A weak checkout is a direct path to fraud, chargebacks, and lost margin.

For Shopify merchants, the payment gateway is not just the tool that accepts a card or wallet payment. It is the control point where transactions are encrypted, verified, screened for fraud, and either approved or stopped before they become expensive problems. If that setup is loose, you do not just face more fraudulent orders. You also lose more chargeback disputes because preventable risk was allowed through at the moment of payment.

That is why payment gateway security deserves the same attention as conversion rate. The goal is not only to process more orders. It is to protect clean revenue and avoid shipping inventory on transactions you were unlikely to keep.

If you are still sorting out how the gateway fits into the rest of your payments stack, this guide on the difference between a merchant account and a payment gateway gives useful context.

One risk gets missed often. Third-party scripts on checkout pages, including chat widgets, tracking tags, and app code, can expose payment data or interfere with the payment flow without obvious warning. For a Shopify store, payment gateway security is a revenue protection strategy first, and a technical project second.

Why Your Payment Gateway Is Your First Defense Against Chargebacks

A weak checkout stack creates two losses at once. First, you ship an order that should never have been approved. Then you lose the revenue again when the cardholder files a fraud dispute.

That's why payment gateway security matters long before a chargeback notice lands in your inbox. Your gateway controls how card and wallet payments are routed, encrypted, verified, and screened. If that setup is loose, fraudsters don't need to break your whole store. They only need to exploit the weakest step in the payment flow.

Fraud prevention starts before representment

A lot of merchants treat fraud tools and chargeback management as separate jobs. In practice, they connect directly.

When your gateway blocks obvious abuse, rejects suspicious mismatches, and limits exposure to raw card data, you reduce the pool of transactions that later become “true fraud” chargebacks. When it doesn't, your dispute team inherits bad orders that were avoidable from the start.

Practical rule: Every fraudulent order you stop before authorization is worth more than a dispute you try to win after fulfillment.

Shopify merchants often ask whether the gateway or the merchant account matters more. The useful answer is that they work together, but the gateway is where a lot of your live security decisions happen. If you need a clearer breakdown, this guide on merchant account vs payment gateway is a good place to compare roles.

What weak gateway security looks like in the real world

It usually doesn't look dramatic. It looks ordinary.

- A stored card detail appears where it shouldn't because tokenization wasn't set up correctly.

- A checkout script gets altered and starts leaking customer payment data before the gateway ever sees the transaction.

- A rushed configuration leaves authentication too permissive, so suspicious orders sail through.

- A merchant assumes PCI compliance equals full checkout safety, even though browser-side dependencies remain exposed.

ChargePay has handled 200K+ disputes, recovered $10.8M+, and posted a 92.4% win rate for Shopify merchants, based on ChargePay platform data. One pattern shows up again and again. Stores with tighter payment controls tend to face cleaner dispute mixes. Stores with weak controls lose money earlier, then spend more time trying to recover it later.

