You already know the promise of subscriptions. Predictable revenue, repeat customers, cleaner forecasting.

What you may not see clearly is where that revenue slips away.

For a Shopify store, processing recurring payments isn't just billing infrastructure. It's your first fraud filter, your churn control system, and your evidence trail when a customer disputes a charge. If that system is weak, you don't just lose renewals. You lose revenue twice. First on the failed payment, then again on the chargeback.

Your Recurring Revenue Is Leaking. Here Is Why

A lot of Shopify merchants think recurring billing problems start when a customer cancels. They usually start earlier, when a renewal fails, a card expires, a bank declines the charge, or the customer doesn't recognize the transaction and disputes it instead of contacting support.

That matters because the subscription economy is huge and still growing. In 2024, the global subscription industry reached an estimated $3 trillion, up 50% year over year, and up to 40% of subscriber loss comes from involuntary churn caused by failed payments, according to RapidCents' subscription industry breakdown. If you sell replenishment products, memberships, curated boxes, or paid access, you're operating inside that reality whether you track it tightly or not.

The upside of subscriptions is obvious. If you want a quick refresher on why brands keep moving in this direction, this overview of How subscription models grow e-commerce is worth a read. The downside is less obvious. Recurring revenue feels stable, but it's only stable if your payment system keeps collecting, retrying, documenting, and communicating.

Practical rule: Every failed recurring payment is a retention problem first and a chargeback risk second.

When a renewal doesn't go through, customers get confused. Some update their card. Some ignore the email. Some see a statement later and file an "unauthorized" claim because they forgot they subscribed in the first place. That's why smart merchants treat processing recurring payments as part of revenue defense, not just checkout ops.

If you're trying to tighten the whole funnel, this guide to chargeback prevention for Shopify merchants helps connect payment setup with dispute reduction.

