You check your Shopify payout after an international order and something feels off. Revenue looks fine. The customer paid full price. But the profit is thinner than a similar sale from a nearby state.

That gap often starts with mastercard international interchange rates. They sit underneath your total processing cost, and they usually climb when the card is issued in another country, when currency conversion is involved, and when the order is online instead of in person. For a Shopify merchant, that means global growth can look great at the top line even as it squeezes margins at checkout.

The part that catches many store owners is that higher payment cost is only one side of the problem. The same international orders that cost more to process also tend to create more friction when something goes wrong, especially around fraud reviews, customer confusion, and chargebacks. If you're selling cross-border, you need to understand both.

Why Did My International Sale Earn Less Profit

A common Shopify story goes like this. You sell the same product to two customers. One buys from California. One buys from the UK. Shipping may be different, taxes may be different, and returns may be different. But even before those factors, the payment itself can cost more on the international order.

That happens because card payments aren't priced as one flat fee behind the scenes. Mastercard sorts transactions into different categories based on where the card was issued, what kind of card it is, and how the payment was accepted. International ecommerce transactions often land in more expensive buckets.

If you've been expanding into new markets, this is part of the reason cross-border commerce feels rewarding and messy at the same time. A broader customer base can increase demand, but each order can carry more hidden payment friction than a domestic sale. If you're navigating that shift, this guide on cross-border e-commerce for Shopify brands helps frame the bigger picture.

Why the same order value can produce different profit

A $100 order isn't always a $100-quality sale to your business.

When the buyer uses a foreign-issued Mastercard, the transaction may involve:

- Cross-border processing that routes through additional network steps

- Currency exposure if the customer pays in one currency and you settle in another

- Higher fraud review pressure because online international transactions are harder to verify than local in-person payments

Those extra layers show up in your payment cost, even if the customer experience looked smooth.

Practical rule: If international orders consistently feel less profitable than domestic ones, don't just review shipping and ad spend. Review payment mix, card origin, and dispute patterns too.

The frustrating part is that many merchants only notice this after volume grows. At first, a few international orders don't move the needle. Then global sales become meaningful, and margins start slipping in a way that standard Shopify reports don't fully explain.