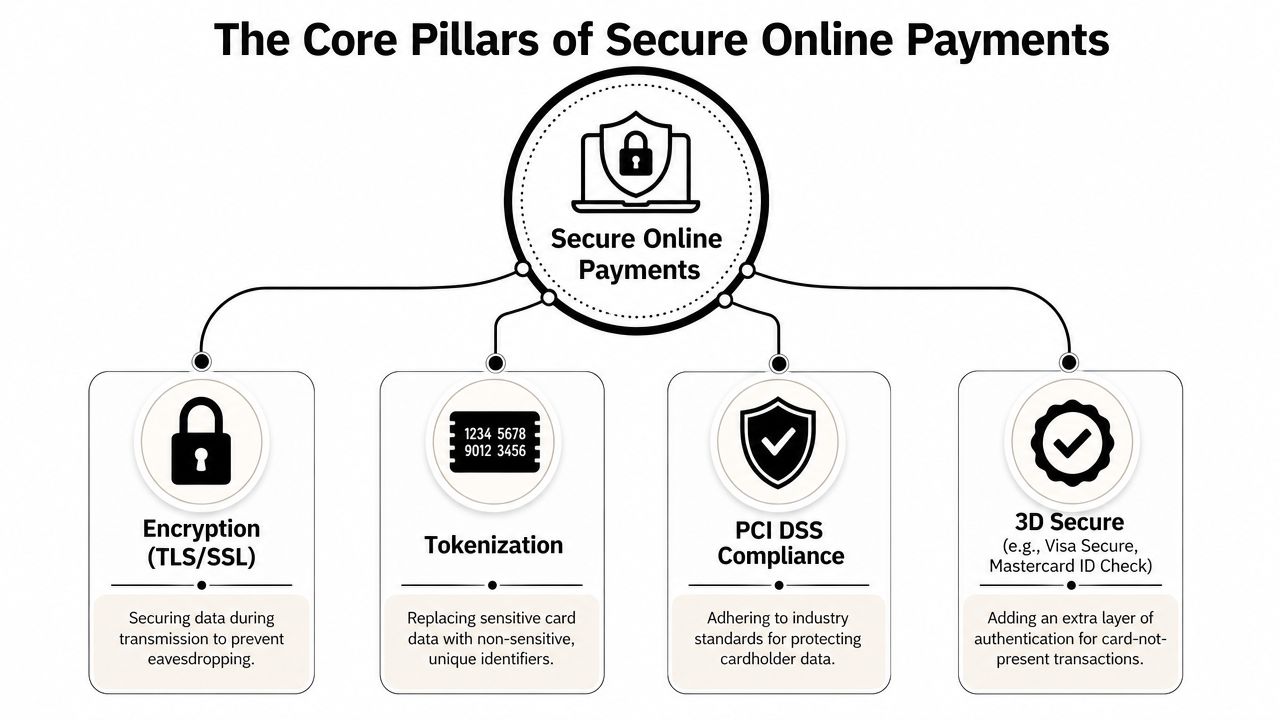

The Core Pillars of Secure Online Payments

The language around payment gateway security gets technical fast. For a Shopify merchant, the useful question is simpler: what stops stolen data, fake purchases, and bad disputes from reaching your bank account?

These four controls do most of the heavy lifting.

Encryption protects payment data in transit

TLS/SSL encryption secures card data while it moves between the shopper's browser and the server. Without it, payment details can be exposed during transmission.

The business impact is straightforward. Encryption helps stop eavesdropping and data interception, which means fewer opportunities for card details to be stolen on the way to authorization. If you're comparing providers or planning a custom payment processing integration, this is one of the first controls to verify because it affects every transaction that passes through your checkout.

Tokenization keeps raw card numbers out of your store

Tokenization replaces the actual card number with a random token. The merchant uses the token, while the actual card data stays outside the merchant environment.

That reduces your exposure in two ways. First, your systems have less sensitive data to protect. Second, your PCI burden is easier to manage because fewer internal systems touch actual cardholder data. This breakdown of encryption vs tokenization is useful if your team still treats them like the same thing.

If your store can operate without ever storing the real primary account number, that's almost always the safer path.

PCI DSS sets the minimum floor

PCI DSS is the baseline standard for handling cardholder data safely. It isn't a marketing badge. It's the framework gateways follow to protect customer data and reduce fraud risk.

Merchants often make one costly mistake here. They hear that their gateway is PCI compliant and assume the whole payment journey is safe by default. That's not how this works. PCI compliance matters, but it doesn't erase bad app choices, weak admin access, or unsafe checkout scripts.

3D Secure adds issuer-side verification

3D Secure adds an extra verification step for online card transactions. The issuer can ask the customer to confirm the purchase before it's authorized.

For your store, that means some suspicious orders get challenged before they become shipped fraud. It can also improve your evidence position in certain disputes because there's stronger proof that the cardholder participated in the transaction.