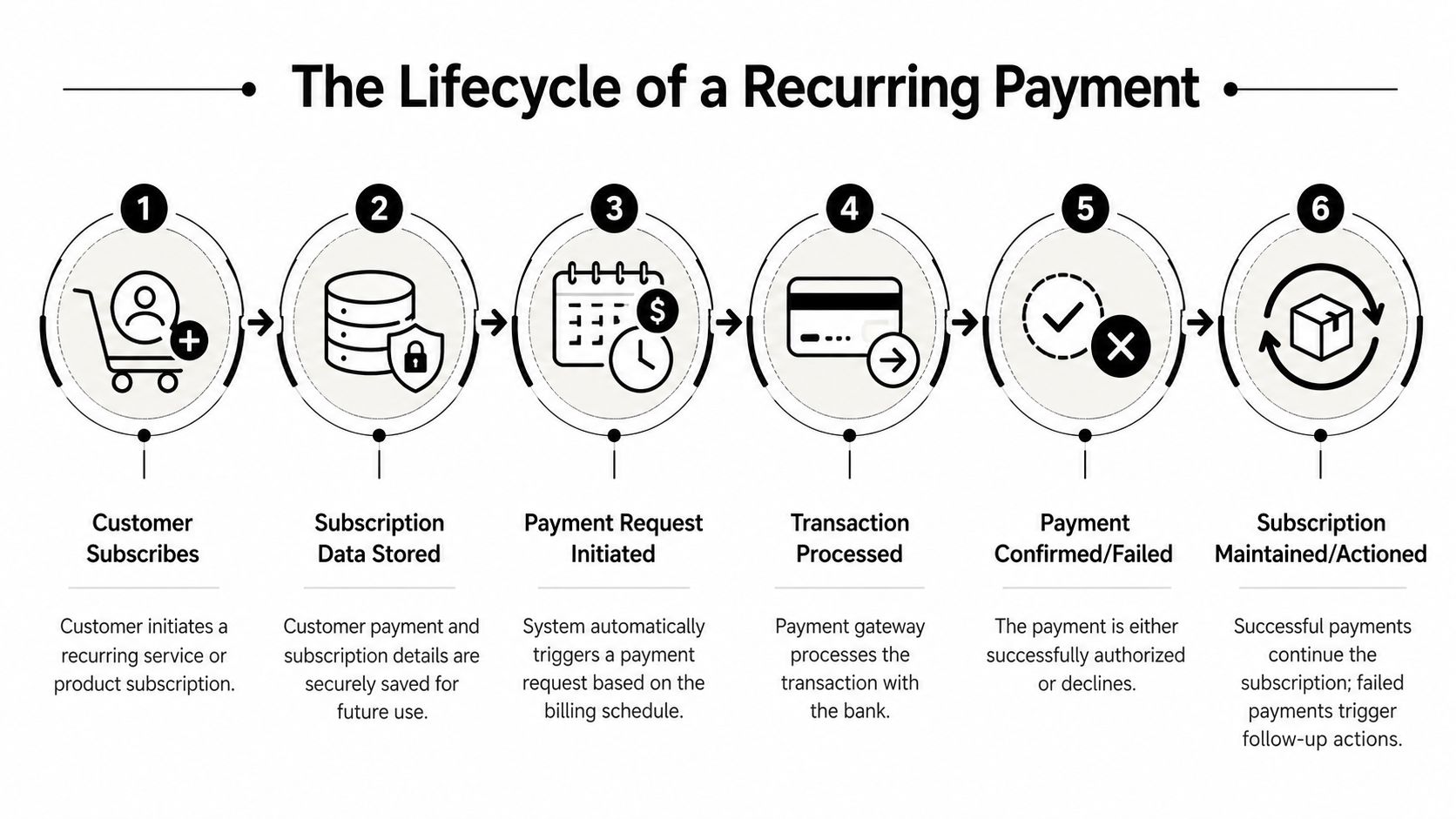

The Lifecycle of a Recurring Payment

The technical path of a recurring charge isn't complicated once you strip away processor jargon. But each step matters because every weak handoff creates either a failed payment or a dispute you have to fight later.

It starts with the first approval

The first payment is the most important one. That's when the customer enters their payment method, agrees to the recurring terms, and the issuing bank approves or declines the transaction.

Think of this as the digital handshake. Your store says, "This customer wants to buy and agrees to future charges under these terms." The bank either accepts that handshake or rejects it. If this step is messy, everything downstream gets weaker.

For Shopify merchants, this means you need clean checkout pages, clear subscription terms, and order records that match what the customer saw when they subscribed.

Then tokenization does the heavy lifting

After the first approved payment, you shouldn't be storing raw card data yourself. Your processor or subscription app stores a token instead. A token is like a secure vault key. It points to the payment method without exposing the actual card number.

That matters for two reasons:

- Security risk drops: You reduce your exposure to sensitive card data.

- Chargeback defense improves: Your records are cleaner because the recurring relationship ties back to an approved initial setup.

If you want a deeper explanation of where security and payment handling split, this article on payment reconciliation in e-commerce is useful once renewals start flowing across orders, payouts, and failed attempts.

A recurring payment is easier to defend when the original signup, the stored credential, and every renewal event all line up in your records.

Billing runs on schedule, not on memory

Once the customer is enrolled, your billing system triggers charges on the schedule they accepted. Monthly. Quarterly. Annual. Whatever your plan structure is.

Many merchants make the wrong assumption. They think recurring billing is "set it and forget it." It isn't. It's "set it and monitor it."

Each billing cycle typically follows a simple flow:

- The system checks the billing date

- It triggers a payment request

- The gateway sends that request to the processor

- The processor routes it to the bank

- The bank approves or declines

- Your store updates the subscription status

That final update is important. If a payment fails but your fulfillment workflow still ships the product, you've created a preventable loss. If a payment succeeds but the customer doesn't receive confirmation, you've created confusion that can turn into a dispute.

Webhooks are the digital messengers

A webhook is just an automated message between systems. When a payment succeeds, fails, or needs action, the processor sends that event to your store or app stack.

Without reliable webhooks, your recurring payment operation gets sloppy fast. Orders don't update on time. Dunning emails don't trigger. Access doesn't pause when it should. Support agents work from bad information.

For a Shopify merchant, good processing recurring payments infrastructure means these messages fire correctly and quickly:

- Payment succeeded

- Payment failed

- Card updated

- Subscription paused

- Subscription canceled

When those events stay in sync, your customer experience improves and your evidence gets stronger. When they don't, you get complaints, refunds, and chargebacks.