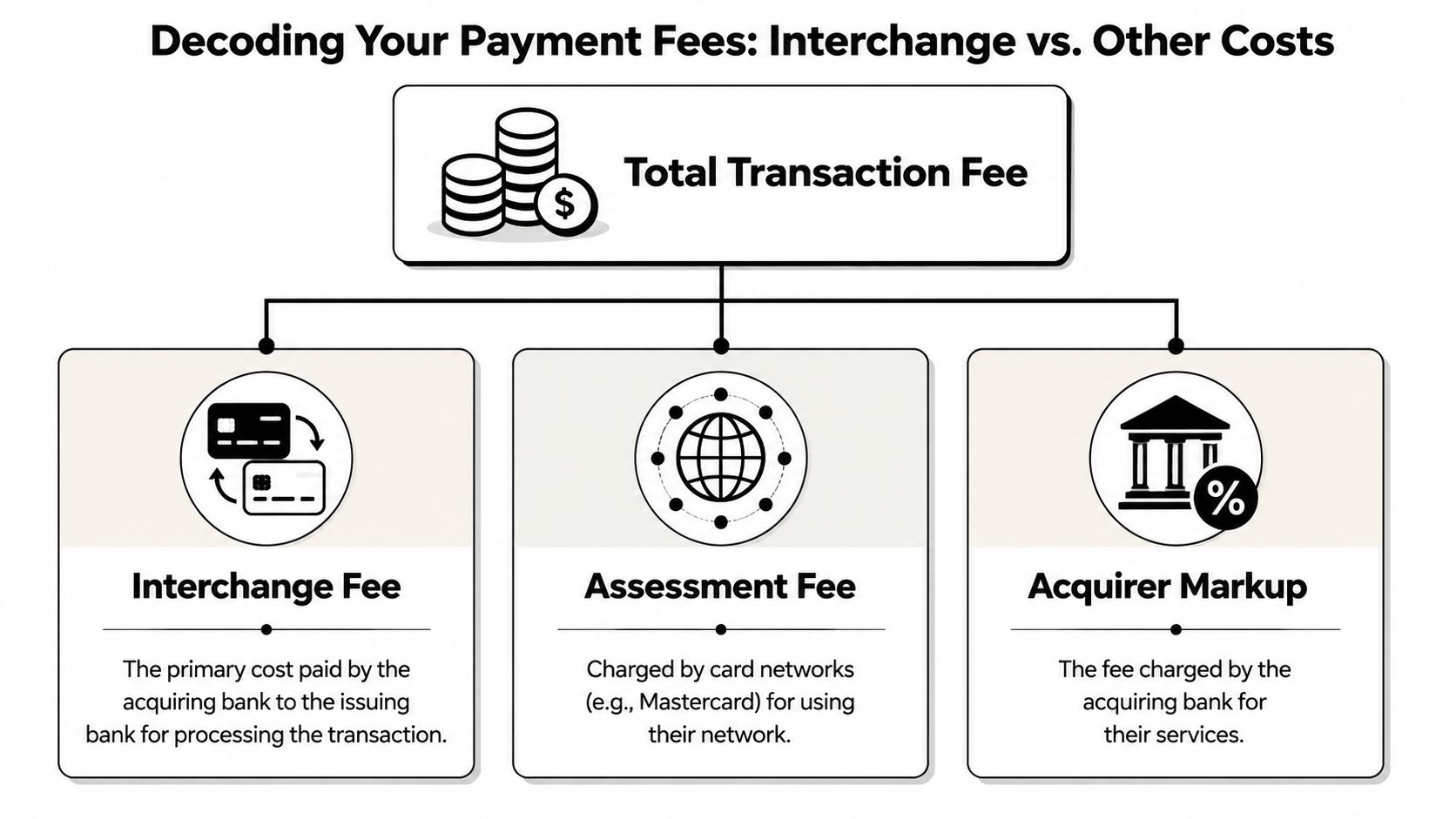

Decoding Your Payment Fees Interchange vs Other Costs

A Shopify merchant sees a $100 international order come in and expects roughly the same margin as a $100 domestic order. Then the payout lands, and the gap shows up. Part of that gap is easy to miss because "processing fee" sounds like one line item, when it is really a stack of separate charges.

The three parts of a card transaction cost

| Fee type | Who gets paid | What it covers |

|---|---|---|

| Interchange fee | The customer's card-issuing bank | The core cost of accepting the card |

| Assessment fee | The card network, such as Mastercard | Use of the network rails |

| Processor markup | Your payment provider or acquirer | Their service, risk handling, and account economics |

For Shopify stores, interchange usually deserves the closest attention because it changes based on the details of the sale. The type of card matters. The country of the cardholder matters. Selling online instead of in person matters too.

A useful way to read this is to separate fixed platform relationships from transaction-specific costs. Your processor markup is tied to the provider you chose. Interchange and assessments are more like upstream charges built into the card system itself. So if an international order costs more than a domestic one, your payment partner is only one part of the story.

Interchange functions like the route fee charged for access to the issuing bank's side of the payment system. A local online purchase usually follows a simpler path. An international ecommerce payment can involve extra checks, more settlement complexity, and more risk controls before the money reaches your account.

That is why two orders with the same cart total can leave you with different profit.

If you're still sorting out which company does what, this guide on merchant accounts vs payment gateways explains how the bank, gateway, processor, and acquirer each fit into the payment flow.

A common mistake among Shopify merchants is blaming the full fee on the processor. In many cases, a meaningful share of the cost is set by the card network and the cardholder's bank before your provider adds its own markup.

Why this matters for Shopify stores

This distinction affects pricing decisions, market selection, and fraud controls.

Most Shopify transactions are card-not-present, which already carries more risk than an in-store swipe or tap. Add a foreign-issued Mastercard, and the transaction often becomes more expensive before any app fees or provider markup are layered on top. If that order later turns into a chargeback, the margin pressure gets worse fast. You paid more to accept the sale, and then you may lose the revenue, the product, the shipping cost, and a dispute fee.

That is the core reason fee breakdowns matter. They help you see which international orders are merely expensive, and which ones are expensive and risky at the same time.

The Anatomy of Mastercard International Interchange Rates

A Shopify order from another country can look simple on your dashboard. The customer clicked buy, the payment went through, and the sale feels done. Under the hood, though, that same order often travels through a pricier route than a domestic one, and that is why Mastercard international interchange works more like a menu of rate categories than a single flat fee.

Geography changes the price

The first factor is location. If the card was issued in another country, the transaction usually costs more than a domestic one.