Here's the practical view:

| Control | What it protects | What it stops from happening |

|---|---|---|

| TLS/SSL | Data in transit | Intercepted card details during checkout |

| Tokenization | Stored payment data | Card number exposure inside your systems |

| PCI DSS | Security process and controls | Weak handling of cardholder data |

| 3D Secure | Cardholder verification | Some unauthorized card-not-present purchases |

As digital payments expanded, controls like TLS/SSL, 3D Secure, and tokenization became standard defenses. That pressure makes sense when global payment transactions are projected to reach USD 9,419 billion by 2025, and payment-related incidents accounted for 20% of all cyberattacks in 2023, according to this overview of payment gateway security protocols.

Common Attacks That Turn Into Costly Chargebacks

A secure gateway doesn't mean a secure checkout.

That's the mistake many merchants make right before a fraud spike. The gateway can be doing its job perfectly while something else on the page is siphoning data, altering checkout behavior, or helping attackers test stolen cards.

The checkout page is a bigger target than most merchants realize

Take a common Shopify setup. A merchant adds an analytics app, a live chat widget, a personalization tool, and an A/B testing script. Each tool seems harmless on its own. Together, they create more browser-side dependencies on the payment page.

If one of those scripts is compromised, the attacker doesn't need access to your payment provider. They can skim card data in the browser before it even reaches the gateway. The customer sees a normal checkout. You see approved orders. Then the fraud disputes start arriving.

That's why browser-side security deserves more attention than it usually gets.

E-skimming turns “approved orders” into future losses

A fraudster injects malicious code into a payment page or into a third-party script loaded by that page. The script captures card details as customers type them. Later, those stolen credentials get used elsewhere, or the original purchase gets disputed as unauthorized.

For the merchant, this creates a nasty chain reaction:

- You process what looks like a normal transaction

- The order gets fulfilled

- The cardholder reports fraud

- You absorb the chargeback and operational loss

This is one reason I push merchants to think beyond “Is my gateway secure?” A better question is, “What on my checkout page can read, alter, or exfiltrate data?”

A useful starting point is understanding how 3D Secure authentication fits into your broader fraud controls. It helps, but it doesn't neutralize browser-side compromise.

Your gateway can pass every compliance check and still sit behind a checkout page that leaks payment data in the browser.

Third-party scripts are often the quiet failure point

PCI DSS v4.0 added a clear operational requirement here. Merchants need to inventory every script on payment pages, justify why each one is there, and detect unauthorized changes to scripts and security-impacting HTTP headers at least weekly, according to payment-page security guidance under PCI DSS v4.0.

That requirement matters because script sprawl is normal in e-commerce. Merchants install tools to improve conversion, not realizing that each script can widen the attack surface.

Watch closely for:

- Analytics and tag managers that inject additional code

- Chat widgets with broad page permissions

- A/B testing tools that rewrite checkout elements

- Apps you no longer use but never removed

- Custom scripts no one on your team still owns

Phishing, session hijacking, and API abuse can also feed chargebacks, but the browser-side script problem is the one many Shopify teams miss because it hides inside normal marketing operations.

Actionable Steps to Harden Your Payment Process Today

Card fraud rarely starts with a dramatic breach. More often, it starts with a weak rule, an over-permissioned app, or a checkout flow no one has reviewed in months. For a Shopify merchant, that turns into approved fraud, shipped inventory, and weaker chargeback outcomes when the issuer asks what controls were in place.

The fastest way to improve payment security is to tighten the parts of the process you can verify this week.

Start with the gateway itself

Your gateway is not just a processor. It is a fraud control point that affects which orders get approved, which ones get challenged, and how much transaction evidence you have later if a cardholder disputes the charge.

Use this checklist before you trust any provider:

- Verify PCI DSS alignment so your provider meets a baseline for protecting payment data.

- Confirm tokenization support and ask whether raw card data ever touches your environment.

- Check authentication options including 3D Secure and other step-up methods for higher-risk transactions.