Mastering Payment Compliance and Security

Most merchants treat compliance like paperwork. That's a mistake.

Compliance is part of your chargeback strategy. If your recurring billing stack is sloppy on security, consent, or authentication, you're giving fraudsters and confused customers an easier path to dispute your charges.

The reason is simple. The payments market is massive. Global digital payments are projected to reach about $157 trillion in 2025, fraud losses have exceeded $40 billion in recent years, and 71% of businesses reported attacks in 2023, based on Clearly Payments' market analysis. Fraud follows volume. If your store runs recurring charges, you're in the blast radius.

PCI DSS is not optional admin work

PCI DSS exists to reduce card data exposure. For a Shopify merchant, the practical takeaway is straightforward. Don't build weird workarounds. Don't store sensitive payment data in places it doesn't belong. Don't let apps or processes create avoidable liability.

Your processor and subscription stack should handle secure storage properly. Your job is to choose tools that don't force your team into manual handling of card details through email, notes, spreadsheets, or support tickets.

If you want a practical comparison of the underlying tools involved, this Shopify payment guide gives a helpful overview of how payment systems fit together.

Consent is your dispute evidence

For recurring billing, customer consent isn't a legal footnote. It's one of the first things card issuers and networks care about when a charge is challenged.

You need records that show:

- What the customer bought

- When they agreed to recurring billing

- How often they would be charged

- What amount or pricing structure they accepted

- How they could cancel

- What happened at signup

If any of this is vague, you're creating future chargeback pain for yourself. The cleanest subscription businesses treat signup records like insurance. Screenshots of checkout terms, timestamps, plan details, IP logs where available through approved tools, and confirmation emails all help build a defensible story.

The easiest chargeback to fight is the one where your records tell the whole story without your team having to explain it.

Authentication matters most at signup

Recurring payments become card-not-present after the initial setup. That means the first transaction carries extra weight. It's your chance to verify the customer properly, capture consent, and prove the billing relationship started legitimately.

For stores serving customers in regions with stronger authentication requirements, you need to support that flow correctly. The extra friction can feel annoying in the moment, but it's usually cheaper than dealing with unauthorized transaction disputes later.

A strong setup usually includes:

- Clear plan terms at checkout

- A visible recurring billing disclosure

- Strong authentication where required

- Immediate post-purchase confirmation

- Stored records that support later disputes

For a technical breakdown of how payment credentials are protected after signup, this explanation of encryption vs tokenization in payments is worth reviewing.

Compliance should lower support volume

When merchants do this right, support gets easier. Customers know what they bought. They recognize the timing. They can find cancellation steps. Banks see cleaner evidence if a dispute happens.

When merchants do it wrong, compliance problems show up as revenue problems. More confusion. More "I didn't authorize this" claims. More chargebacks that could have been avoided before the first renewal ever ran.

Smart Operations to Minimize Failed Payments and Disputes

Most recurring revenue losses don't come from one catastrophic error. They come from a pile of small operational misses. A vague billing descriptor. A weak retry sequence. No pre-billing email. A support team that can't quickly explain a renewal.

That's fixable.

Fix the statement descriptor first

If customers don't recognize your charge on their bank statement, you're inviting unnecessary disputes.

Your billing descriptor should match your store name or brand name closely enough that a customer instantly knows what they bought. If your legal entity name is different from your storefront, clean that up where your processor allows it. Add a support phone number or URL if the payment setup supports that option.

This one change helps reduce "unrecognized transaction" claims before they start.

Send pre-billing notices people can understand

A pre-billing notice works because it removes surprise. Surprise is the fuel behind a lot of friendly fraud.

Keep it simple. Tell the customer what is renewing, when they'll be charged, what amount to expect, and how to manage or cancel the subscription if they no longer want it.

A practical pre-billing email usually includes:

- Product or membership name

- Renewal date

- Amount

- Last four digits or payment method label, if available through your system

- Manage subscription link

- Support contact

For annual plans and higher-ticket subscriptions, these messages matter even more because the customer may not think about the charge often.

Build a dunning sequence that actually recovers money

When a renewal fails, don't send one generic email and hope for the best. Use a structured dunning flow.