For a Shopify merchant, that extra cost comes from added routing, currency handling, settlement steps, and tighter fraud screening. A domestic payment is the shorter route. A cross border payment is the longer route with more checkpoints. More checkpoints usually mean more cost.

You do not need to memorize every Mastercard table to understand the pattern. International transactions often sit above comparable domestic transactions before your processor markup and other network fees are added. So when you start selling into the UK, Canada, Australia, or Europe, your payment cost can rise even if your product, cart value, and ad costs stay the same.

Card type changes the rate

The second factor is the card itself.

A basic debit card is usually cheaper to accept than a premium rewards credit card. That difference matters online because many international shoppers use travel, rewards, or high tier cards. Those cards may be great for customer loyalty. They are not always great for your margins.

A merchant guide from Chargebacks911's Mastercard fee summary shows how wide the spread can be across debit, core credit, and premium credit categories, especially when card-not-present ecommerce is involved. For a Shopify store owner, the takeaway is simple. Two international Mastercard orders with the same order value can carry very different interchange costs because the customer used different card products.

Ecommerce pushes transactions into costlier categories

Online checkout adds another layer. In a retail store, the chip card is physically present and the issuer gets stronger signals that the buyer is legitimate. On Shopify, you rely on billing data, shipping details, device signals, and fraud tools instead.

That does not mean online payments are bad. It means they are priced for more uncertainty.

If you want a cleaner picture of which company routes the payment and where interchange sits in that chain, this guide on what a payment processor does helps connect the dots.

This short video gives a useful high-level view before you go back to your own payment reports.

For international Shopify sales, the expensive combination often looks like this:

- Foreign-issued Mastercard

- Card-not-present checkout

- Premium or rewards card product

- Extra fraud screening

That mix matters because higher acceptance cost and higher dispute risk often show up together. The same signals that make an issuer or network price the transaction more carefully can also point to a greater chance of fraud, confusion, or a later chargeback.

A practical way to read interchange is this: the more risk checks and exception handling a transaction needs, the more it tends to cost you.

Rate schedules do not stay fixed

Mastercard also updates parts of its interchange schedule over time. Fees can change, categories can shift, and a market that looked profitable last quarter can become tighter if your payment costs rise while your product price stays the same.

That is why Shopify merchants should review international performance by country, card mix, and dispute rate instead of looking only at top line revenue. A market with strong sales volume can still underperform if higher Mastercard interchange and a heavier share of international chargebacks keep shaving down the profit from each order.