- Review fraud filters for address mismatch, velocity checks, geolocation issues, and unusual order patterns.

- Understand API exposure if you run custom apps, headless components, or external order workflows.

If a gateway cannot explain how it handles risky orders, failed authentication, and transaction logging, you will feel that gap later in fraud losses and dispute representment.

Tighten the controls Shopify merchants own

A lot of loss prevention comes down to basic discipline.

- Turn on AVS and CVV checks where your provider supports them. AVS helps compare billing details against issuer records and can stop low-quality fraud before fulfillment. If you want the merchant logic in plain English, this guide to AVS address verification explains where it helps and where it falls short.

- Require strong admin security with two-factor authentication for every account that can install apps, edit themes, change payment settings, or access customer data.

- Remove stale apps and scripts from checkout-related pages. Old tools create quiet risk, especially if no one on your team still owns them.

- Review capture and fulfillment timing for higher-risk orders. Approving payment is not the same as approving shipment.

I have seen merchants spend hours tuning fraud rules while still shipping high-risk orders within minutes. That is usually an operations problem, not a gateway problem.

Here's a useful walkthrough if your team wants a quick visual refresher on payment security basics:

Audit the full data path, not just the checkout form

Approved fraud often slips through the systems around the gateway. Order data may pass through subscription apps, post-purchase tools, ERPs, customer support platforms, fraud scoring tools, and custom middleware. Every handoff is a place where weak authentication, poor logging, or exposed APIs can create risk.

Map the full path of payment-related data, tokens, and customer identity signals. Then test the controls around each connection point. Look for weak access controls, outdated dependencies, poor secret management, unpatched plugins, and missing logs. Those weaknesses do not just create security exposure. They also leave you with thinner evidence when you need to show an issuer that the transaction was legitimate and your controls were active.

If your store depends on multiple SaaS tools, a structured SaaS security checkup can help your team think beyond the gateway and look at the surrounding applications that may still touch payment-related workflows.

Merchant shortcut: List every system that can influence payment approval, order creation, fulfillment release, or transaction evidence. Fraud often enters through those connections.

Build a weekly hardening routine

Security holds up better when the work is routine, not occasional.

- List every payment-related app and integration. Include subscriptions, upsells, analytics, support tools, fraud tools, and any script that loads on checkout-related pages.

- Decide which tools belong near payment pages. Remove the ones that do not have a clear business case.

- Review admin access for staff and agencies who can edit scripts, install apps, or change checkout settings.

- Patch on a schedule so old components do not become easy entry points.

- Write down manual review rules for risky orders so your team applies the same standards every time.

- Keep evidence trails including AVS and CVV results, authentication status, device or order notes, and fulfillment decisions.

ChargePay is one option for the dispute side of this workflow. It automates evidence-backed chargeback responses for Shopify merchants and helps when suspicious transactions still turn into disputes. It does not replace payment security. It helps you recover more revenue after prevention fails.

