wrong payment method can create avoidable loss even when the sale itself was legitimate.

International growth increases revenue and dispute exposure at the same time. Your payment method decides how much of that revenue you actually keep.

Plenty of merchants learn this after the fact. They expand into new markets, keep the same payment habits, then watch margin disappear into fees, payment reversals, support hours, and harder-to-win disputes. That is avoidable if you choose the rail based on revenue risk, not convenience.

How Your Payment Choice Impacts Chargebacks and Fraud

At this point, merchants usually get burned.

ACH looks cheap, flexible, and customer-friendly. Then a customer disputes a legitimate bank debit. Maybe it was a subscription renewal. Maybe they forgot the purchase. Maybe they’re gaming the system. Now your team has to prove the charge was valid, and the clock starts immediately.

ACH creates more room for friendly fraud

The problem isn’t that ACH is unsafe. The problem is that reversible payments invite abuse.

According to Mercury’s ACH versus wire article, chargebacks cost U.S. merchants $32.5B in 2024. The same verified data states that analysis of over 200,000 cases shows 70% of e-commerce disputes are related to ACH, and without an automated defense, merchants lose these fights 60% to 70% of the time.

That should change how you think about bank payments immediately.

If your store accepts ACH debits, you need more than a billing system. You need a documented defense process. Order records, customer communication, fulfillment proof, recurring authorization records, and reason-code handling all matter. This overview of chargeback prevention for Shopify merchants covers the operational side that is often neglected.

Wire reduces one risk, but creates another constraint

Wire’s biggest strength is finality. Once settled, it generally doesn’t create the same post-payment reversal fight that ACH does. That makes wire useful for high-stakes transfers where certainty matters.

But don’t twist that into “wire is safer for e-commerce.” It’s not practical for regular DTC sales. It’s too expensive, too manual, and too rigid for common consumer transactions. You’re not going to run a normal Shopify checkout business on wire transfers.

What a merchant should actually do

Use ACH with discipline, not blind optimism.

- Tighten authorization records: If you can’t prove consent cleanly, you’re exposed.

- Store fulfillment evidence fast: Tracking, delivery confirmation, and customer messages matter when a dispute lands.

- Watch recurring billing complaints: A lot of “fraud” is really buyer regret or confusion.

- Escalate high-value one-off transfers to wire: Finality has value when the amount or urgency justifies it.

A short walkthrough can help if your team is building a response workflow:

Merchants rarely lose disputes because they had no evidence at all. They lose because the evidence wasn’t organized, submitted correctly, or submitted in time.

That’s the ugly truth behind ACH dispute loss. The rail itself isn’t the whole problem. Weak process is.

When to Use ACH and When to Use a Wire Transfer

You don’t need a big framework here. You need a usable rule set.

Use ACH for repeatable domestic payments

ACH is the right choice when the payment is predictable, scheduled, and operational.

Examples:

- Monthly payroll or contractor payments: Low cost matters more than instant settlement.

- Recurring domestic vendor bills: If the relationship is stable and timing is known, ACH is the cleaner option.

- Subscription or invoice collection by bank account: It fits the rail, but only if your authorization and dispute process are tight.

Use wire for urgency, finality, and international reach

Wire makes sense when delay creates real business damage or when the payment needs to move outside ACH’s comfort zone.

Common situations:

- Urgent supplier deposits: If inventory depends on same-day movement, use wire.

- International supplier payments: Wire is usually the more practical option.

- Large one-time settlements: The fee is easier to justify when certainty matters.

Don’t use the same payment logic for customers and vendors

Merchants often blur those lines. That’s a mistake.

Customer-facing payments need convenience and dispute readiness. Back-office payments need reliability and cost control. Vendor and treasury decisions are not the same as checkout decisions.

If your team still mixes up merchant account logic with gateway logic, this guide on merchant account versus payment gateway differences helps clean up the basics.

A simple decision filter

Ask these questions in order:

- Is this domestic and routine? Use ACH.

- Is it urgent or high-stakes? Use wire.

- Would a reversal be painful? Lean toward wire for qualifying transactions.

- Can your team defend a dispute cleanly? If not, be careful with ACH pulls.

That’s usually enough to make the right call.

Our Recommended Payment Strategy for Shopify Merchants

Most Shopify merchants shouldn’t choose ACH or wire. They should use both on purpose.

ACH should be your default workhorse for domestic, recurring, operational payments. It keeps routine money movement practical. Wire should stay in your toolbox for urgent, high-value, and international transactions where speed and finality matter more than fee savings.

That hybrid approach is the sane answer.

The strategy I’d recommend

- Default to ACH for domestic operations: Payroll, routine vendor payouts, and scheduled transfers belong here.

- Reserve wire for exception cases: International settlements, urgent inventory payments, and large one-off transfers are better candidates.

- Build your payment policy around dispute exposure: If a transaction type attracts reversals, don’t evaluate it on fees alone.

- Review expansion plans through a finance lens: If you’re growing outside the U.S., this guide to scaling UK online businesses is a useful operations-side resource.

What merchants usually get wrong

They optimize for visible fees and ignore invisible loss.

A cheap ACH workflow can turn expensive when your team spends hours responding to disputes, misses deadlines, or loses valid revenue because evidence is scattered across Shopify, email, shipping systems, and customer support tools. A wire can feel expensive up front, but that fee may be trivial compared with the cost of a delayed supplier payment or a failed inventory launch.

Bottom line: Use ACH for efficiency. Use wire for certainty. Build your process around the downside of each.

That is the essential distinction between ACH and wire for a Shopify merchant. One helps you scale routine payment movement. The other helps you protect high-stakes transactions. The stores that handle this well do not obsess over one rail. They match the rail to the risk.

If chargebacks are eating your margin, install ChargePay from the Shopify App Store. It’s built for Shopify, carries a 4.9-star rating, and uses a pay-per-win model so you only pay when money is recovered. ChargePay handles the dispute process for Shopify merchants who are tired of losing revenue to friendly fraud, messy evidence collection, and missed response windows.

.svg)

.svg)

.svg)

.svg)