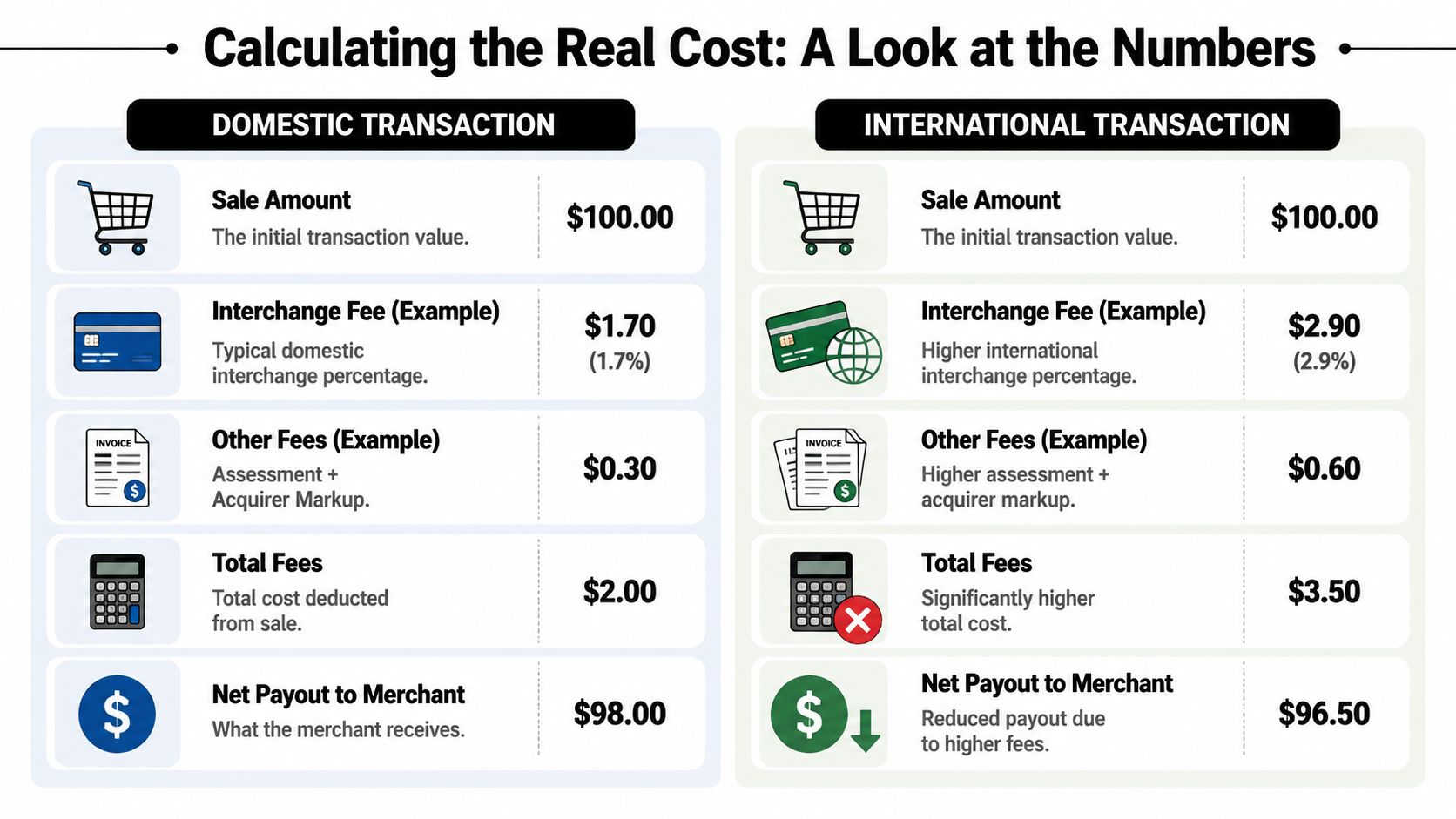

Calculating the Cost: A Look at the Numbers

A $100 international order can look healthy in Shopify. Then the payout lands, and the margin is thinner than expected.

The easiest way to see why is to hold the sale amount steady and change only the card scenario.

Example one domestic standard credit

Start with a $100 domestic sale paid with a standard credit Mastercard. Using the example rates noted earlier in the article, the interchange rate is 1.55% + $0.10.

Here is the math:

- Percentage portion: 1.55% of $100 = $1.55

- Per-transaction portion: $0.10

- Interchange total: $1.65

That is only one layer of the fee stack. Your processor markup and Mastercard assessment fees still sit on top, which is why your statement total is always higher than interchange alone.

Example two international standard credit

Now keep the order at $100, but change the card to an international equivalent at 2.10% + $0.20.

The math changes fast:

- Percentage portion: 2.10% of $100 = $2.10

- Per-transaction portion: $0.20

- Interchange total: $2.30

Same product. Same selling price. Different card context. Your interchange cost rises by $0.65 on that one order.

Side-by-side comparison

| Scenario | Example interchange rate | Interchange on $100 sale |

|---|---|---|

| Domestic standard credit | 1.55% + $0.10 | $1.65 |

| International equivalent | 2.10% + $0.20 | $2.30 |

On one order, $0.65 may feel minor.

Across hundreds of international orders, it starts acting like a quiet margin leak. If you sell lower-margin products, or your average order value is modest, that extra cost can absorb a meaningful share of your profit before shipping, returns, and support time enter the picture.

Why this matters for Shopify merchants

Shopify merchants often focus on conversion rate, ad spend, and average order value first. Those numbers matter, but payment mix matters too. A market can produce strong sales volume and still underperform if a larger share of orders comes from costlier international cards.

That is why it helps to compare your card costs with your broader checkout setup. If you want a merchant-focused baseline, this guide to Shopify payment processing fees can help you line up what Shopify shows in reports with what you see in your payout and processor statement.

One more point matters for cross-border sales. Higher acceptance cost is only the first hit. If one of those pricier international orders later turns into a chargeback, the margin you already gave up on processing fees gets squeezed even harder.

How High Fees and Chargebacks Hurt Your Margins

A Shopify store owner sees a healthy international order come through, ships it out, and expects a solid profit. Then the payout lands smaller than expected. A few weeks later, the order turns into a dispute. What looked like a good sale now becomes a loss.