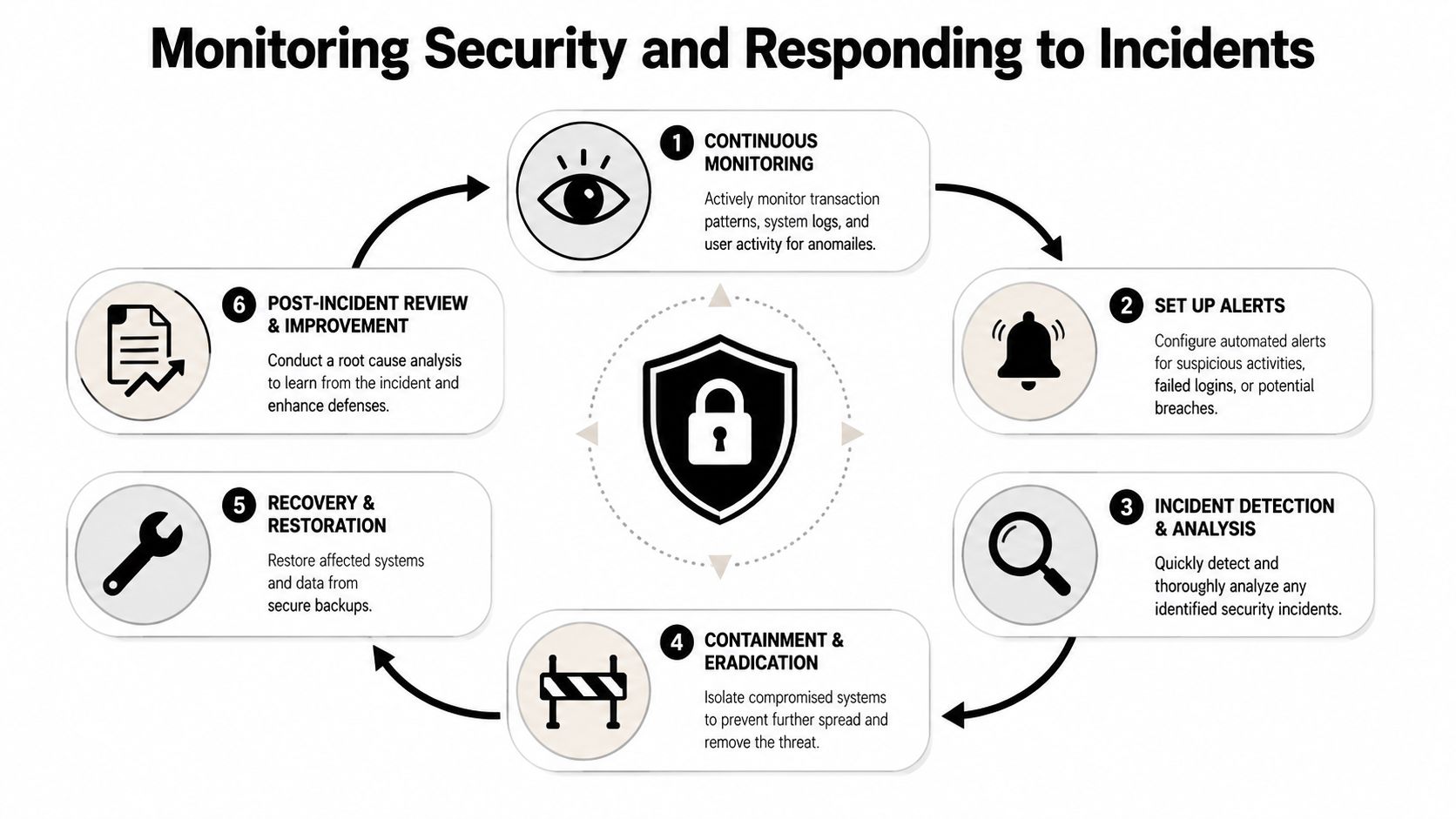

Monitoring Security and Responding to Incidents

A fraud spike rarely starts with a chargeback. It usually starts with something smaller that nobody treated as urgent. A new checkout script. A compromised staff login. A cluster of payment attempts that look odd but still get through.

For Shopify merchants, monitoring is revenue protection. If you catch abuse before fulfillment, you prevent fraudulent orders from turning into lost inventory, processor scrutiny, and weak dispute files later. If you miss it, the cost shows up twice. First in the bad order, then again in the chargeback.

Watch the signals that usually show up before losses

Useful monitoring is not about collecting every alert your tools can generate. It is about watching for patterns that tend to precede fraud and disputed orders.

Pay attention to signals like these:

- Repeated failed payment attempts from the same IP, device, or customer profile

- Orders with mismatched customer details that do not fit normal buying behavior

- Sudden demand for high-resale products or digital goods that can be fulfilled fast

- Admin logins from unusual locations or unexpected changes to checkout scripts and apps

- Orders that clear payment but trigger refund requests or customer confusion soon after

That last point gets missed often. A payment can authorize successfully and still become a bad revenue event if the order came through a tampered page, a manipulated promotion flow, or a checkout script that captured data it should not have touched. Third-party scripts on checkout-related pages deserve close attention because they sit near the point where fraud, data exposure, and evidentiary gaps can all start.