The point of dunning isn't just collecting the payment. It's also preventing customer confusion from turning into cancellation, support friction, or a dispute.

A strong dunning flow usually includes a mix of:

- Immediate failure notice

- Clear update-payment link

- Timed retries for likely temporary failures

- A warning before access pauses or shipments stop

- A final message confirming the account outcome

Keep the language plain. "We couldn't process your renewal. Update your payment method here." works better than clever copy.

Here's a useful walkthrough that shows how recurring billing issues are often handled in practice:

Match the operation to the chargeback risk

Recurring billing operations work best when each action has a clear defensive purpose.

| Operational move | Why it matters | Chargeback risk it reduces |

|---|---|---|

| Clear descriptor | Customers recognize the charge | Unrecognized transaction disputes |

| Pre-billing reminder | Removes surprise before renewal | Friendly fraud and refund disputes |

| Payment receipt after successful renewal | Confirms the transaction happened | Confusion-based unauthorized claims |

| Smart dunning emails | Helps the customer update details fast | Involuntary churn that later turns into disputes |

| Easy cancellation path | Reduces frustration | Escalation to bank instead of support |

Operator's view: If customers can find the charge, the plan terms, and the cancel button, many disputes never happen.

Consider alternative payment rails where they fit

Cards aren't the only option forever. For some customer segments and markets, real-time payments can cut failed payments by up to 40% and support the 167 million unbanked individuals projected to gain accounts by 2028, according to the U.S. Chamber's recurring payments guide.

That doesn't mean every Shopify subscription brand should rush to replace card billing. It does mean you should watch where payment friction comes from. If a segment of your customers struggles with card declines, card updates, or friction around verification, alternative rails may reduce both failed payments and friendly fraud pressure.

Processing recurring payments well means using the right payment method for the right customer, then communicating every charge clearly.

Why Payments Fail and How to Recover the Revenue

Not every failed payment deserves the same response. Some failures are temporary. Others are dead ends. If your system treats all declines the same, you either leave money on the table or annoy customers with pointless retries.

The cleanest way to manage this is to separate soft declines from hard declines.

Soft declines need a recovery plan

A soft decline usually means the payment could work later. The card may still be valid. The issue may be temporary. Timing matters here.

Examples include insufficient funds, a temporary bank block, or a processor issue. In these cases, retrying can recover revenue without asking the customer to start over. But retries should be deliberate. Random hammering doesn't help.

Hard declines need customer action

A hard decline means the stored payment method probably won't work again without a change. The card may be closed, replaced, reported lost, or blocked permanently.

Many merchants waste time in situations like this. They keep retrying a dead card, the customer keeps getting failure notices, and irritation builds. That irritation can easily turn into a dispute later if the customer thinks your billing system is messy or aggressive.

For merchants working with bank debits, this guide to managing direct debit rejections is a useful parallel because the recovery logic is similar. You need to know whether the failure is temporary, final, or customer-driven.

Common recurring payment failures and solutions

| Decline Type | Common Reason | What It Means | Your Next Step |

|---|---|---|---|

| Soft decline | Insufficient funds | The account may fund later | Retry on a sensible schedule and notify the customer |

| Soft decline | Temporary bank issue | The issuer may approve later | Retry later and monitor the next attempt |

| Soft decline | Processor or network interruption | The failure may not be customer-related | Retry after the system stabilizes |

| Hard decline | Expired card | The stored credential is outdated | Ask the customer to update the payment method |

| Hard decline | Lost or replaced card | The old card should not be retried indefinitely | Trigger card update messaging immediately |

| Hard decline | Closed account | The payment method is no longer usable | Stop retries and request a new payment method |

| Hard decline | Suspected fraud block | The issuer wants stronger validation or a new method | Pause automated retries and route the customer to support |

Recovery should protect the customer experience

A recovery sequence should do two things at once. Recover the money and keep the customer calm.

That means your failure messaging needs to be specific without sounding accusatory. "Your renewal didn't go through. Update your payment method to avoid interruption" is better than a vague failed payment notice with no next step. The customer should know what happened, what they need to do, and what happens if they ignore it.

If you're handling bank payment failures too, this overview of ACH return charges and what they mean helps when recurring payments go beyond cards.