That is the margin problem with cross-border sales. The order often costs more to process from the start, and it is also more likely to create expensive cleanup later.

Why the same risk shows up in both places

International card costs and international chargebacks often come from the same root problem. More uncertainty.

For a domestic in-person purchase, there are fewer moving parts. For an international ecommerce order, the bank and card network are dealing with a buyer in one country, a merchant in another, currency conversion, longer shipping routes, and fewer simple ways to confirm what happened. That added uncertainty raises the cost of acceptance. It also raises the odds of confusion, fraud claims, or delivery-related disputes.

For Shopify merchants, this matters because the extra fee is only the first cut into margin. If the order later becomes a chargeback, you are no longer dealing with just a more expensive transaction. You are dealing with a sale that may reverse after you already paid to acquire the customer, fulfill the order, and support them.

What one bad international order can take away

A disputed cross-border order can chip away at profit from several directions at once:

- Higher card acceptance cost upfront because the transaction falls into a more expensive international category

- Lost revenue if the issuer sides with the cardholder

- Lost product and shipping cost if the item cannot be recovered

- Team time spent pulling tracking, customer emails, and order records

- Extra dispute expense that adds to the loss. If you want the basics, this guide explains what a chargeback fee is

That stack of losses is what makes international disputes so painful. The sale was already less profitable before the chargeback ever arrived.

Why thinner-margin Shopify stores feel it faster

A high-ticket store with wide margins may absorb a few expensive international mistakes. A Shopify merchant selling cosmetics, supplements, accessories, or other lower-margin products has much less room.

Here is the simple math. If an international order already gives up more of the sale to payment costs, your cushion is smaller from day one. If that same order turns into a chargeback, one bad outcome can erase the profit from several successful orders in that market.

That is why international growth is not just a sales question. It is a margin control question. A country can look promising in Shopify reports because order volume is rising, but if those orders carry higher card costs and a higher dispute rate, the market may be less profitable than it appears.

The practical lesson is straightforward. More international sales do not always mean more money kept. What matters is how much of each sale survives fees, friction, and chargebacks.

Protect Your Profits How to Manage International Costs

You can't negotiate away Mastercard's entire pricing structure as a typical Shopify merchant. You can control how much damage it does.

The first move is operational. Reduce avoidable friction before the dispute ever starts. Clear currency display, clean descriptor information, accurate shipping timelines, localized support, and tighter fraud review all help. They won't lower interchange by themselves, but they can reduce the number of expensive international orders that later become revenue losses.

Focus on the levers you can actually control

Some merchants improve economics by adjusting payment routing, localizing checkout, or steering demand toward markets where payment friction is easier to manage. Others get stricter about which orders they manually review before fulfillment.

What matters is choosing practical controls, not chasing a perfect fee table.

A good working checklist looks like this:

- Review card origin trends: Look at which countries produce profitable repeat buyers versus costly one-off disputes.

- Tighten fraud signals: Pay close attention to mismatched billing and shipping patterns, rushed shipping requests, and orders that don't fit normal customer behavior.

- Audit customer communication: Many chargebacks start as confusion. Make billing descriptors, shipping updates, and return policies easier to understand.

- Compare market-by-market margin: Revenue from a country isn't the same thing as healthy profit from that country.

Why risk management matters more right now

Mastercard announced in 2024 that it would lower U.S. credit card interchange for at least five years as part of a settlement, which raises a real operational question for merchants selling globally: whether international pricing will also ease, or whether more cost pressure will remain in cross-border transactions, as described in Mastercard's 2024 settlement announcement.

That uncertainty is exactly why chargeback control matters. If domestic card costs change while cross-border costs stay high, the merchants who protect dispute revenue will be in a better position than the merchants who only watch headline fee changes.

You may not be able to stop every expensive international transaction from happening. You can build a system that keeps more of the revenue those orders create.

ChargePay helps Shopify merchants protect that revenue after the sale. It has a 92.4% win rate, has handled 100K+ disputes, and recovered $2.8M+ for merchants. ChargePay is built for Shopify stores dealing with fraud, friendly fraud, and chargebacks from domestic and international orders alike. It also has a 4.9-star rating and a Built for Shopify badge. If chargebacks are eating into the already tighter margins of cross-border sales, install ChargePay from the Shopify App Store.

.svg)

.svg)

.svg)

.svg)