Good records help you recover money

By the time a chargeback arrives, your team is working from memory unless the store kept a clean trail. Memory loses disputes. Records give you a chance to win.

Keep the details tied to each risky transaction: fraud review notes, AVS and CVV results, 3D Secure or authentication status, order timestamps, fulfillment holds, customer messages, app changes, and any manual decision your team made. If you want a practical model for what to track, these transaction monitoring solutions show the kinds of signals and records that support both fraud review and dispute response.

The point is simple. Monitoring should feed chargeback defense, not live in a separate workflow.

Use a response plan your team can follow under pressure

A Shopify store does not need a complicated incident program. You need a short playbook that tells your team what to do in the first hour after something suspicious appears.

| Incident stage | What your team should do |

|---|---|

| Detection | Flag the suspicious transaction, login, app behavior, or script change |

| Containment | Hold fulfillment, disable the affected script or app, and restrict access for the account involved |

| Analysis | Review order logs, gateway data, customer details, and recent checkout changes to find the source and scope |

| Escalation | Contact your gateway, processor, app vendor, or hosting partner if payment data or checkout integrity may be affected |

| Recovery | Restore approved configurations, test checkout, and confirm payment and order flows are working normally |

| Documentation | Save screenshots, logs, timestamps, internal notes, and customer communications for dispute evidence and future rule updates |

Teams that respond well are usually the ones with clear ownership and a written process. They know who can pause fulfillment, who reviews script changes, who contacts vendors, and who preserves evidence before it gets overwritten.

As noted earlier, payment security also depends on ongoing testing and review outside the gateway itself. Monitoring catches changes in real time. Incident response limits the damage before fraud turns into chargebacks you could have prevented.

From Secure Payments to Winning Every Winnable Chargeback

Payment gateway security reduces risk. It does not eliminate disputes.

That's the part merchants need to keep straight. You can harden checkout, reduce exposure to raw card data, tighten scripts, and improve authentication, and you should. But some chargebacks still come from customer confusion, buyer's remorse, subscription disputes, or friendly fraud. No gateway setting can fully block those.

Security lowers the volume, operations win the remainder

Visa recommends layering EMV chip, point-to-point encryption (P2PE), and tokenization because each control protects a different point in the payment flow. P2PE protects data before it enters merchant systems, and tokenization removes the actual card number from the merchant environment, as explained in Visa's guide to secure payment technologies and layered defense.

That's the right model for chargebacks too. You need layers.

One layer blocks preventable fraud before authorization. Another catches suspicious behavior before fulfillment. The last layer handles disputes with strong evidence when a chargeback still lands. Merchants lose money when they rely on only one of those layers.

What a complete defense looks like

A practical store setup looks like this:

- Secure gateway controls to reduce fraud at the point of payment

- Checkout-page discipline so scripts and apps don't undermine the gateway

- Monitoring and incident response so suspicious behavior gets caught early

- Dispute operations that can respond fast with usable evidence

That final part is where many teams still struggle. They can improve fraud controls, but they don't have time to build representment packages, track deadlines, and spot friendly fraud patterns consistently. That's why dispute management needs to be treated as part of revenue protection, not just back-office admin.

Chargebacks don't stop just because your checkout is safer. You still need a system for the disputes worth fighting. ChargePay is built for Shopify merchants and handles the dispute lifecycle with AI-generated evidence packages, a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered based on platform data. It has a 4.9-star rating on the Shopify App Store, carries the Built for Shopify badge, and uses pay-per-win pricing. If chargebacks are draining revenue from your store, install ChargePay from the Shopify App Store.

.svg)

.svg)

.svg)

.svg)