Don't confuse persistence with strategy

Some merchants think more retries always mean more recovered revenue. That's not true. Good recovery depends on matching the retry behavior to the failure type.

Retry soft declines. Stop hammering hard declines. Tell the customer what's happening. Pause fulfillment or access when necessary. Keep records of every attempt and message.

That approach recovers more revenue and creates fewer angry cardholders.

The Hidden Risk of Recurring Payments and Friendly Fraud

A lot of chargebacks in subscription businesses are not pure stolen-card fraud. They're confusion, convenience, or opportunism dressed up as fraud claims.

That's why recurring billing is tricky. A customer signs up once, then charges continue automatically. Over time, some customers forget the subscription, don't recognize the descriptor, or decide going through the bank is easier than contacting support. Others know the charge is valid and dispute it anyway.

Why subscriptions get targeted

After signup, recurring payments run as Card-Not-Present transactions, which makes them structurally vulnerable. As noted in this research on recurring billing fraud and CNP exposure, fraudsters can use stolen card details to start subscriptions, and those transactions can later turn into chargebacks that hurt the merchant long after the original signup.

The issue isn't limited to criminals using stolen cards. The same setup creates room for friendly fraud because each later renewal happens without the cardholder being physically present or actively authenticating again.

Friendly fraud is often predictable

You can usually spot the patterns before the dispute lands.

Common triggers include:

- The customer forgot they subscribed

- The descriptor didn't match the brand they remember

- The renewal amount surprised them

- Cancellation was harder to find than the bank dispute option

- A household member signed up and someone else saw the charge

- The customer wants a refund but chooses a chargeback instead

None of this means your chargebacks are automatically unwinnable. It means your process has to account for human behavior, not just payment logic.

A subscription merchant who only thinks about payment approval rates is missing the real problem. Approved charges can still become disputed charges.

Manual dispute handling breaks at scale

Friendly fraud is one reason manual workflows fail so badly. When a dispute arrives, you need the signup record, renewal history, customer communications, cancellation terms, receipts, and any evidence of use or fulfillment. You also need it fast.

If your team is digging through Shopify orders, email tools, subscription apps, and help desk threads by hand, you're already behind. Deadlines don't care how messy your stack is.

Prevention starts before the dispute exists

The most effective recurring payment systems reduce friendly fraud before representment is ever necessary. That usually means:

- Clear recurring consent at signup

- Recognizable billing descriptors

- Renewal reminders

- Instant receipts

- Easy cancellation

- Accurate records across your payment and order systems

Those controls don't eliminate chargebacks. They make chargebacks more preventable and more defensible.

The merchants who protect recurring revenue well don't treat friendly fraud like bad luck. They treat it like an operating problem with clear causes.

Your Automated Defense on Shopify and PayPal

If you run subscriptions on Shopify, you already have enough to manage. Billing logic, retries, support tickets, refunds, and renewals are hard enough before disputes arrive. Once chargebacks hit, the manual approach falls apart fast.

You have to gather order data, match it to the original subscription terms, pull customer communications, package evidence, and submit everything before the deadline. Do that across Shopify and PayPal, and the admin load gets ugly.

Automation stops being a nice extra and becomes the only sensible option. Chargebacks in recurring billing are repetitive, evidence-heavy, and deadline-driven. AI is good at exactly that work when it's trained on dispute outcomes and connected directly to the systems where your proof lives.

If you're selling through both channels, this overview of ChargePay's Shopify and PayPal chargeback workflow shows how one connected process can cover both.

ChargePay is built for this specific problem. It automatically handles the dispute lifecycle for Shopify merchants, including friendly fraud detection, evidence assembly, and on-time submission. According to ChargePay's platform data, it has a 92.4% win rate, has handled 200K+ disputes, and has recovered $10.8M+ for merchants. It also holds a 4.9-star rating on the Shopify App Store and carries the Built for Shopify badge.

If you're still fighting subscription chargebacks by hand, you're wasting time and giving up recoverable revenue.

Install ChargePay from the Shopify App Store and stop letting recurring payment disputes drain your margin. It's built for Shopify, rated 4.9 stars, and priced pay-per-win, so you only pay when ChargePay recovers your money.

.svg)

.svg)

.svg)

.svg)